Why We Invested in Drift Protocol

Going Long Solana's Perpetuals Ecosystem

TL;DR: Decentralised.co is increasing its exposure to perpetual exchanges through a position in Drift Protocol. Solana is yet to benefit from positive tailwinds in the growth of perpetual exchanges. Drift is best positioned to benefit from RWA assets and internet capital market instruments issued on Solana. At a price-to-earnings multiple of five based on last year’s earnings, it is deeply discounted relative to its position in perpetual exchanges.

This brief note should help explain why we are going long on the long-standing perpetual exchange in Solana. Venture@decentralised.co is the best place to reach out if you are building in the theme, and would like to chat.

Over the past month, we built a position in Drift. The protocol generated $19.8 million in fees over the last year. It currently trades at an FDV of $95 million. At the same time, it sits at a price-to-book of 3.5x on its operational balance sheet alone. We believe Solana will continue to be the chain on which fintech applications are built and scaled. Drift is the longest-standing perpetual exchange within it. These two forces blend to make it an interesting asset to own. Our primary reasoning for involvement with Drift boils down to three core factors.

Drift’s team has worked relentlessly towards scaling perpetuals on Solana. We are comfortable going long on the team itself.

Drift’s architecture for providing liquidity will become valuable in a world where centralised sequencers are seen with suspicion. DLOBs, JIT, and vAMM collectively offer a better experience to end users. Open, verifiable markets will be a necessity as on-chain markets evolve.

The DeFi landscape on Solana has significant runway for growth in equities, real estate assets, and internet-native capital instruments. A perpetual exchange will be needed for sophisticated actors to interact with these instruments. Drift can be the preferred avenue for price discovery and hedging.

To keep terminologies tight, we use the following throughout this note.

Earnings - What is left in the protocol’s balance sheet after cost of incentivising economic activity

Revenue - Total dollar value made by protocol and users

As a general heuristic, we use price-to-earnings throughout much of the document, except in the initial section.

Before getting into the why for Drift, it helps to understand how its fundamentals stack up.

