Coming of Age

Speculative Premia -> Fundamentals

Hey there,

Today’s piece might scream existential crisis, but hope is what it delivers. With VCs leaving the industry and founders wondering whether AI is the play to make, now is a good time to explore why we are even here. We broke down the numbers and traced where revenue flows. Today is part one of a series of articles that speak to the crux of why crypto matters, where it stands, and how it evolves from here.

Decentralised.co is actively investing in the liquid markets. The research that shapes pieces like today’s informs how we allocate. If you are an investor or a founder looking to explore how fundamentals tie back to crypto assets, join us at Telegram. Or drop us an email at venture@decentralised.co.

Let’s dig in..

The fear and greed index for crypto is at the lowest it’s ever been. At the same time, the industry has never been more profitable. Since 2018, DeFiLlama has tracked $74.8B in fees generated by crypto-native protocols. Nearly half - $31.4B was generated in the eighteen months between January 2024 and June 2025.

How is it that an industry can have its best series of quarters in eight years and still find itself in fear?

Entropy Protocol. Milkyway Protocol. Nifty Gateway. Rodeo. Forgotten Runiverse. Slingshot. Polynomial. Zerolend. Grix Finance. Parsec Finance. Angle Protocol. Step Finance. These are twelve names that shut down over the past two months. Products that have sustained for years and were built by passionate founders we respect OKX, Mantra, Polygon Labs, Gemini and Binance have each had layoffs, too.

Conferences have fewer people visiting. VCs are pivoting to AI. Developers are flocking to AI. The doom and gloom are real. If you are in crypto, pivot to AI - has become the prevailing sentiment.

But should you?

We have been thinking about this question for the past few weeks. When a technology emerges, markets initially assign it a premium due to its novelty and the scale of its ambition. Close to 6% of the UK’s GDP was invested in rail stocks in the 1800s. Hyperscaler capital expenditures will represent 2% of US GDP in 2026. But as reality hits, the technology trends towards more reasonable valuations. What matters is whether an industry can prove itself useful in the return to sanity.

In today’s issue, I break down how crypto revenue has historically evolved, the stickiness of the money generated, and the nature of moats in our industry.

