Vertically Integrated Capital Aggregators

A Field Guide to Monopolies in Web3

Hey there,

A few weeks back, we wrote one of our first large liquid investment theses. A $280 million hack involving North Korea was not one of the risks we accounted for while underwriting it. With the benefit of hindsight, it probably should have ranked high on the list of risks to consider when deploying capital into crypto tokens.

Today’s story is a derivative of what we have learned since then. I was curious to understand what makes protocols anti-fragile and how tokens can be used as a wedge to fuel ecosystems. In the weeks since the hack, we have gone deeper into the Hyperliquid ecosystem. What became apparent quickly is that protocols in the industry have been integrating vertically to build moats that are hard to compete against.

Today’s piece explores how category leaders in Web3 maintain their moats. In a future issue, I’ll be breaking down how capital allocators are evolving to meet these changes. If these themes interest you, make sure to join us in our Telegram community here, or drop an email to venture@decentralised.co.

Note - I use the terms supply side aggregator, demand side aggregator and vertically integrated capital ecosystem quite frequently in this piece. For ease:

A supply side aggregator is one that pulls in differentiated market participants to offer a commoditised product (eg., Uber).

A demand side aggregator is one that expands offerings to a collective that looks similar from the outside (eg., Amazon).

A vertically integrated capital aggregator is a financial entity that brings together multiple parts of an ecosystem to offer users several products within the same venue.

TL;DR - Blockchains are money rails. The value of a protocol lies in its economic output. Composability and real-time verifiability allow blockchain native businesses to integrate vertically. Tokens allow participants across the stack to be incentivised with a shared medium. Teams that are intentional about how each part of the stack accrues value, have moats. Vertical integrations aid in accelerating capital velocity within ecosystems. Done well, they become a source for revenue.

The short, twitter version of the article is linked here

This is a precursor to a series exploring the slow, but gradual enterprise-ification of crypto.

It is a beautiful Saturday morning in Bangalore. As is often a habit, I spend most of it in Cubbon Park. Built over a century ago, the trees there are often older than the country they find themselves in. Near it are old buildings that were once used to design fighter jets. “2607,” I say for my OTP as the driver plugs into the streams of traffic that choke the city. I rush for Spotify to drown out the noise. J. Cole’s latest album to the rescue.

Boredom strikes a few moments later, and I seek refuge in Substack. Maybe I could order snacks from Swiggy - the equivalent of Uber Eats in town on my way home.

In a matter of minutes, I’d have used four aggregators, each of differing kinds.

Uber aggregates riders across town and positions itself as a demand aggregator. So does Swiggy. You may not find much difference in the average rider or hungry person. They can be commoditised. So as a platform, Uber gets to take 30% of each commodity (I mean human users) they have aggregated to scale. The restaurants hate this. So do the drivers. Both try to circumvent by asking the user if they can pay directly in cash and skip the platform.

The rider (or me, in this case) understands that the platform’s ability to enforce a reputation system is what makes it valuable. No cash transactions today.