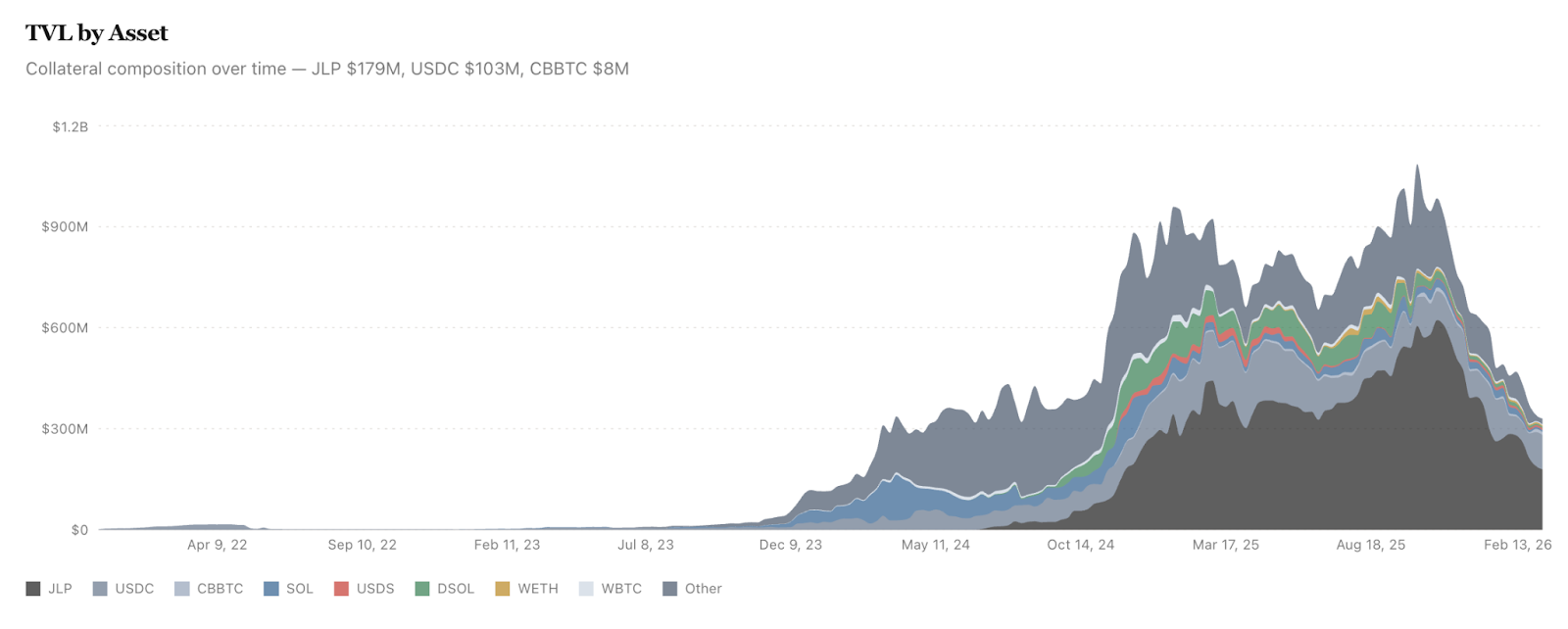

Drift Protocol is the longest-standing perpetual exchange on Solana. It currently holds a quarter of all TVL allocated to perpetual exchanges on Solana. Its yearly revenue grew by 193% in 2025, from $14 million to $41 million. Annualised, in 2026, the protocol is on pace to generate $30.75 million in revenue, extrapolating from what the protocol made in January and February. (Revenue here combines fees paid by users alongside staking rewards from Drift-staked-Sol). Drift holds $27 million in its fee treasury accumulated entirely from protocol earnings over four years, excluding the $52.3 million raised from investors.

Perpetual exchanges are booming as a category, but they are not entirely open, verifiable, or decentralised. Part of our interest in Drift comes from its open-source nature and direct settlement on Solana. But before we go into how it operates, it helps to have a perspective on why open, verifiable financial networks matter.

Open Markets Need Verifiable Infrastructure

Human institutions work well during periods without stress. A dictatorship can be more efficient than a democracy until the citizenry questions those in power. People think about the mechanism that elects someone to power only when the power is abused. The same applies to markets. We don’t often think about how a market functions until something breaks. Markets, like democracies, are bundles of rules that must function in sequence. When the rules are not followed or broken, trust in the market declines. And a byproduct of that is citizens (or traders) simply moving elsewhere.

This is why trustlessness is a fundamental need for markets to evolve. Bitcoin serves this function for spot assets. AMM model markets on Ethereum and Solana solve this for spot markets. The fact that we know how much money is lost to MEV is a feature that happens because the rulesets and infrastructure through which a spot order is settled on-chain are verifiable. Perpetual exchanges currently do not have that verifiability or decentralisation. We have accepted centralised sequencers as a default for perpetual exchanges as a trade off for speed.

Open source, verifiable markets built on public infrastructure will be tremendously valuable as the world’s assets settle on-chain. To understand why, it helps to have a perspective on what happens when markets are walled off and centralised.

The London Interbank Offered Rate Scandal

LIBOR was a benchmark rate used to determine the cost at which banks paid to borrow from one another. It was determined through collecting lending rates from individual banks who in turn submitted data without verification. Since there was an active derivatives market to trade these rates, traders at banks were incentivised to provide faulty data or collude to manipulate the benchmark and profit off the derivatives. In 2012, Barclays paid $453 million to settle the allegations. Part of the reason the scandal occurred was that centralised parties (the traders) had incentives large enough to abuse the system through a liquid derivatives market.

The equivalent of a LIBOR cannot happen on Aave because the lending rates are open and verifiable. The lending rates are not set by individuals, but rather by supply and demand. Anyone can audit the numbers at any time, since there is no central trader providing these rates. The blockchain provides records that cannot be falsified.The Nickel Squeeze of 2022

In 2022, as the war between Ukraine and Russia raged, the nickel markets began acting strangely. Nickel futures jumped 250% between March 4 and 8 that year - going from $25k to $100k per ton on the London Metal Exchange. A large entity (named Tsingshan) had short exposure that would have resulted in it owing $15 billion to multiple large banks. The LME (London Metal Exchange) had visibility into only about 20% of the entity’s nickel short exposure, as much of it was in OTC transactions.

To avoid losses from Tsingshan taking down the entire market, the LME suspended trading on March 8th, wiping out $3.9 billion in transactions. The market lost its integrity and shattered the trust people placed in it. 145 years of reputation, lost on a March morning.

Libor was about rate-setting collusion. LME’s situation was a byproduct of a lack of visibility into where the exposure lay. Both instances were fuelled by the lack of transparency in financial markets. Perpetual exchanges face a similar vulnerability to centralised sequencers, which create opacity around order fulfillment.

Verifiable infrastructure is a market necessity, not an option.

Today, regulators can audit and verify these markets. But it requires human intervention, and even when the regulator is involved, there can be slip-ups. Bernie Madoff’s scheme was known to the SEC as early as 1999. The point of introducing technology in these markets would be to avoid requiring individual regulators to verify, and instead have a steady stream of audits every block.

When market infrastructure (like the NYSE) can reverse transactions, it gives undue power to a handful of people who can hurt retail investors and hedge funds that are on the right side of trade. These exchanges are themselves at risk, as they often lack visibility on the complex OTC transactions market participants engage in. Blockchains provide mechanisms to solve all three problems.

They bring radical transparency through making it considerably easier to verify and vet where exposure stands.

The immutable nature of a blockchain ensures transaction finality. Settlement finalities are a guarantee unless the network forks.