Studying The Ledger

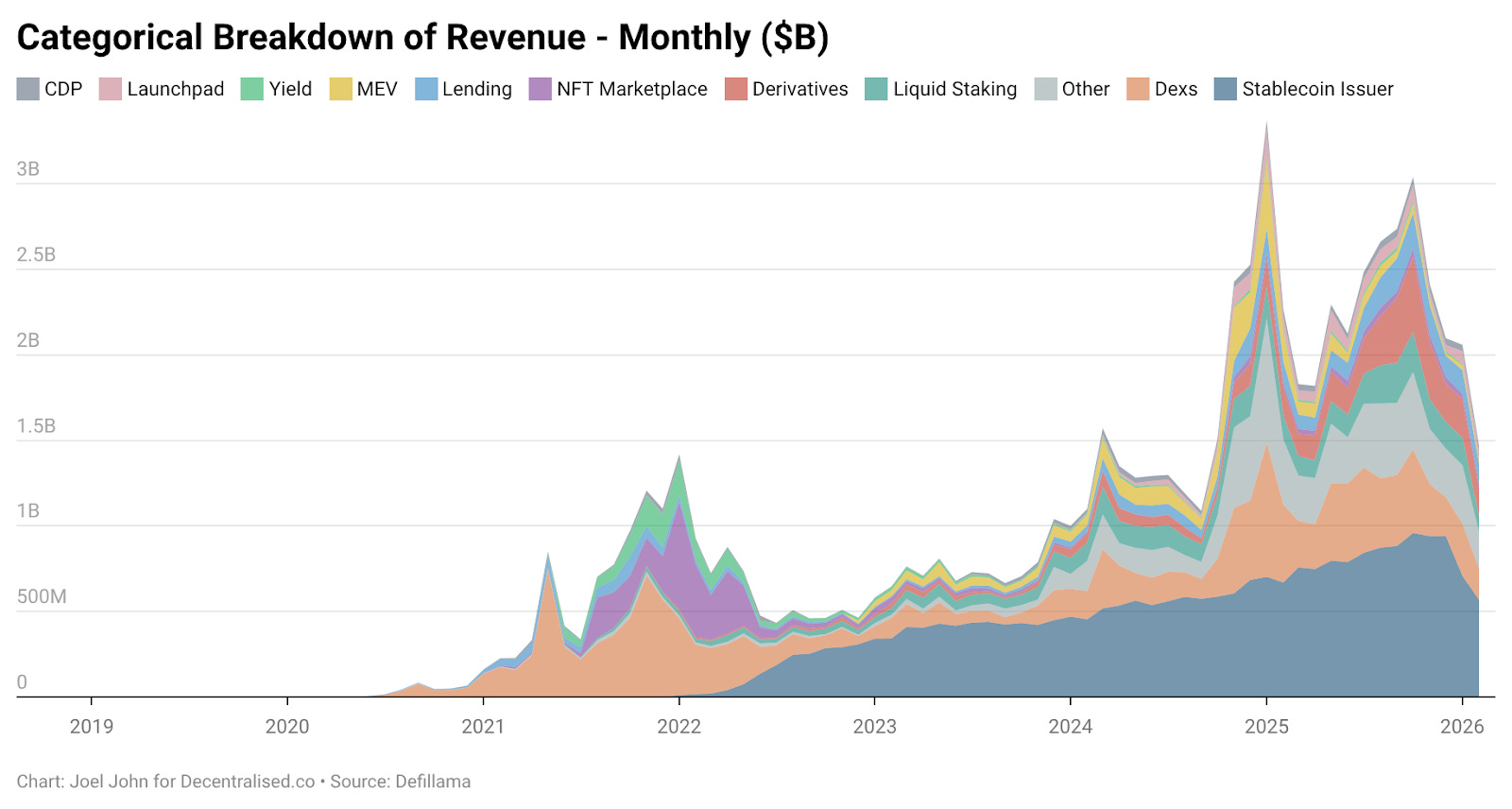

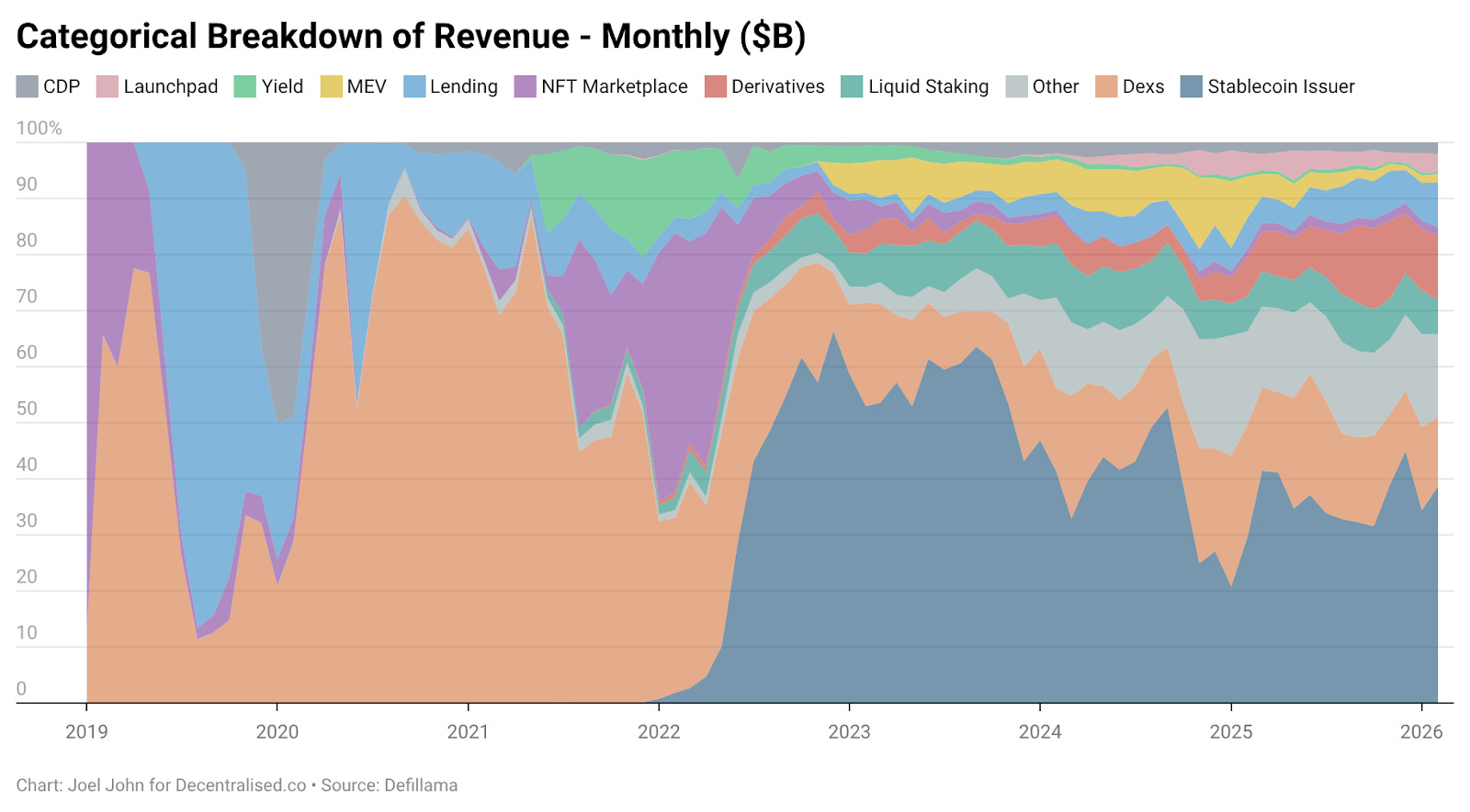

Crypto-native businesses have generated revenue since the industry’s inception. Exchanges like Bitmex, Binance and Coinbase were massively profitable endeavours. They were centralised, owned by a few individuals, and their revenue was not public. DeFi native primitives like exchanges (Uniswap) and lending platforms (Aave) changed the mood. You could verify how much the protocol made each day.

Tokens were expected to trade at valuations that reflected the economic activity these primitives enabled.

As late as 2022, decentralised exchanges accounted for 28.4% of revenue generated. Together, they generated $2.27B that year. Lending told a similar story and was highly concentrated. Aave and Compound accounted for 82% of all lending fees. There were category leaders, but there was also hope in the long-tail of protocols evolving to capture market share.

The technology itself was novel enough to command a high valuation.

Crypto’s consumer expansion closely followed. NFTs represented a hopeful vision of culture being priced on-chain. Celebrities that the average person knew were changing display pictures on Twitter. People presumed this would translate to massive adoption. OpenSea generated $1.55B or 71.7% of all NFT market revenue. In hindsight, the marketplace’s $13 billion valuation looks less absurd. They could have evolved to be a sustained monopoly.

Fate and markets had other plans. In 2025, NFTs accounted for less than 1% of revenue. We had our Beanie Baby moment, but it left us with no physical memorabilia. Decentralised exchanges, in contrast, grew but struggled to capture any valuation gains. Last year, decentralised exchanges generated $5.03B in fees. Lending platforms generated $1.65B in fees. Combined, these two segments account for 22.9% of overall fees, down from 33.1% in 2022.

Their economic activity represents a smaller share of a larger pie, but their valuations have dropped drastically.

What grew then?

How did crypto’s native business models evolve in the years since 2022?

The chart below offers clues.