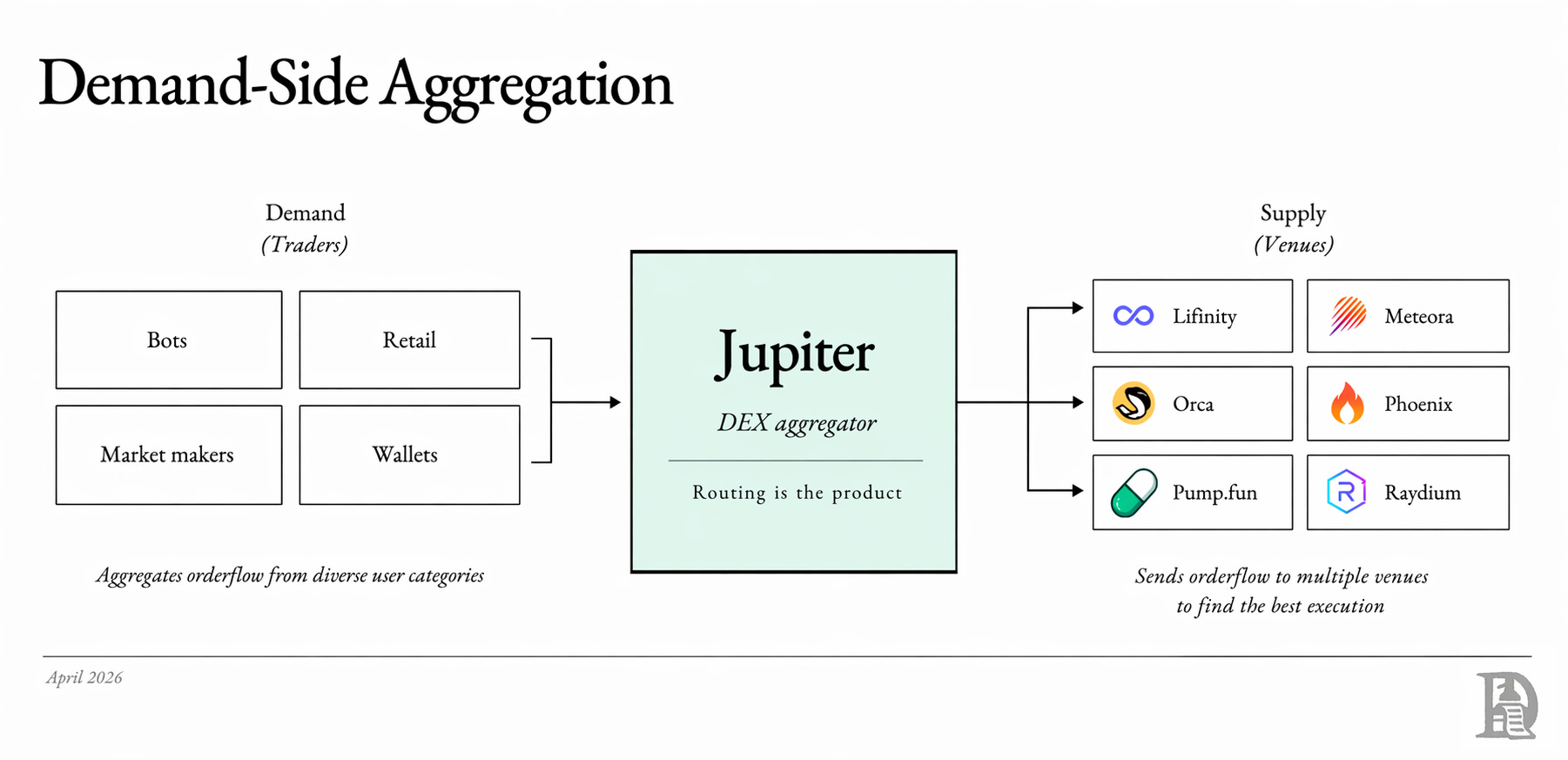

You see a version of this with Jupiter on Solana. Its influence in its early days was a byproduct of its ability to route orders across exchanges and offer the best prices to users. Instead of restaurants and drivers, Jupiter aggregates venues for my WIF buy orders to flow towards.

Substack and Spotify, however, operate on different parallels. Spotify pays up to 70% of its revenue to labels. As of last year, it paid roughly $13.75 billion to rights holders out of $20.22 billion in revenue. $0.04 of each dollar it makes reaches the artist. Substack gets to keep just 10% of what I may have paid the author of the newsletter I was reading. It has neither commodified the reader nor the writer. It simply positions itself as a tool. Perhaps, intentionally because if it were to command pricing power, the writers on the platform may simply abandon it.

Spotify is an instance of a loosely knit supply side aggregator by virtue of the number of record labels it has collaborated with. Substack on the other hand positions itself as a demand side aggregator with no pricing power by virtue of the readers on it.

Each of these apps aggregates a different side of the market. But their ability to accumulate capital (or pricing power) hinges on how well knit they are within their ecosystem. We will soon see a different version of this.

Web2 native aggregators tapped into an abundance of users that came online through two forces.

1. First was Moore’s law working its magic on the cost of a smartphone. India alone has 800 million smartphone users. Roughly 5.5 billion individuals are online today. (Cheap phones, yay!)

2. Reduction in internet costs and the rapid decline in cost of bandwidth. (Cheap internet too! yay!?!)

Crypto as an economy - in contrast has a much smaller TAM. By best estimates, ~560 million users have interacted with crypto. Last month, DeFi saw ~10 million active wallets. These are distinctly different economies, with very different rulesets.

One runs on attention. The other, powers through what flows through your wallet on-chain. We often convolute behaviour from the attention economy into what may happen in the transaction economy. People on prediction markets for instance do not behave the same way they do on Instagram.

Revisiting Aggregation

Three years back, when I first wrote of aggregators, I argued that blockchains reduce the cost of verification and trust. The original promise of the web was access. You could sit in your pajamas in New York and buy Temu goods from Shenzhen. I argued that blockchains make it possible to verify and settle a transaction with the vendor in real time at minimal cost. Or so I prophesied the industry would evolve.

Writing in 2022, with my first sponsor for this newsletter (thanks Nansen) I wrote:

We believe that blockchains will enable an entirely new category of markets that are able to verify on-chain events instantaneously. This will collapse the cost of validating intellectual property at a massive scale and thereby create new business models.

In the years since, the new markets did come on-chain. NFTs did ~$100 billion in volume since. Perps became an economy that cleared ~$14.6 trillion since. Decentralised exchanges cleared ~$10.8 trillion. The understanding that the technology will be used to clear transactions with anonymous counterparties at a global scale was true.

But at the same time, it ought to be noted that OpenSea’s volume went from ~$5 billion back then to ~$70 million this month.

Markets emerged, evolved and died. As with many things in life. In the process, they left us fuel to meander and ponder upon. Sid believes that the speculation in crypto is a feature not a bug. All new markets are undefined in the early days with participants not understanding what they are buying or why something may hold value. The novelty is baked into the price. As sanity returns, valuations become efficient and the bubble becomes memories of times past. NFTs and DeFi have had their own cycles of such mania.