They allow participants to verify and vet how orders were sequenced to ensure fairness in the system

Perpetual exchanges in crypto are not entirely open and verifiable. Many of the largest names have centralised sequencers whose order sequencing logic and history cannot be verified. As our markets turn increasingly reliant on blockchains for settlement, there will be primitives that aid in making markets open, verifiable and trustless. Part of our interest in Drift emanates from this view. Unlike many of its peers, the way it sequences orders, its codebase, and its liquidity sourcing can all be verified. Besides, within the mix of assets one can pick within Solana, Drift is mispriced for the traction it holds

Understanding Solana’s Perpetual Ecosystem

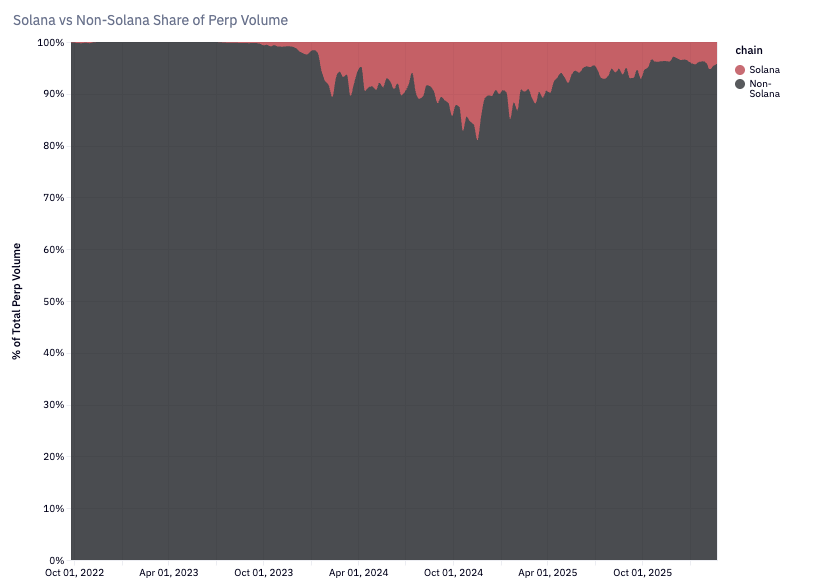

Solana accounts for less than 5% of all perpetual exchange volume. On an average day, 60% of its current activity is on Pacifica. Solana’s early foray into perpetuals did not go quite well. Mango Markets was exploited early on. The FTX crash left a nascent DeFi ecosystem bleeding. Much of the activity on Solana in the quarters that followed was in the spot market. This is where players like Jupiter, Meteora, and PUMP earned their mettle.

Hyperliquid, in contrast, focused on the perpetual meta aggressively when it launched. It listed meme asset perpetuals faster than centralised avenues did, thereby attracting a core subset of retail users. Combined with marketmakers that benefited from the exchange’s faster settlement times, this created a nascent but healthy ecosystem. It set the stage for what we know as the decentralised perpetual ecosystem. As of writing, Hyperliquid accounts for ~30% of all volume on decentralised perpetual exchanges, compared to ~5% on Solana.

Jupiter is a leading contender for perpetual products on Solana. It is hard to compete against the network effects the protocol has from its multitude of products. It has also issued JLP - an index instrument that represents BTC, SOL, and a mix of stablecoins. Jupiter’s higher TVL and take-rate make it interesting, but a bet on Jupiter is a bet on a generalist that has too much to do. We had earlier explored Jupiter in this article.

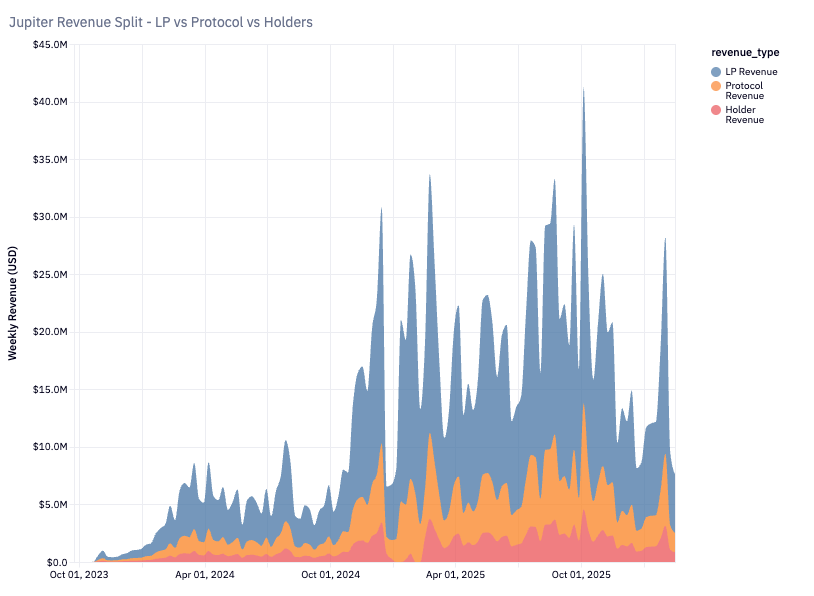

Jup has generated over $1.2 billion in fees from its perpetual product alone. The challenge is that much of the fees go back to liquidity providers on the exchange. Jup’s token model passes on fees in the form of USDC in yield back to token holders. 66.7% of fees generated on Jupiter go back to liquidity providers on JLP. Think of this as the cost of capital for TVL on Jupiter’s exchange. The product has capital density but pays a heavy premium for it. 22.2% of the fees go toward the protocol, and the remaining 11.1% is distributed to users as staking yield. So even though the perpetuals product generates a lot of fees, much of it is not captured or reflected in the token.