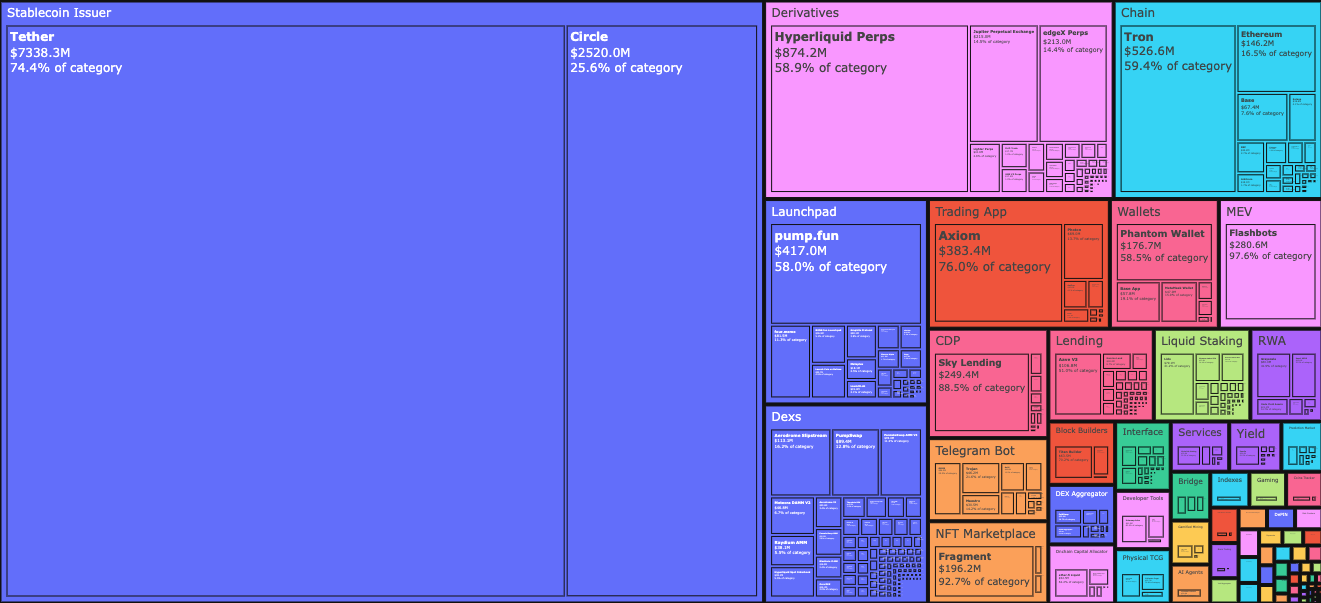

In January 2026, stablecoin issuers Tether and Circle accounted for 34.3% of all fees generated. Put differently, $0.34 of every dollar earned in the industry goes to two firms. Their revenue has doubled from $4.95B in January 2023 to $9.89B in 2025, driven almost entirely by T-bills. These are startup metrics for bank-scale financial products. Tether generates almost three times as much revenue as Circle.

Their rise came down to two forces.

The first was demand. The Global South always needed instruments to hedge against local inflation and to move money freely. Dollars, even digital ones, fill that gap in a way local currencies cannot. Capital flight is a necessity. Not a feature.

The second was the cost structure. Blockchains absorb the operational aspects of running a stablecoin business. Unlike traditional banks or fintechs, Tether and Circle do not need to hire in proportion to the amount of stablecoins issued on-chain. The marginal cost of issuing the next $1 billion on-chain and moving the next $100 billion between addresses is next to zero.

The two forces tangoed. One was pulled from the demand side as citizens voted with their money. The other flattened the cost curve. Together, they made stablecoin issuance one of the most capital-efficient businesses in financial history.

Stablecoin businesses require moats in liquidity, compliance, and the Lindy effect. The number of issuers that have survived multiple cycles is incredibly small. Between Tether and Circle, close to 99% of all stablecoin issuance revenue is captured. Why is that the case? Both assets benefited from being early. The network effects of multiple exchanges plugging in legitimised them in a way technology could not.

Tether had initially launched on Omni as a side-chain. It was slow and clunky, but it was also accessible in the touchpoints OTC desks and exchanges interacted with. That was a distribution moat, not a technology one. A moat that crypto-native founders often struggle to replicate with code alone.

Stablecoins benefited from the Lindy effect.

A new category would soon benefit from distribution moats.

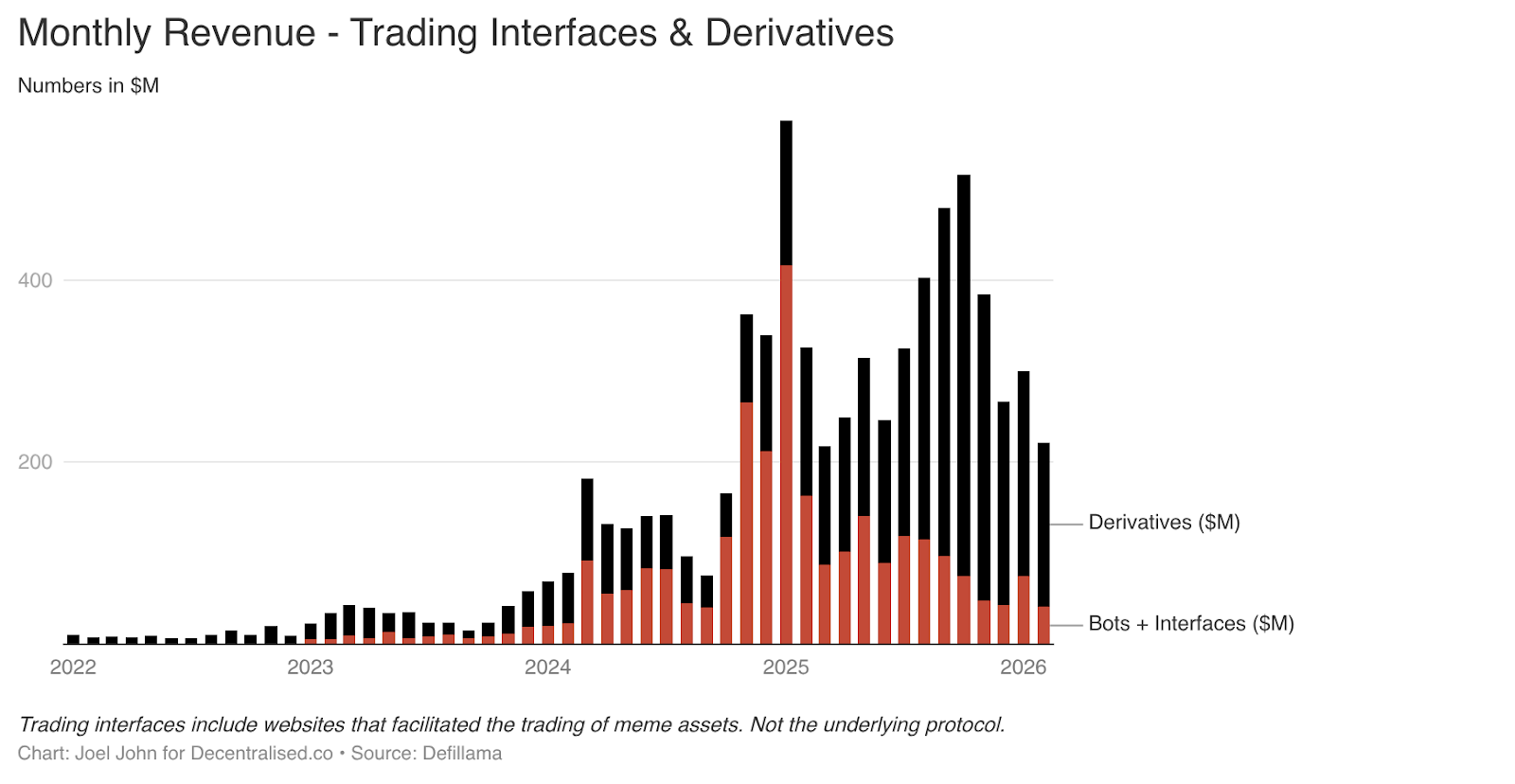

We teased the idea that crypto is a transaction economy in two of our pieces. One was Money Moves, and the other was written last year in Everything Is a Market. What we did not account for at the time was the pace at which transactional products built around Telegram trading bots and trading interfaces were growing.