These bubbles were crucial to stress-testing and validating the monetary rails that eventually set the stage for markets like the one on Hyperliquid.

Which leads me to the past few weeks of operating in crypto. Between Drift and Kelp, close to ~$578 million was hacked in the past three weeks. In the trailing twelve months, roughly ~$1.7 billion was stolen across DeFi and crypto protocols tracked by DefiLlama. Excluding stablecoin issuers - all of DeFi made roughly $3.42 billion in protocol revenue over the same window.

In other words, this past year, close to $0.50 was lost to hacks for every $1 DeFi made in revenue.

At the same time we are seeing an increase in the number of apps being released. Software itself has become a commodity. The App Store saw ~84% more apps being submitted this quarter compared to the same quarter last year. We are simultaneously seeing two forces at play. More software demanding the attention of fewer users. And fewer platforms dominating the bulk of the revenue created within crypto.

A moment back, we were with the trees in Cubbon Park. We are now realizing we lose $0.50 on every dollar earned in the industry. Sharp curve I know - but stay with me.

If we break down the $3.5 billion earned across decentralised avenues, you will see a quick pattern. Roughly 40% of it comes from derivatives platforms. Hyperliquid alone contributed some ~$902 million towards it. The second largest category is decentralised exchanges, within which the leader Uniswap made some ~$927 million in fees. Lending platforms like MakerDAO follow at third, with close to ~$500 million in combined revenue. What is common amongst all of them is that they are capital dense businesses.

Unlike products that can be built with lines of code on a Saturday afternoon, they require coordination of patient capital that is willing to accept the risks of these platforms. I explore these themes in great depth in the two stories linked below.

This is where you realise the primary difference between web2 aggregators and web3 native ones. Because blockchains are primarily toolsets to move money and verify that the nature of the transaction follows rule-sets created by developers - they become valuable only when they are able to engage in capital dense operations. Perpetual exchanges are able to put large sums of money to productive use repeatedly on the same day. Lending platforms skim a small share of the large amount of money generated as yield.

Aave for instance earned ~$123 million off the ~$920 million it made in yield over the past year. But such aggregators dominate only when they are able to own three key things.

The supply side (of liquidity),

The demand side (of users) and

Distribution.