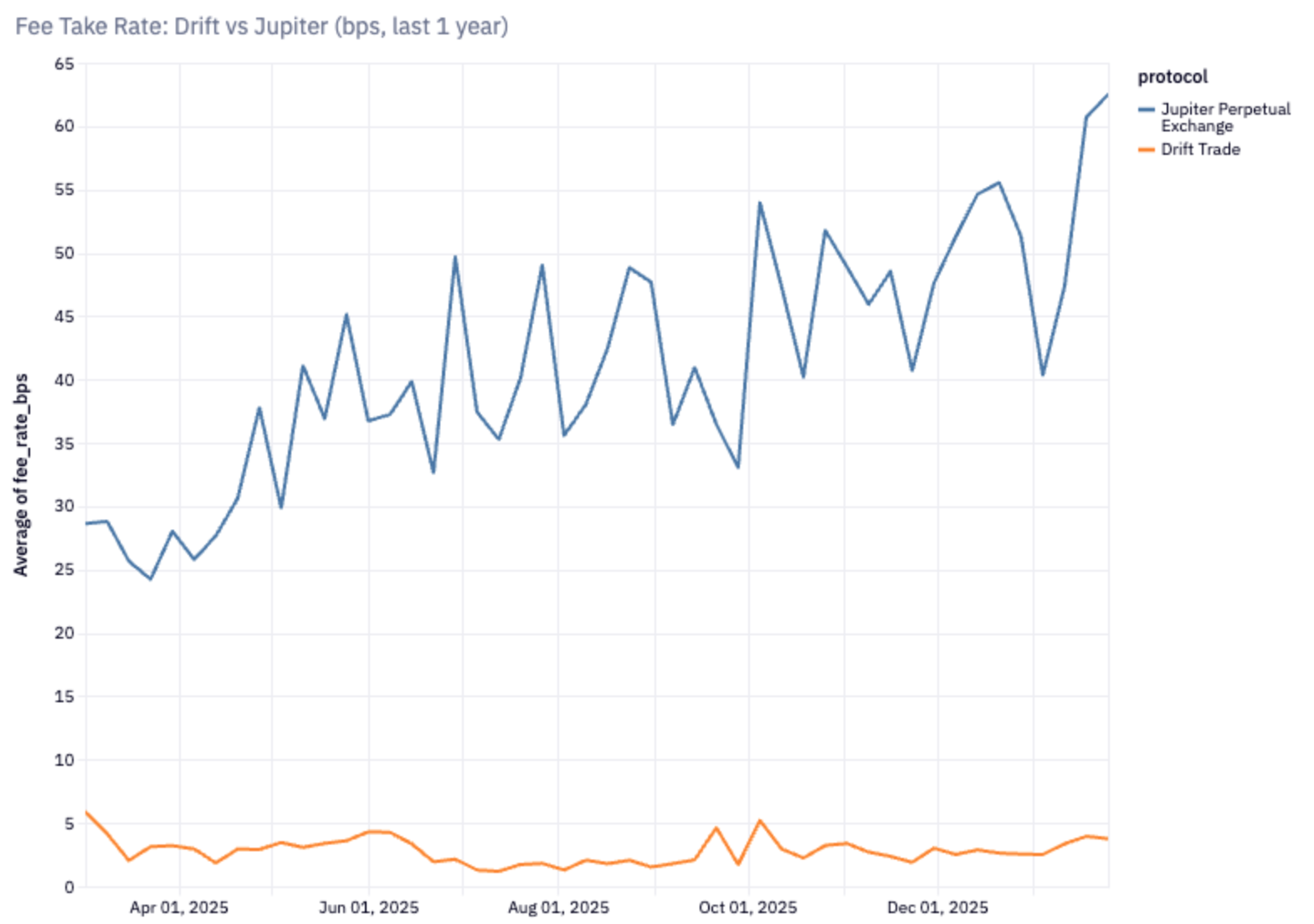

A different way to see it is through the lens of take rates. As seen in the chart above, Jupiter’s take rate on its perpetual exchange is 16 times what Drift charges. This is both a feature and a bug. Jupiter’s fee rate steadily climbs due to its linear pricing mechanism for its perpetual exchanges. Large orders that move markets tend to pay more. It is a good strategy as the exchange has made verifiably more than Drift in the past year. For large institutional traders & high frequency traders, the model will simply be ineffective as pricing cannot be predicted.

The parallel here is that of Google and Yahoo in the early 2000s. Yahoo branched out to multiple product lines considerably before Google did. The former focused on its core business (advertising) before expanding into email (Gmail), streaming (YouTube), and operating systems (Android). Yahoo expanded early through costly acquisitions like Geocities and Broadcast.com, but struggled to integrate them into its core business. Google focused on search and kept the product simple, as that is what the users wanted. Today, close to 80% of Google’s revenue is its core search and advertising business. Another 11% is from its cloud business. Only 9% of its revenue comes from the expanded product line.