Combined, in Jan of 2025, these two sectors alone accounted for $575M in fees. It makes sense when you consider what consumers want. Meme trading and perpetual exchanges allow users to make quick profits. They pay hefty fees in pursuit of quick returns. The category rose from 1% of overall revenue to just over 15% between 2022 and 2025.

Products like TryFomo and Moonshot generated millions of dollars in revenue by focusing on the end user. The product was not technically sophisticated. On the contrary, it was the ability to aggregate crypto-native primitives and bundle them to create better user experiences. Developers no longer had to incentivise liquidity or bother about wallet management thanks to tooling like Privy coming of age.

The primitives that we were all excited by in 2022 were now mature. Applications (such as BullX and Photon) were built on top of it. The sector alone created some $1.93B in fees between January 2024 and February 2026.

Meme assets had one fatal flaw. They were thin applications with great amounts of seasonality attached to them. Feels like Déjà vu? It is because NFTs and Web3 gaming had similar spurts of growth and eventual collapse. This seasonality is both a bug and a feature in our industry. We will revisit this theme shortly. But for now, let’s try to map out where revenue went instead.

Perpetual exchanges (and later prediction markets) represented new avenues with longevity. PumpFun democratised asset issuance through meme coins, but the game was not fair.

Eventually, markets wised up to the fact that meme coins die. Dreams of being a millionaire through buying a token named ShibaInuYouShouldShareThisNewsletter coin died with them. People did not want to manage a portfolio of random tokens. They wanted risk. Perpetual exchanges offered that.

You could trade Bitcoin, Solana or Ethereum with extreme leverage. Market-makers and traders that needed an alternative to centralised avenues flocked in. The core product in this category was liquidity. Hyperliquid was the dominant player because its orderbook depth was comparable to that of a centralised exchange. Without that parity, users had no reason to move over. Hyperliquid and Jupiter accounted for the bulk of the fees in the category over the past three years.

Perpetual exchanges and trading platforms ripped the band-aid off crypto. They made it apparent that capturing small sums of fees off high-velocity transactions was where the money had to be made. Meme trading platforms and perpetual exchanges were dopamine machines that packaged and sold risk.

One of them would mature to be a core financial primitive. One that the world would use to trade commodities, equities and digital assets even on a weekend. Blockchain-native apps replicated what Robinhood and Binance had long offered: avenues for risk.

Starving a Fat Protocol

Notice that I haven’t mentioned protocols so far? The base layer where all the magical internet money movements were recorded? That is because they have an entirely different (but pertinent) story to say. They are casualties of the novelty premium, which is trending towards a discount. Let me explain

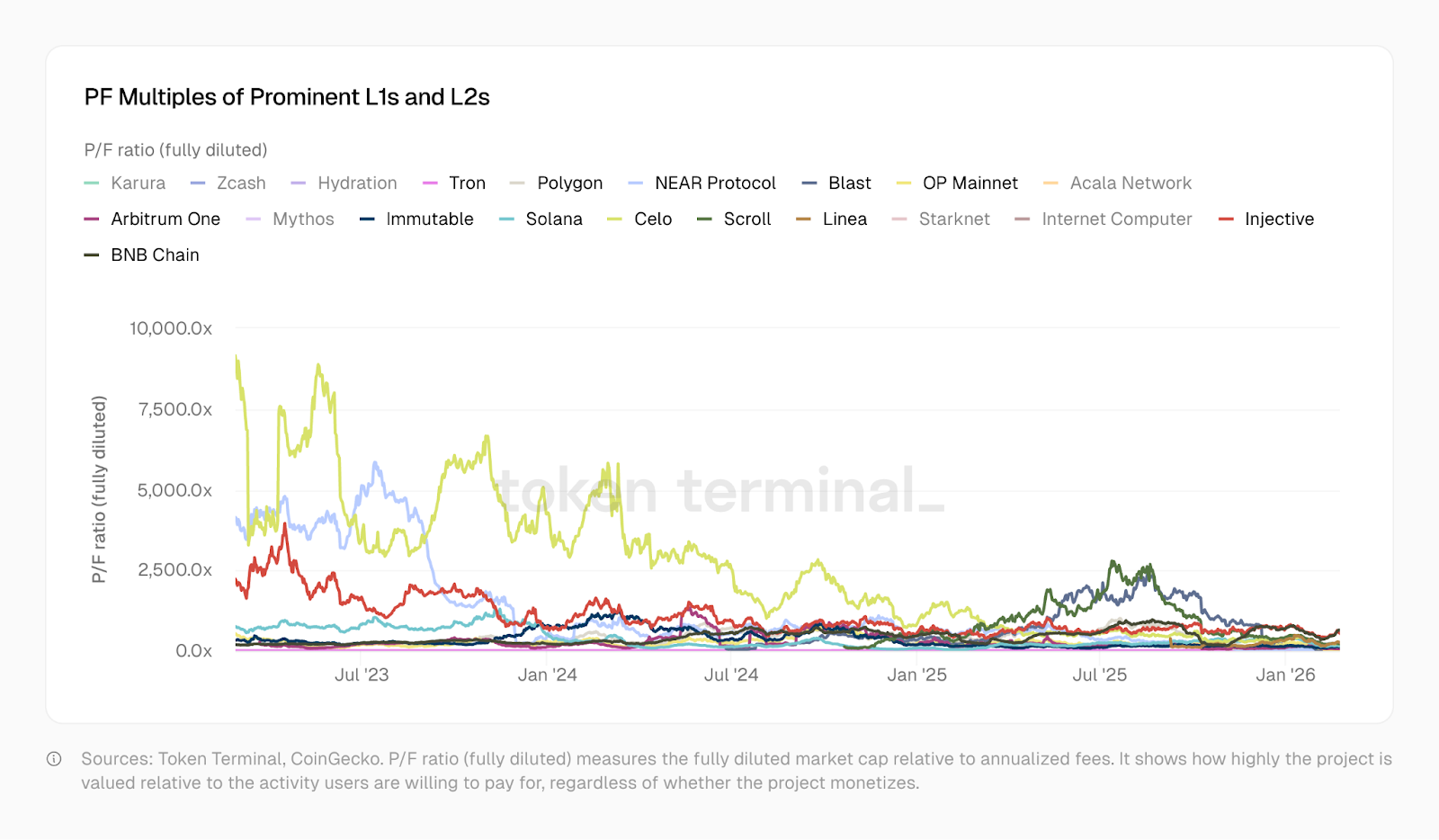

In January 2023, Optimism was trading at PF (price-to-fee) multiple of 465. Solana was at 706. Arbitrum and BNB were around 206. Today, Solana is at 138, Arbitrum is at 62, and OP is at 37. Polygon trades closer to a fintech company at 20. Tron sustains the stablecoin ecosystem and sits at a multiple of 10.2. Taken individually, Optimism, Solana, Arbitrum, and Polygon have enabled more sophisticated products in the years since. Each of them has more users, better liquidity and a more complex suite of financial applications built on top of them.