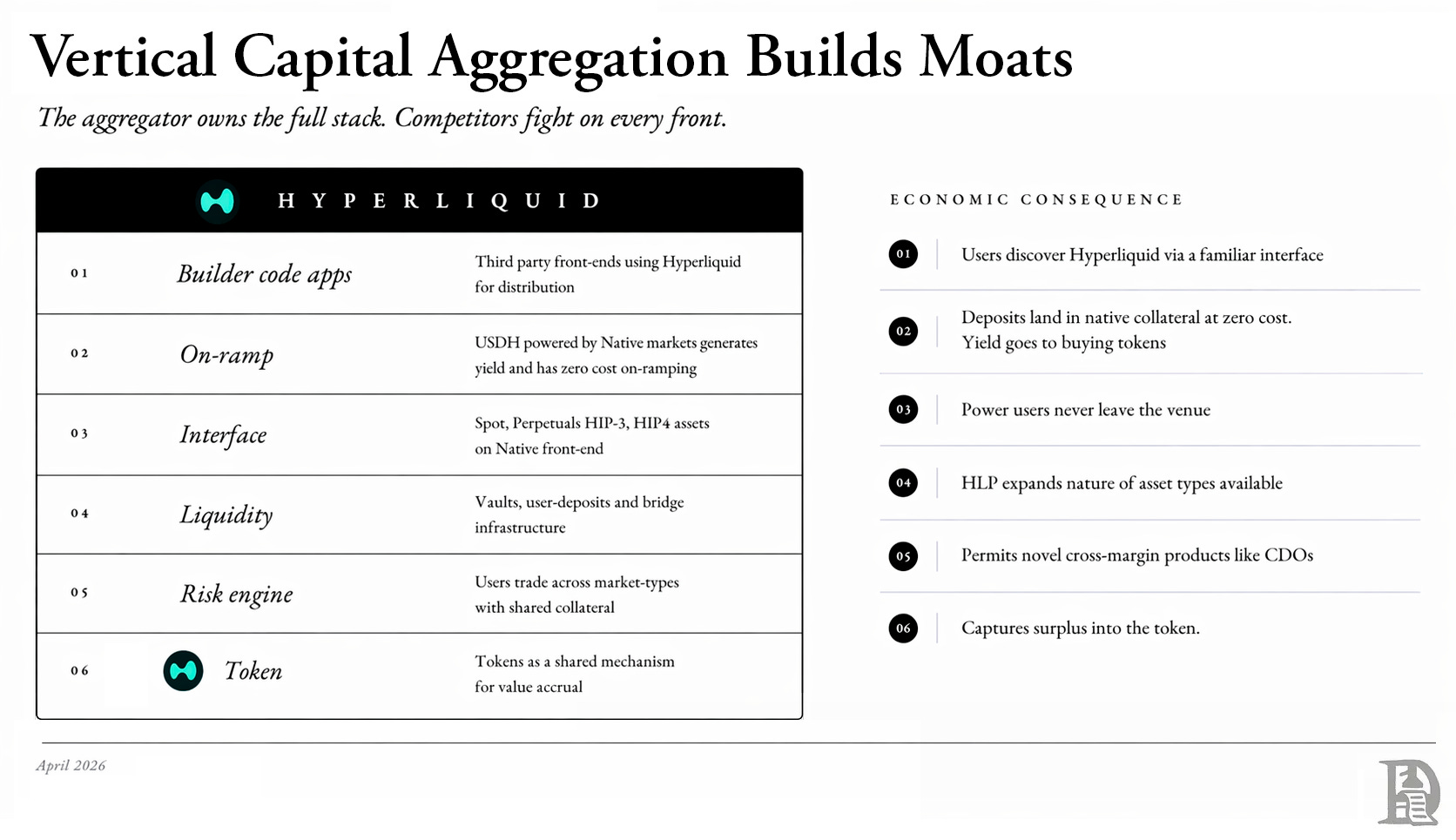

Hyperliquid is a unique beast in this regard. It has paid out close to $100 million in builder code fees but the vast majority of revenue comes from its own native front end. It is simultaneously able to retain its best users while expanding the surface area for new ones to interact with the protocol.

But what is the logic behind that? One theory is that distribution is a toll-fee paid in Web3. Large protocols tend to own and retain their best users. You realise this when you notice what amount in revenue has been created by decentralised exchanges, compared to on-chain aggregators who route orders.

On Ethereum, aggregators account for 36% of all DEX trades. On Solana, that number can be as low as ~7%, depending on the month. Kyber, 1inch, CoW and ParaSwap have combined made about ~$112 million in fees since launch. Compare that with Uniswap’s ~$5.5 billion in lifetime fees as the standalone exchange that sees the bulk of the volume. You can see a similar phenomenon in Hyperliquid too.

Combined, builder codes account only for ~6% of the cumulative ~$1.1 billion Hyperliquid has made in revenue. MetaMask’s tight-knit integration on Ethereum has earned it $184 million in fees last year through swaps. Phantom generated close to $180 million but consider that this is a small chunk of a huge economy of scale ecosystem. These products work when they are built atop a single protocol that has both the liquidity and the economic activity that is required to drive value towards them.

These products are able to attract and retain users because of the depth of liquidity available on them. Look through these lenses - capital in crypto is no longer a commoditised product. It is the most necessary ingredient. Vertical integration of capital gives participants more reasons to stay within the ecosystem. In such systems, capital begets liquidity because it can be put to productive use.

Capital is not the moat. It is a consequence of vertical integration you built. Vertical integration is the moat, and capital is the byproduct

The caveat is that it works only when parking capital is not incentivised. Don’t believe me? Take any pre-launch protocol that has an airdrop programme for deposits and you will see the case in point. Or the countless L2s that have struggled to generate value.

Any business that does capital aggregation is by extension a hack target. Drift was a target because it had ~$570 million in TVL. KelpDAO was a target because it held close to ~$1.6 billion in restaked ETH. Hyperliquid’s bridge holds close to ~$2 billion in user deposits, making it one of the most valuable standing targets in the space. You could see this play out with Ronin (~$625 million) and Nomad (~$190 million) too.

Because blockchain native businesses need high amounts of capital to be valuable, we have a dynamic where to win requires being vulnerable at least until the mechanisms to secure capital and freeze capital movements are in place.

And even when you do have capital, having a large TVL does not warrant success on its own. Capital in an economy that is parked idly, or put to little use can be a liability in the event of a hack. This is why you see protocols trying to differentiate themselves on the basis of what economic output they are able to generate, from niche usecases.

CHIP, the firm behind USDAI, has been able to place close to ~$100 million in loans this quarter, with a $1.5 billion pipeline in motion that will generate close to ~16% APY on its riskier tranches over the course of the year.

The highest risk pools on Maple generate ~15–20% APY which is comparable to or higher than the ~12.6% APY on USDC pools on Aave today. It has aggregated borrowers that can use the liquidity on the protocol to create that economic output.