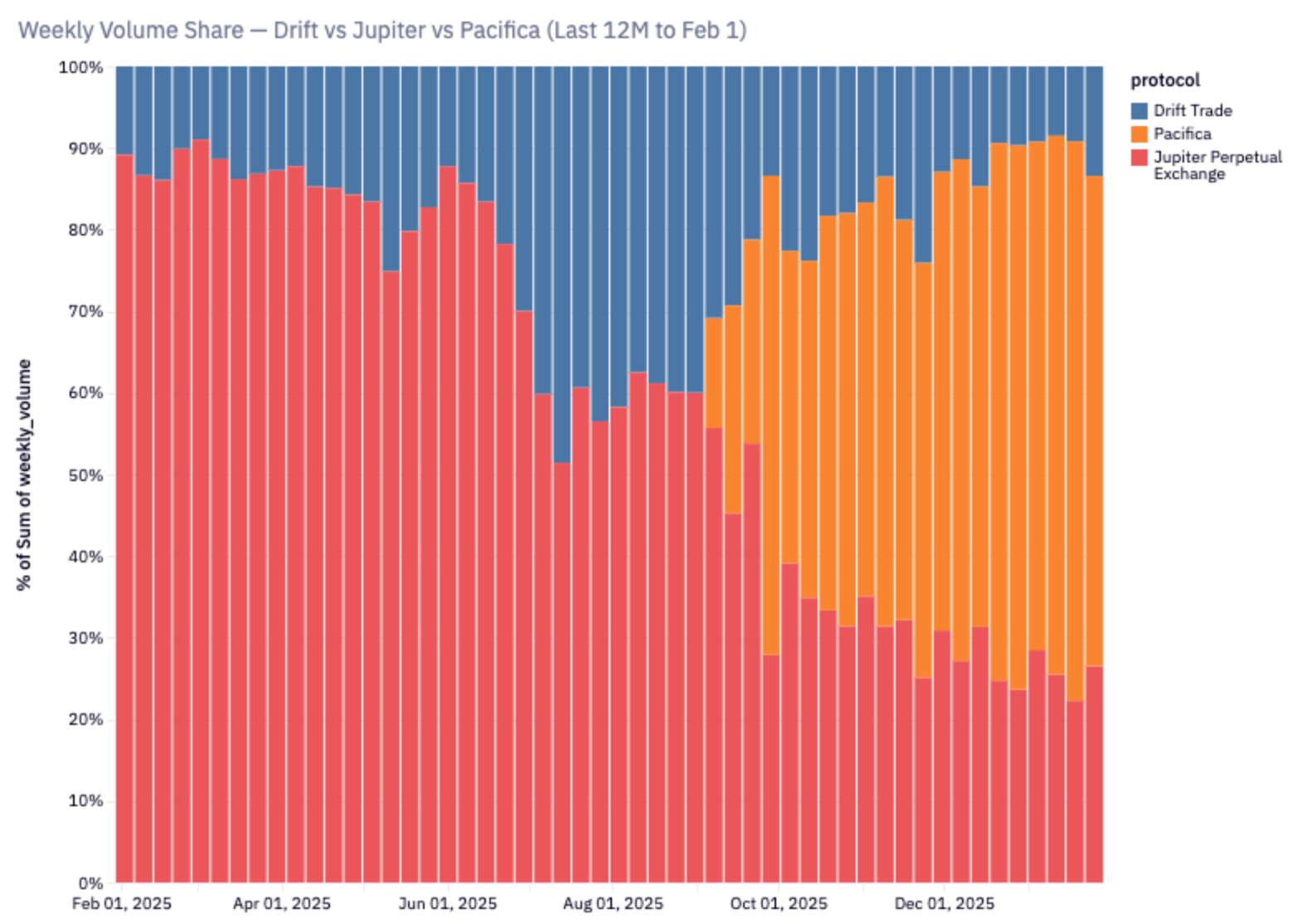

Pacifica is the new upstart on Solana that has seen more trading volume than both Jupiter and Drift. Despite being in closed beta, the product generated over $6.7B in volume, compared to Jupiter’s $3.3B and Drift’s $ 1.4B. It accounts for nearly 60% of the total volume in Solana’s perpetual exchange ecosystem. However, there are two key concerns. Firstly, it has a centralised sequencer that is neither open nor verifiable. Secondly, the liquidity model used is that of a CLOB. If we were pursuing a native CLOB exchange, our bet on Hyperliquid would already cover that side of the market. Between these two points of friction and the fact that Pacifica does not have a liquid token, we had to explore further.

For us, the composability, verifiability, and openness of Drift is worth a premium.

Jup, Pacifica, and Drift are three entirely different products when it comes to perpetual exchanges. For JUP, the perpetual exchange is an extension of their product suite, and the fee model is optimised towards yield. For Pacifica, the focus is on being a CLOB product that is at parity with centralised exchanges. For Drift, the focus is on composability, verifiability, and openness. We go deeper into Drift because of how its liquidity model could scale, as the mix of asset types on Solana evolves from where the ecosystem is today.