The discount in their price-to-fee multiples tells us about how the market perceives them.

Historically, L1s and L2s have traded at extreme premiums compared to standalone infrastructure or ventures. That premium, when invested well, could have created new economies. It could have funded developers to build real applications that mattered to real people outside our industry. Instead, the open-source nature of the products and the ease with which things could be tokenised meant we had fifty replicas of the same thing across thirty networks, with broken composability.

That was okay, because we had bridges. And cross-chain messaging. And countless other mechanisms to move money. All of which were now being valued at increasingly lower levels.

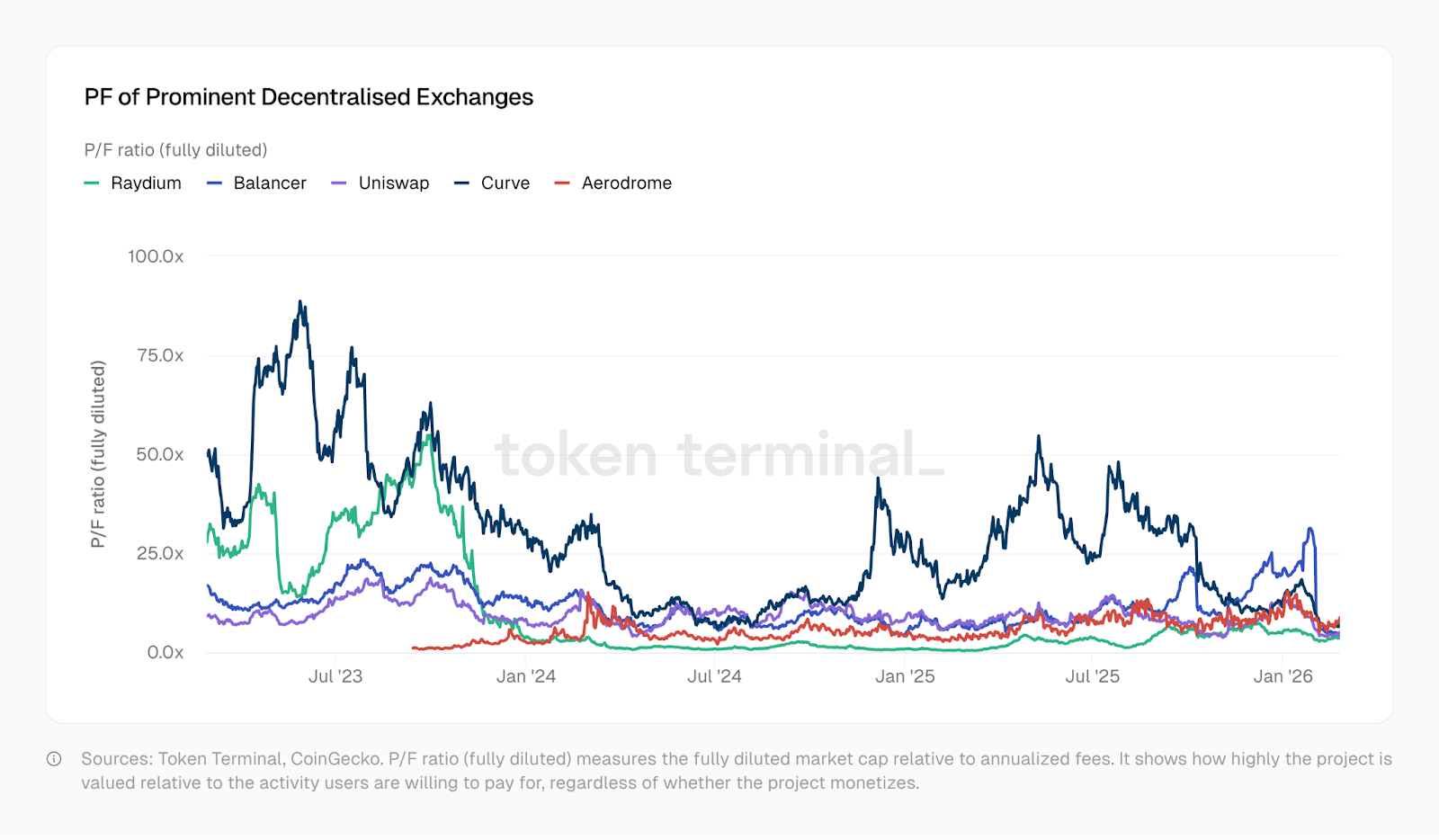

Consider the fate of DeFi primitives. Investor optionality and the lack of novelty butchered valuations, even when these primitives drove more economic activity. These are fragmented markets where investors have a multitude of choices to bet on. The novelty of being “decentralised” or on a blockchain has long since worn off. Kamino, Euler, Fluid, Meteora and PumpSwap have entered the chat - all at lower price-to-fee ratios than what protocols commanded in 2022. As the chart below from TokenTerminal shows, price-to-fee multiples of decentralised exchanges collapsed between 2023 and 2025. Some now trade at a multiple of 1.

In other words, the market values them below the fees they will generate over the coming year. A strange paradox is on display. Although the underlying protocols, be they DeFi primitives or the L1 itself, have trended lower in valuation, the apps built on them have generated more revenue over shorter periods.