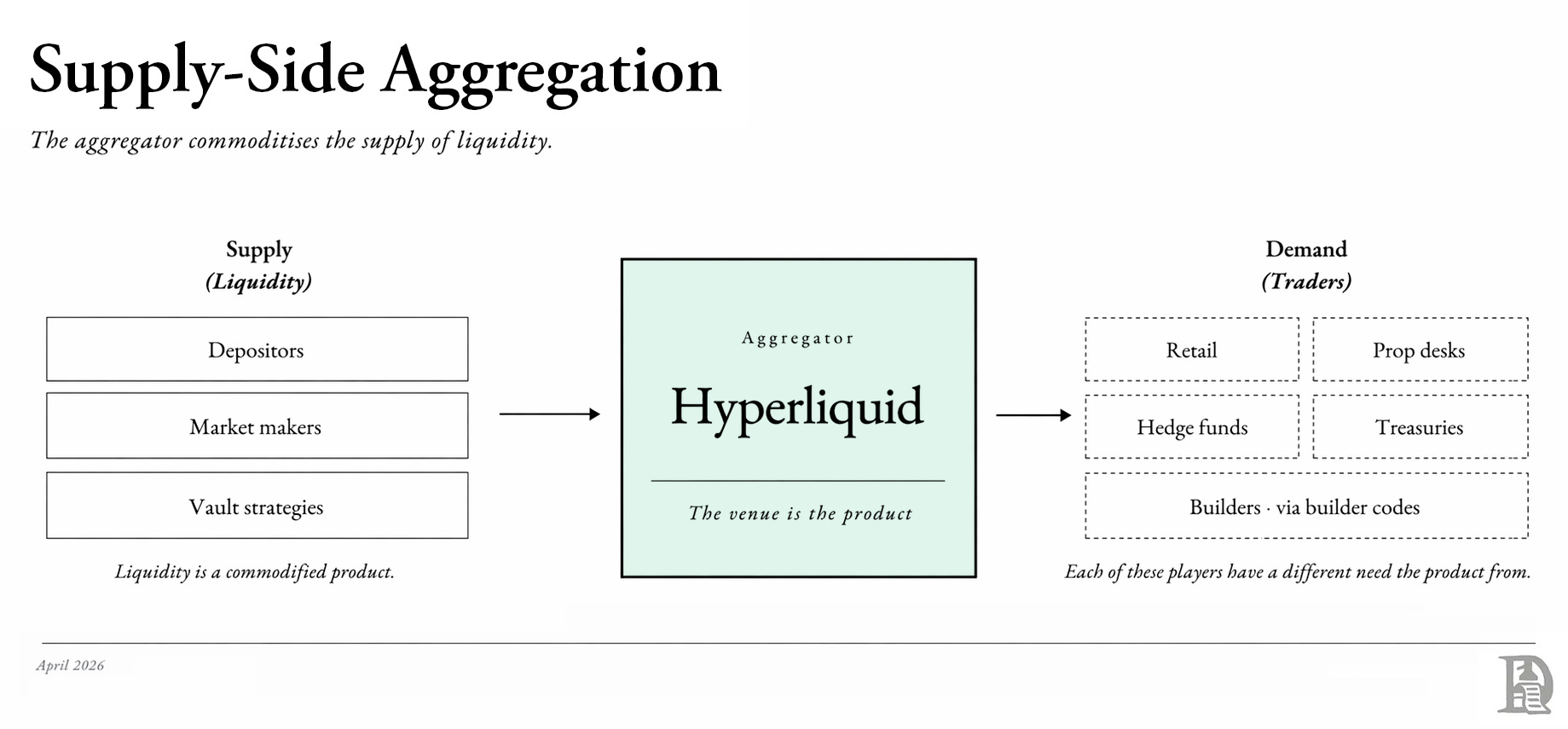

Naturally, Hyperliquid is the best instance of a supply side aggregator that has been able to put capital to meaningful use. The last year saw Hyperliquid do ~$942 million in revenue with an average of roughly ~$3.5 billion in TVL. By some very crude math, each dollar parked on the protocol has rotated close to ~285 times annually, yielding ~$0.30 in fees per $1 of TVL. Compare that to Aave’s ~$0.05 in fees generated per $1 of TVL across its lending markets.

I can almost hear my finance professor screaming at me for comparing the yield on TVL between Hyperliquid (an exchange protocol) and Aave (a lending avenue). But in a market where consumer preferences are not predetermined, and investor loyalty is not deep, capital will flow where it produces the best outcome. When accounting for hacks, investors will demand a premium for the risks involved. As it stands, perpetual exchanges are the one place that are able to take idle capital and repeatedly use it on-chain to produce fees.

I initially thought Hyperliquid is simply a supply side aggregator. It supplies capital for users willing to trade on-chain. This has been my thesis. And that is indeed true. But it breaks when you consider how it uses tokens to incentivise vertically integrating into it. But before we go there, let me explain how a vertically integrated ecosystem works.

Ticketmaster is responsible for 70% of all major live events in the United States. It is able to take 30% off tickets you buy to perhaps see Justin Bieber play his old tracks on YouTube at Coachella because it owns the venue, promotes the tour, ensures you have merch at the concert and coordinates with sponsors. The 30% you pay, is 15 times what Stripe would charge to process a ticket sold online. But you pay that premium because Ticketmaster is vertically integrated across the value chain.

You have the illusion of a marketplace: artists, venues and fans are all parties but nobody gets to argue with Ticketmaster on its cut. The same applies to Apple’s App Store. Apple is responsible for curating the store, collecting payments, ensuring the device works and bringing in the millions of users that are now attuned to the ding Apple Pay makes when you subscribe to yet another app you will never use.