Where Drift Differs

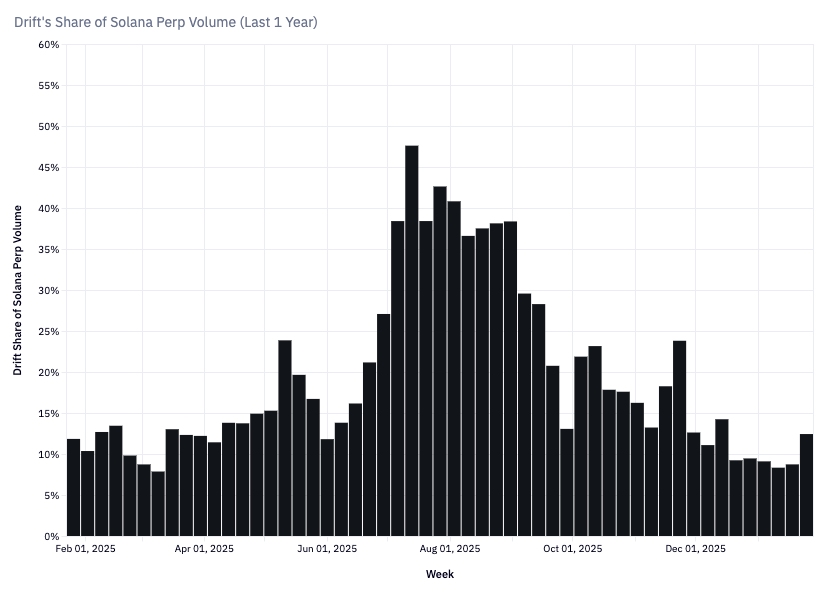

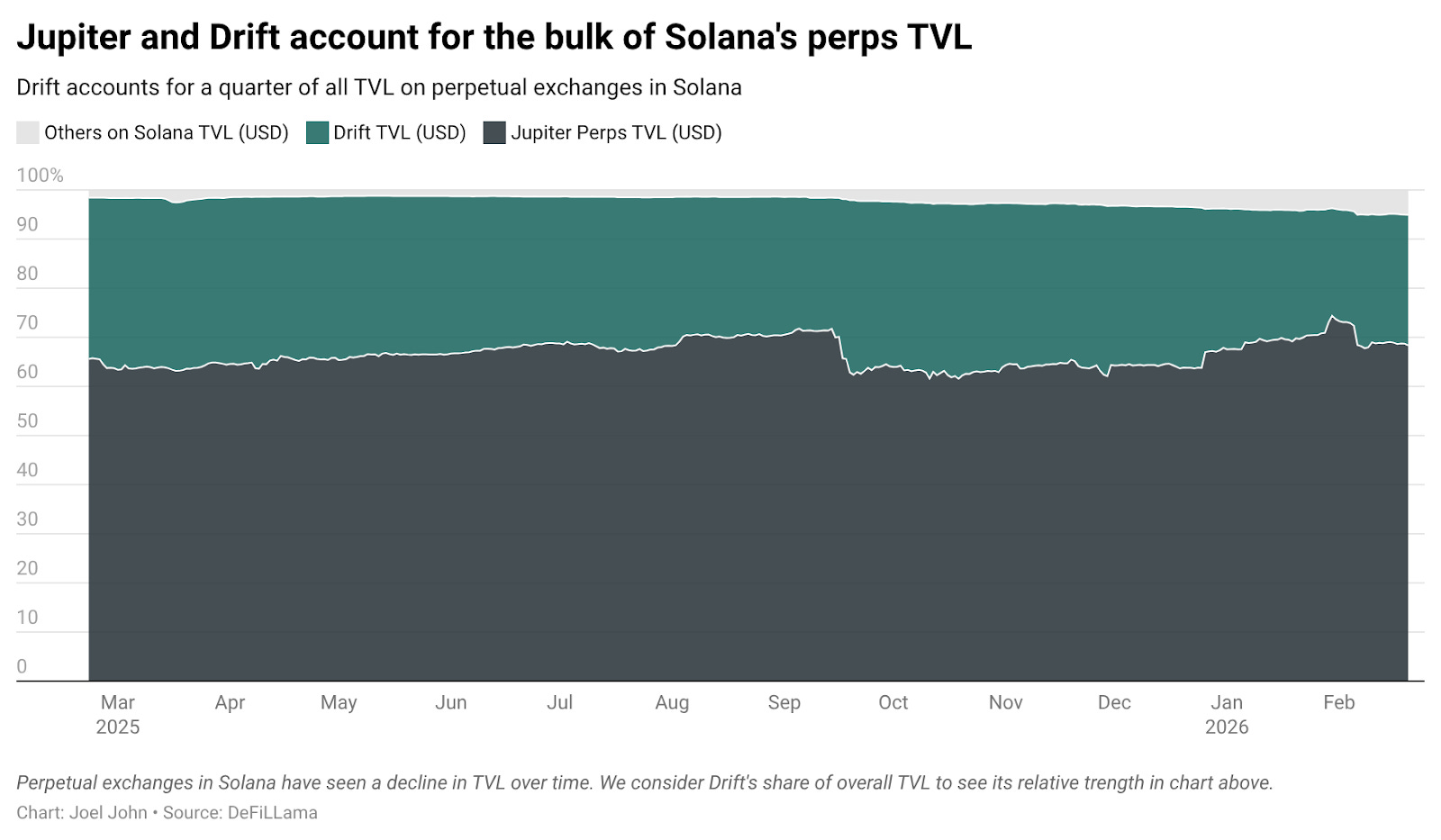

Drift is a perpetual exchange focused solely on improving infrastructure for margin trades and can iterate faster than an aggregator. The market tends to discount Jupiter for such reasons. Drift is also home to the second-largest TVL among perpetual exchanges. It holds close to 15% of all TVL committed to perpetual exchanges across all chains.

Drift has not seen meaningful competition from the emergence of other perpetual exchanges on Solana, either, until Pacifica came. Jup and Drift collectively own 95% of the TVL in perpetual exchanges. Drift’s share has stayed steady over the course of the year.