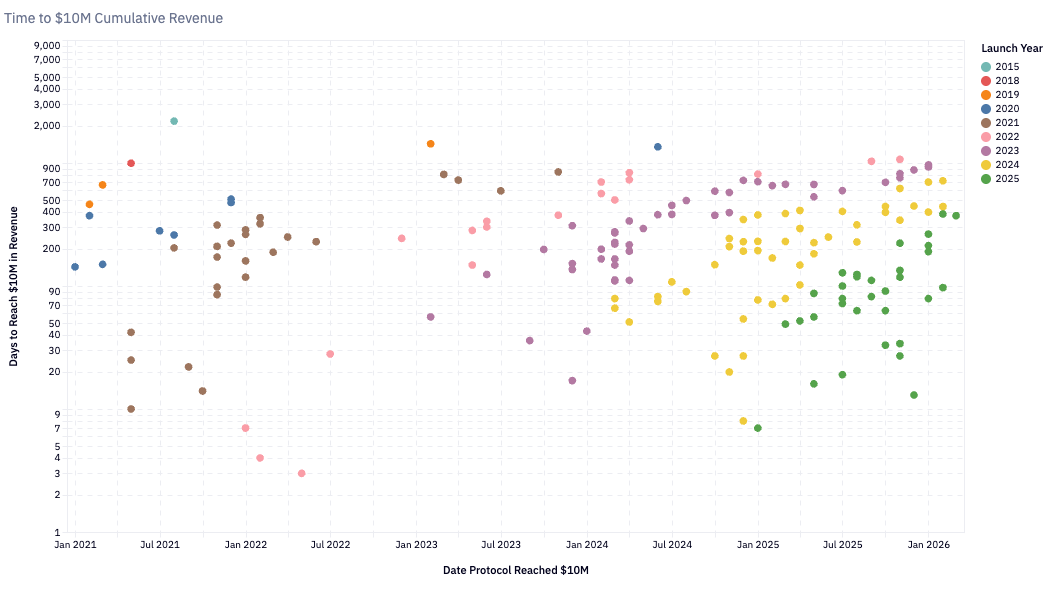

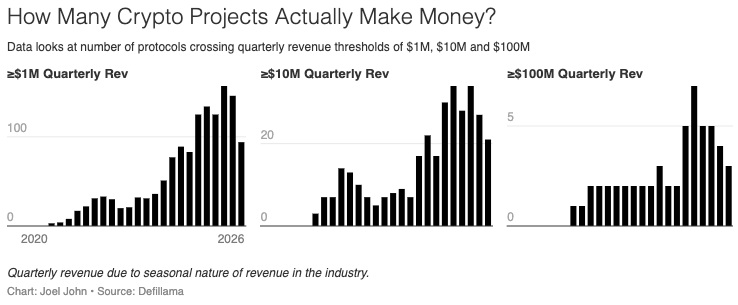

The number of teams doing over a million in revenue every quarter has steadily risen since the early 2020s. The figure is over one hundred. Protocols that took twenty-four months to reach $10 million in annual revenue in 2020 were considered fast. By 2024, protocols were reaching that milestone in approximately six months. Pump.Fun, launched in early 2024, reached $10 million in revenue in roughly two months, the fastest recorded trajectory.

This acceleration reflects both the maturation of the underlying infrastructure (faster chains, cheaper transactions) and the expanding pool of on-chain capital looking for yield and entertainment. If you’re a developer or a founder, consider the facts:

There are nearly 900 protocols generating revenue in crypto today.

Each of them competes for a smaller share of median revenue, but the broad arc shows more teams generating more revenue. For context, revenue-generating protocols grew almost eight times, from 116 to 889.

Median revenue has declined to $13k every month

Blockchain native businesses have three forms of moat. Each of which is evident when we study how revenue is made.

First Mover Advantages: The network effects that Tether and Circle gain from being early will be hard to replicate. They have been around through multiple cycles and are established duopolies, despite the emergence of new players. As it stands, these businesses are non-tokenised and hyperfinancial. Tether is a centralised entity whose revenue mostly comes from T-Bills.

Liquidity Moats: Aave has sustained liquidity depth across cycles in an industry where capital has historically been mercenary. Hyperliquid has replicated it, but it is too early to say. These protocols have an incentive to return capital to liquidity providers and tweak tokens towards governance.

Distribution Moats: Seasonal applications, such as meme-coin trading platforms, rely on capital velocity and consumer demand. Web3 games and NFTs stick here. AI-fuelled productivity would mean small, lean teams can now ship consumer-oriented products faster. Where does edge come from? It would boil down to onboarding and retaining the most users when markets are hot.

Products built on distribution moats can be tremendously valuable, but they are outliers and not the norm. A startup was traditionally valuable because its learnings could be replicated. Y Combinator works partly because of the lindy effects of the ideas that prevailed. Crypto evolves at a pace that is too fast for such Lindy effect learnings to be instilled. This is partly why we do not see founders replicate their success in consumer products as a category. The seasonality that helped scale a venture in the first place may not replicate itself.

That is not to suggest founders should not pursue the opportunity. Segments such as prediction markets or data providers for agentic-economy products may generate a great deal of cash flow in the short run. It is just pertinent to understand that they are high-velocity, short-term games that may not last. The trap for such product categories is in needlessly raising venture capital or being stuck with a token issued long after the meta that enabled the product in the first place dies.

What makes tokenised businesses valuable then? Are their valuations even justified?

The data offers some clues.

Questioning Governance

In 1999, many tech companies traded at a price-to-sales (P/S) ratio of 10x-20x. Akamai, a content delivery network, traded at 7,434 times sales. By 2004, Akamai had fallen to 8x. Many companies went from P/S of 30x-50x to less than 10x. The dot-com bubble burst evaporated trillions of dollars in speculative value. Yet many of the companies survived because the underlying businesses were real. Amazon fell 94% from its dot-com peak and went on to become one of the most valuable companies in history.

Crypto is going through the same compression, faster. In 2020, when DeFi was still an experiment, crypto generated just about $21 million in total annual revenue. The aggregate P/S across tracked protocols sat at 40,400x. The market was all about the future: “What could crypto be?” By 2021, as DeFi summer turned protocol revenue into real numbers, P/S collapsed to 338x. Today, with $18 billion in annualised revenue, it sits at ~170x. The compression from 40400x to 170x took five years.

However, there is a catch. When Visa trades at 18x, shareholders receive dividends and buybacks. They have a legal claim on the company’s earnings and a seat at the governance table enforced by securities law. When Aave trades at 4x, token holders have governance rights but, until recently, no direct economic claim on revenue. Hyperliquid uses its assistance fund for buybacks, making HYPE holders the closest thing to equity holders in DeFi. Aave approved a $50 million annual buyback programme in 2025.

These are meaningful moves, but they are exceptions. Across the broader market, most protocols lack a mechanism to return value to token holders. The multiples look cheap, but the rights attached to those multiples are thinner than anything in traditional markets. What makes these multiples possible is an industry that generates revenue at a scale and efficiency unlike anything in traditional business.

The protocols compressing crypto’s P/S ratio are not large organisations with thousands of employees. They are small teams running global financial infrastructure with near-zero marginal costs and no physical footprint. How thin can those costs get? And how much will holders trust these teams with doing the right thing with protocol revenue?