Vertical Integrations in Crypto

Protocols have slowly begun carrying out the same thesis.

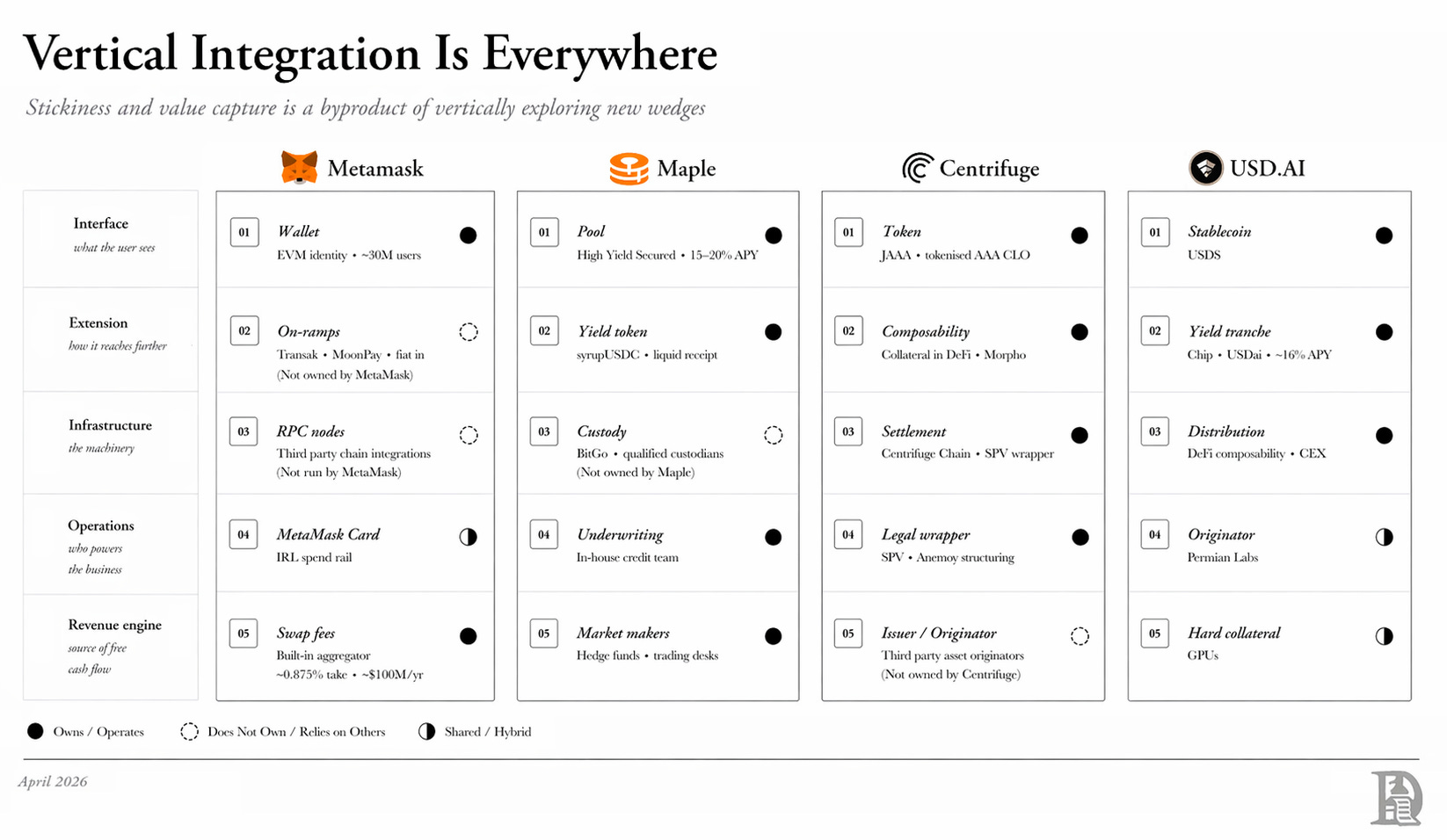

In Web3, a capital provider can be treated as commodity if vertical integrations do not make it easier to work with. Users do not have loyalty until the ecosystem is integrated such that the cumulative experience is non-existent anywhere else.

For Maple, such an integration would involve years of experience working with hedge funds and market makers. For Centrifuge, the integration involves receiving close to ~$1 billion from Grove for their JAAA bond offerings from Janus Henderson. Instead of capturing loose, abstract parts of an economy, they integrate vertically to offer the end-user a better product. In doing so, they create moats that are hard to replicate overnight.

Maple’s years of underwriting experience, or Centrifuge’s moat in being a trusted capital coordinator are moats in a world where capital and relationships have become the only things that are hard to replicate.

Firms doing vertical aggregation may routinely give up parts of the stack to a third party. Part of the reason for doing it is the lack of economic benefit from doing so. Maple owning custody or Metamask issuing its own cards may not be massively profitable when compared to the capital they generate in swaps and credit underwriting.

However, when a business scales exponentially, owning the whole stack is where the competitive edge is built. This is partly the reasoning behind M&As in the industry.