Drift trades at a $95 million FDV, compared to Jupiter’s $1.05 Billion. Core to our thesis on Drift is how its liquidity model works. Conventional exchanges (like Hyperliquid and Pacifica) follow a centrally sequenced CLOB model (CLOB stands for central limit order book). The exchange holds the power to determine how individual transactions are ordered.

In traditional markets, having the power to outrun the way orders are routed to an exchange is a multi-billion-dollar endeavour. Flash Boys by Michael Lewis famously exposed how a handful of firms had an undue edge through latency arbitrage. While CLOB-based models are necessary to compete with CEX-like features, the cost is a lack of verification and real-time settlement.

This is where Drift’s liquidity model becomes interesting.

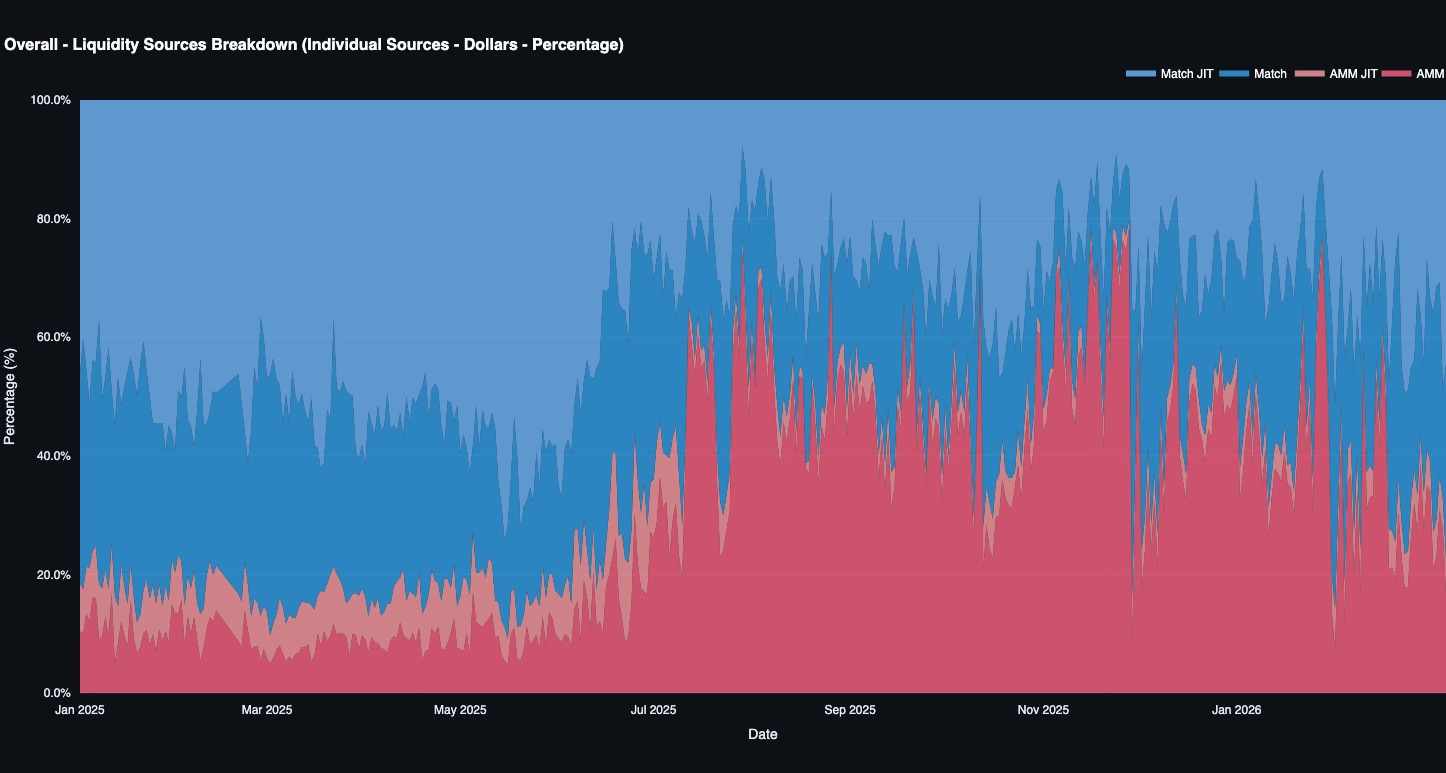

When a user sends an order to Drift, the order routes through three forms of liquidity.