Segregate the market by sector to get a much better picture. Aave, the largest lending protocol in DeFi, trades at a P/S ratio of roughly 4x. Hyperliquid, which controls ~80% of the decentralised perpetual futures market, trades at roughly 7x. These are not bubble multiples. Arguably, they are lower than their closest traditional comparables. Coinbase, the only major publicly listed crypto exchange, trades at roughly 9x revenue. CME Group, the world’s largest derivatives exchange, trades at ~16x. Visa, the gold standard of payments infrastructure, trades at ~15x.

Will Clemente mentioned on our podcast that crypto is the purest form of capitalism. In no other industry do successful businesses achieve profit-per-employee numbers that approach Tether’s estimated $100 million. To put this in perspective, Nvidia generates $5.2 million in revenue per employee, Apple generates $2.4 million, and Google, $2 million. Tether, with 125 employees and roughly $12.5 billion in annual revenue, operates at a scale that suggests the highest profit per employee in corporate history.

Despite the crazy 170x P/S number, the market is not irrational about the protocols that actually generate revenue. It prices them at or below traditional financial infrastructure.

Which leads me to the next question - what even is the use of tokens? In many categories, tokens are powerful instruments for coordinating capital towards a shared vision. Crypto is in this phase where entrenched duopolies are the norm. Traditionally, a founder had to take debt (against equity) or raise money to infuse capital for financial products. Hyperliquid, Uniswap, Jupiter, and Blur are proof that, with token incentives, individuals will allocate capital to new products. The same individuals could contribute substantially when tokens have governance rights attached. In this regard, tokens may evolve to serve two functions.

Firstly, to coordinate capital and resources from the right kind of individuals

Secondly, to empower them to govern a protocol.

Tokens on their own are no longer valuable. Even equities are tokenised now. These instruments will need to have claims to economic activity and the ability to guide governance. Many Layer 1 and Layer 2 tokens struggle to deliver on either. Teams and VCs often hold the bulk of the token, leaving holders in disarray. It leaves no reason for the marginal person to care about newly listed digital assets.

Today, these experiments are split. MetaDAO allows holders to receive a full refund of their investments if teams make false representations. There are no large protocols on it yet. Crypto’s core reckoning is that tokens have traditionally given holders few rights. Protocols are now trying to answer the age-old question of why anyone should hold these instruments in the first place. In a future issue, we will explore the correlation between holder rights and valuations.

The Fork In The Road

Capital markets have become more intertwined over the past two decades. Much of it can be attributed to technological improvements. We can trade commodities, foreign indices, digital assets and even compute (GPUs) in the near future. Blockchains have made it possible to trade these markets globally, at all times. The fact that Nasdaq and NYSE are now trending towards 24/7 markets is an instance of a technology changing the zeitgeist.

We live in a hyperfinancial world, where ironically, news of war has us scrambling to figure out which prediction markets are the best to bet on.

For founders, that means rethinking what they build and how they build it. If the data here makes anything apparent, it is that all blockchain products eventually monetise through two core maxims.

Through taking a small cut of high-frequency transactions or

Taking a large cut of transactions where verifiability and trust assumptions matter

The edge is either in velocity or verifiable transparency.