When a business has a vertical integration in play, you are not competing with a single product. The battle is against the combined experience a user has within it. On Hyperliquid, once HIP-4 is on, a user would be able to be on-ramped for free (through Native Markets), take a prediction market position, and use that position as collateral to trade on its perpetual product. Its risk engine allows this experience. And for what it’s worth, this is not possible even in TradFi today without a merchant banker.

Hyperliquid owns the user, on-ramp, risk engine, trade interface, liquidity and issues the token. For a new business to compete against it, would mean battling on six different fronts, all at the same time.

For new apps that are launching, tapping into a small share of this is meaningfully a better outcome than building on a new protocol like Monad, which has done about ~$2.6 billion in cumulative derivatives volume across all five of its perps protocols.

Integrated ecosystems like the one on Hyperliquid attract developers, more integrations, headlines and happy token holders. (Or in my case - a writer that spends his time obsessing about how these things work)

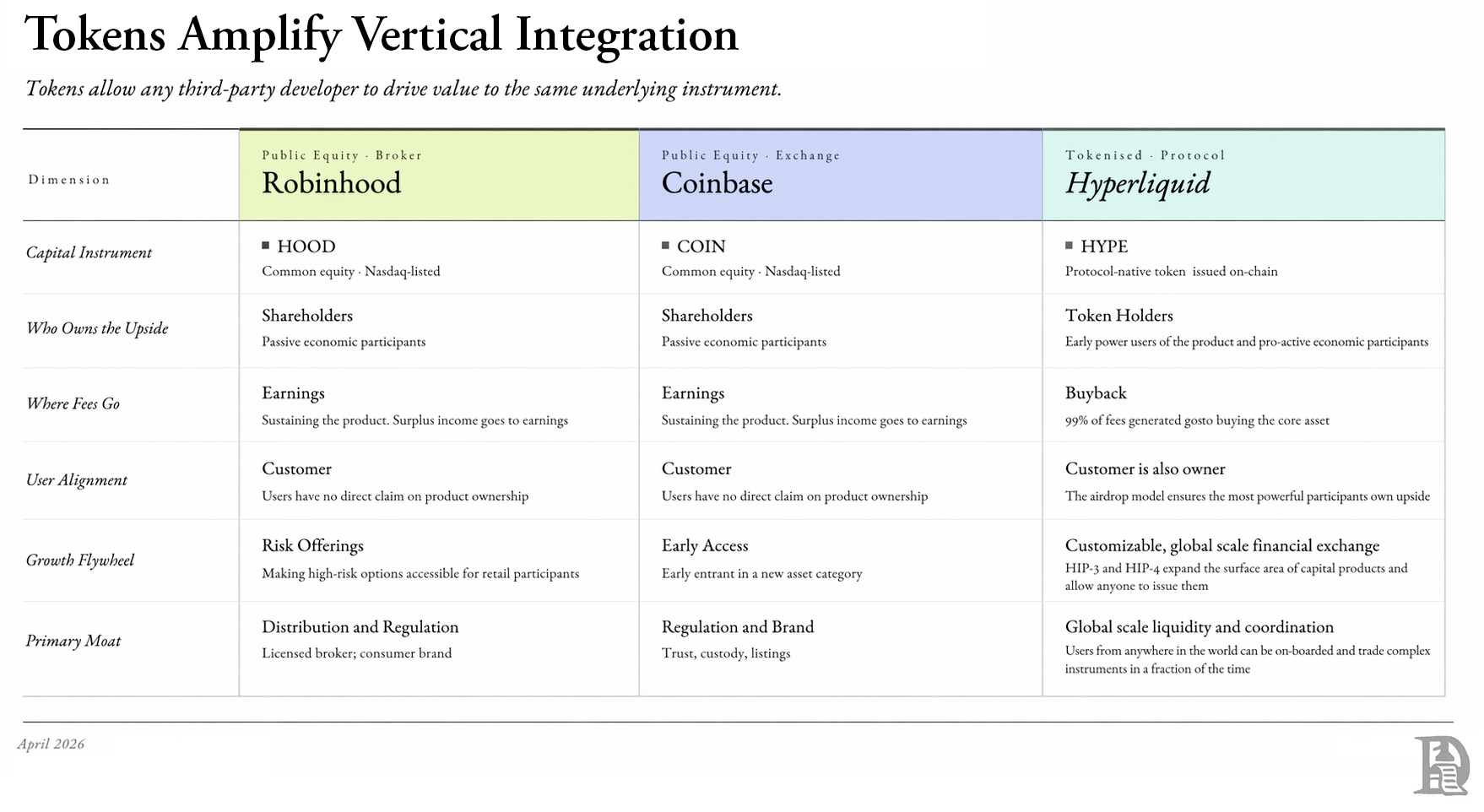

Exchanges see this shift. Coinbase acquired Deribit, has a custodial business, co-issues the currency (USDC) with Circle and captures revenue on reserves, a massive wallet infrastructure and on-boarding rails in 100+ countries. It also launched its own chain in pursuit of vertically integrating the experience. Admittedly, Coinbase may have been too early in pursuing retail users that clearly did not want to “coin” content on a blockchain or use Farcaster.

The integrations for Coinbase exists in loose terms but sits hidden behind layers of bureaucracy, regulatory hurdles and internal priorities. This is perhaps the primary difference between an open-access integrated system and a walled one. Coinbase by virtue of being an exchange with ~$60 billion in market cap has little incentive to pursue the marginal developer.

Hyperliquid in contrast benefits from developing its core avenue to the best place to trade and simultaneously creating an ecosystem whilst driving value to the underlying token.

The token is part of the integration in this context as it is the shared substrate that keeps these integrations alive and valuable. This is where you see the industry confusing itself between a tokenised protocol, and a tokenised business. A tokenised protocol is predicated on the ease with which a third-party developer can build on it. It incentivises people to drive value (downwards) to the token - often in the form of buying it back from the market.

Firms like Robinhood and Coinbase are powerful economic participants, but they cannot replicate Hyperliquid’s core network of owner-operators.

The protocol’s airdrop ensured the people that own it, were individuals that contribute economically towards it. They own enough tokens to warrant driving value towards it. Hyperliquid commits to that cause, by giving up 99% of its revenue to buy the tokens back from the market. Imagine a listed firm using 100% of its revenue to buy back ESOPs from its employees. We may see people become more accepting of capitalism perhaps.

And this is where you see how the industry is evolving whether we like it culturally or not. Solana focuses on immutability. Ethereum has its focus on censorship resistance and open source. But observe carefully where traction resides and you will see the industry adjusting ideology to commercial reality.

Hyperliquid, while a beautiful garden, is a walled one. The source code is not open-source as far as I understand. How its risk engine works is not verifiable either as far as I understand. Nobody knows what parameters go into Maple’s risk underwriting. (Or at least, I don’t). As a lender, I may not even know who underwrote the loans on USDAI. But the question is, are these parameters being openly accessible a requirement for me? I don’t quite know. Probably not.

Negotiating With Chaos

An economy cannot be built if half a dollar on every dollar created in revenue is lost to hacks in a single quarter. Founders will flock to AI, if they are expected to be responsible for hundreds of millions of dollars parked as TVL on their product. Each time there is a hack we rush to hope stablecoins are frozen. Which in turn, are often centralised.

A vertically integrated stack will eventually require giving up complete decentralisation for the sake of economic progress.

And this is not a new story on the web. In the late 1990s, visions of an open internet that allowed free speech without consequences were dreamt of heavily. Nazi memorabilia was once auctioned on Yahoo until French courts intervened in 2000. Tim Wu explores this theme in great depth in Who Controls the Internet? The story of the web, or perhaps all human commercial networks - is that of complete decentralisation paving way for a toned down version that gives up controls for the sake of economic interaction.

We settle for a diluted version of the original so that the commerce can scale, because in the absence of dilution, chaos will ensue.

This massive expansion in energy is caught in how we describe those ages. The “wild” West. The dot-com “boom”. Perhaps, even crypto is undergoing a similar expansion and toning down of energy. I explored these themes in great depth last year in the stories below.

What does this mean for founders? Observe Metamask and Phantom’s numbers. Those businesses make more money than most L2s, because they are downstream in an ecosystem with tremendous economic output. Building bridges to nowhere and exchanges for nobody is no longer a business model. Especially when the pain associated with it involves hacks. You build where the liquidity and users are today.

Mimicking a vertically integrated product overnight may not be possible. But you can build atop it.

Operating systems saw a similar pattern. When Blackberry declined and iOS became a dominant player - developers had to choose where they built. We are seeing a version of that in crypto too. Except this time, capital incentives may keep developers blinded longer.

Remember how I mentioned Cubbon Park? I often think of why the park exists clean and well kept for the decade or so I have spent time in Bangalore. Part of the reason is that there are rules. You are not allowed to spend time in it past 6 pm for instance. Or hosting an event in the middle of it may get you screamed at. Sometimes, they are harsh. But the rules keep the place functional.

Platforms and protocols on the internet are a lot similar. We may not like rules around it but they keep things functional.

In the age of vertical integrators, we may find ourselves increasingly agreeing to rules so that our dollars stay with us and the economies we spend so much of our time on, continue to scale. The trends point towards this. Stablecoins, RWAs, perpetual exchanges with closed-access risk engines, lending desks with risk underwriters that are unknown and off-chain RFQ products like Derive all point to the same trend.

That of vertically integrated capital aggregators that are willing to give up dreams of complete decentralisation for the sake of progress.

Reading loads of Neil Postman

Joel John

The 'capital is the byproduct' line is the right frame, and it gets stronger this week. The CLARITY Act yield compromise treats every protocol like a stablecoin issuer, which leaves pricing power only with firms that own user routing end-to-end. Coinbase didn't back that bill out of charity. Vertical integration is the new yield.

capital isn't the moat, it's the byproduct of owning the full stack. really excellent piece.