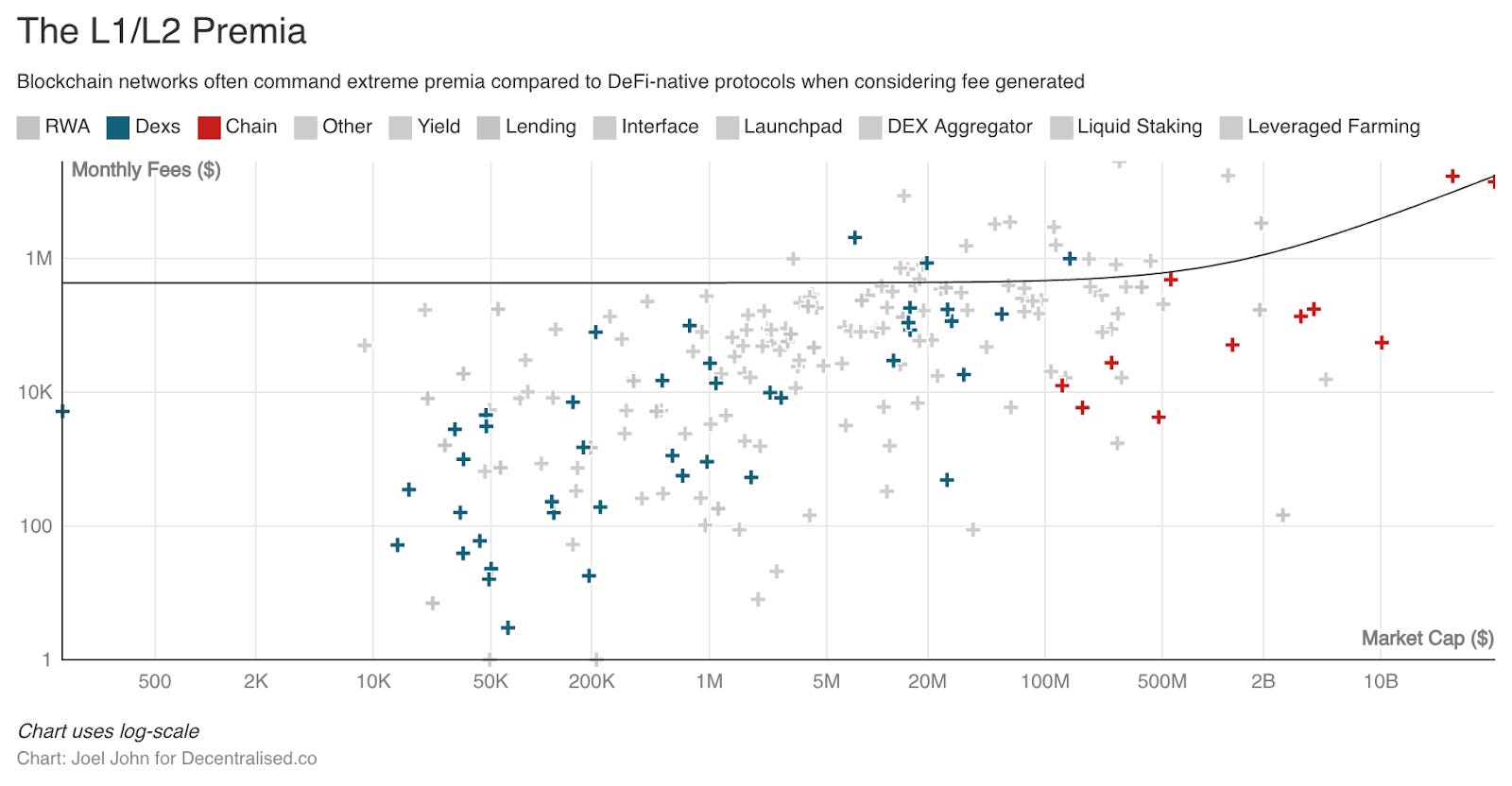

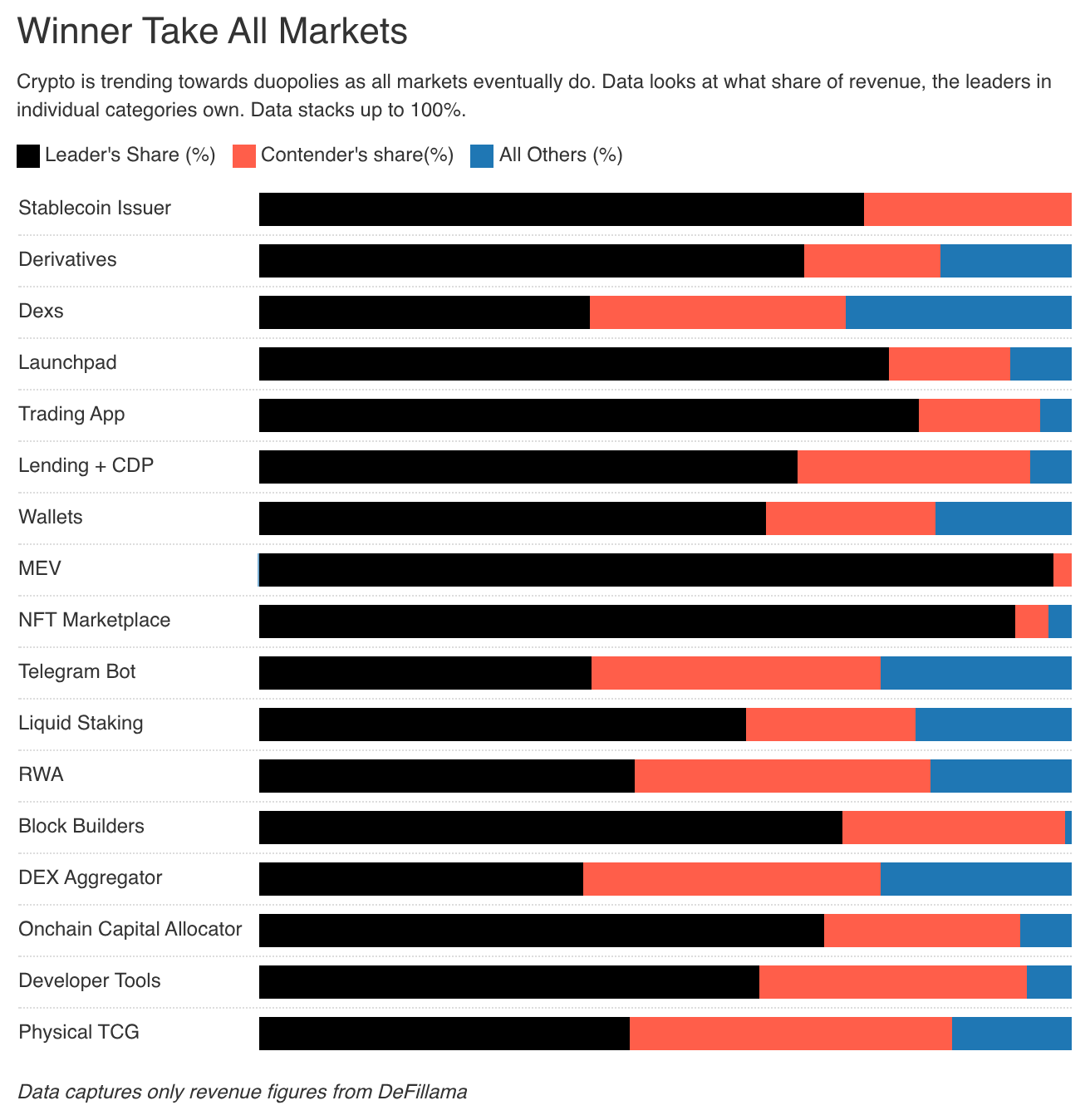

Profit motives are the purest incentives for participants in the capital market. There is a core belief that eventually, markets trend towards extreme efficiency. We see versions of this with categorical leaders. That chart where we saw 70% of multiple segments being owned by two key players? That is a brutal aspect of life and markets we all grapple with. What this means for founders is that the capital that once went towards their token is now redirected to assets with higher volatility or higher returns on capital.

Long-term capital exists, and may even pay a premium, but only if it values the underlying business. Investors in Google and Amazon did not have to scramble for the exits because the underlying businesses were valuable.

In an age where the value of software itself is under question, blockchain native apps will have to find new ways to be valuable. We can restructure tokens. Perhaps, we could even make start-up equity tradable on-chain. But this is not just a token problem. It is a business model problem, too. The vast majority of long-tail blockchain applications - like Web3 social, identity and gaming products have struggled to see scale or meaningfully differentiate from their traditional counterparts. It is not that those experiments were not valuable. It is that we struggled to monetise them effectively.

The infrastructure age of crypto is behind us. What lies ahead is a period when it blurs with the Internet. Nobody talks about an “online” business anymore; you simply exist on the Internet. Nobody is a “mobile app developer” anymore; you are a developer.

Long live the age of the blockchain enthusiast. We are simply ledger maximalists wondering what the best use of these ledgers is.

Craving a good shawarma,

Joel John

P.S - I wrote this piece, part monitoring drone hits on the town I call home - Dubai. There is a silent resilience in continuing, even when it may seem as if the world is coming to an end. A rebellion in its own right. Many founders in crypto are displaying the same resilience. If you are still here and building, we’d love to chat and see how our data and learnings could be put to use in building scalable protocols.

Research here is guided by data from DefiLlama, TokenTerminal, Codex, Santiment and a mix of traditional data vendors.

The upshot of all this right is the weird and wild times are basically over and crypto is just sort of going to wire in with everything else and become as boring as the internet itself.

Bitcoin will always be there for the cowboys to ride away into the cypherpunk sunset on — but there will be fewer and fewer cowboys until eventually there are none. The days of the hype and the weirdness and the memes are all gone or at least going.

Before long it will be platformified, tamed and probably governed by algorithms, just like speech is online.