A Just-in-Time Auction

A Just-in-Time Auction Orders on Drift has a 5-second phase during which multiple market makers can competitively bid to fill an order. This is similar to the RFQ system we had written about bebop here. RFQ systems benefit consumers by enabling large orders to be competitively bid among multiple parties. It helps a market-maker, as they have the option to avoid toxic flow and reuse idle assets in external venues where they could be more productive.

In a CLOB model, consumers see the price and spread they could expect. A JIT model can absorb more in both volume and size at tighter spreads, even when the order book does not appear highly liquid. The downside of such a model is the time it takes for orders to settle. Both market-makers and traders are ultimately settling on Solana, so there will be an infrastructure bottleneck.

The other assumption required for this to work is that a multitude of market-makers want the order flow from such an auction. If competing platforms offer points or rebates alongside high amounts of volume, market-makers may have little reason to bid on Drift’s JIT auctions.

A DLOB maintained by keepers

If no market-maker bids on the order, a network of keeper bots financially incentivised by Drift can place bids. Rebates from Drift’s trading fees are passed on to keeper bots. Individual keepers are similar to brokers on the NYSE. Except that each of them can verify and maintain their own version of the orderbook permissionlessly. Everyone keeps a copy of the orders, open for anyone to verify.

A decentralised limit order book orders transactions by price, age, and size. When trigger conditions are met, the bot fills the order, depending on how it is configured. Drift - the protocol itself does not dictate how orders are sequenced. Everyone has a copy of the ledger because orders are settled on Solana.

Individual keeper bots have the ability to arbitrage against third party venues or trade among themselves to give the trader a bid. Their primary role is to keep a record of all orders. The DLOB keeper bot model is open-source. Anyone can spin up their own bot, run it, and thereby verify any of Drift’s claims. Verifiable.

A Virtual AMM

In edge scenarios, market makers can simply choose not to bid (in JIT), and keeper bots can avoid providing liquidity. This is what usually happens on days when liquidity cascades take markets down. Given that, in CLOB models, liquidity is a byproduct of humans (or APIs) providing it, traders can be left without a guaranteed bid. Drift’s approach to the problem is to provide a virtual AMM pricing model (similar to Uniswap’s) that uses user collateral and protocol balance sheet assets (liquidity provider deposits and the insurance fund).

It ensures that there is always a bid for traders, although spreads may widen and slippage increase. This has proven to be effective in scenarios where auto-deleverage kicks in and liquidates users on a CLOB-based market.

This aspect of Drift is currently underpriced by the market. Most exchanges that operate on CLOBs offer instantaneous settlement on the underlying network, but the order sequencing itself is neither verifiable nor composable. The use of perpetual exchanges cannot occur without infrastructure that is scalable and verifiable. Drift’s core architecture can deliver on these promises while incurring some sacrifices in settlement time.

As real-world assets like gold, equities, and commodities come on-chain, markets will prefer avenues that offer these benefits over recreations of the centralised structures that already exist. The ones that dominate CLOB models will be avenues that compete on liquidity, speed, and depth. All of those metrics are currently dominated by Hyperliquid. Drift sits on the other end of the spectrum, where a relative lag in an order going through is fine if the transaction sequencing itself is verifiable.

This positioning of Drift is tremendously valuable due to a few core factors that collide

New instruments on Solana are yet to scale. Internet capital markets in their current format are at best a meme. Startups and founders will raise capital on the network for longer-standing assets. MetaDAO is a sign of this shift. These instruments will need a perpetual exchange to enable a rich capital market. Lending needs hedging. Margin allows risk-on exposure. Spot trading allows a singular user persona

Real-world assets - like equities, foreign currencies, and tokenised real estate will increasingly come to Solana given its heavy retail-oriented user base and strong developer base. These markets will need a decentralised avenue to hedge. Composable workflows, such as taking a loan in USD and hedging against currency risk on a perpetual exchange, do not exist yet. Drift will be able to capture a reasonable share of this market.

Commodities - like gold, silver, and platinum are yet to find a market (of scale) on Solana. Decentralised.co’s own portfolio company (Orogold) is working on the problem. If commodities are to scale on-chain, market makers will need an avenue to hedge exposure with minimal risk on the same network. This is where Drift can play a role.

Ultimately, Solana benefits from a healthy ecosystem of traders, developers, and capital allocators that seems to be struggling to find a shared language for discussing risk. Perpetual exchanges are that language. Drift is where the language is spoken.

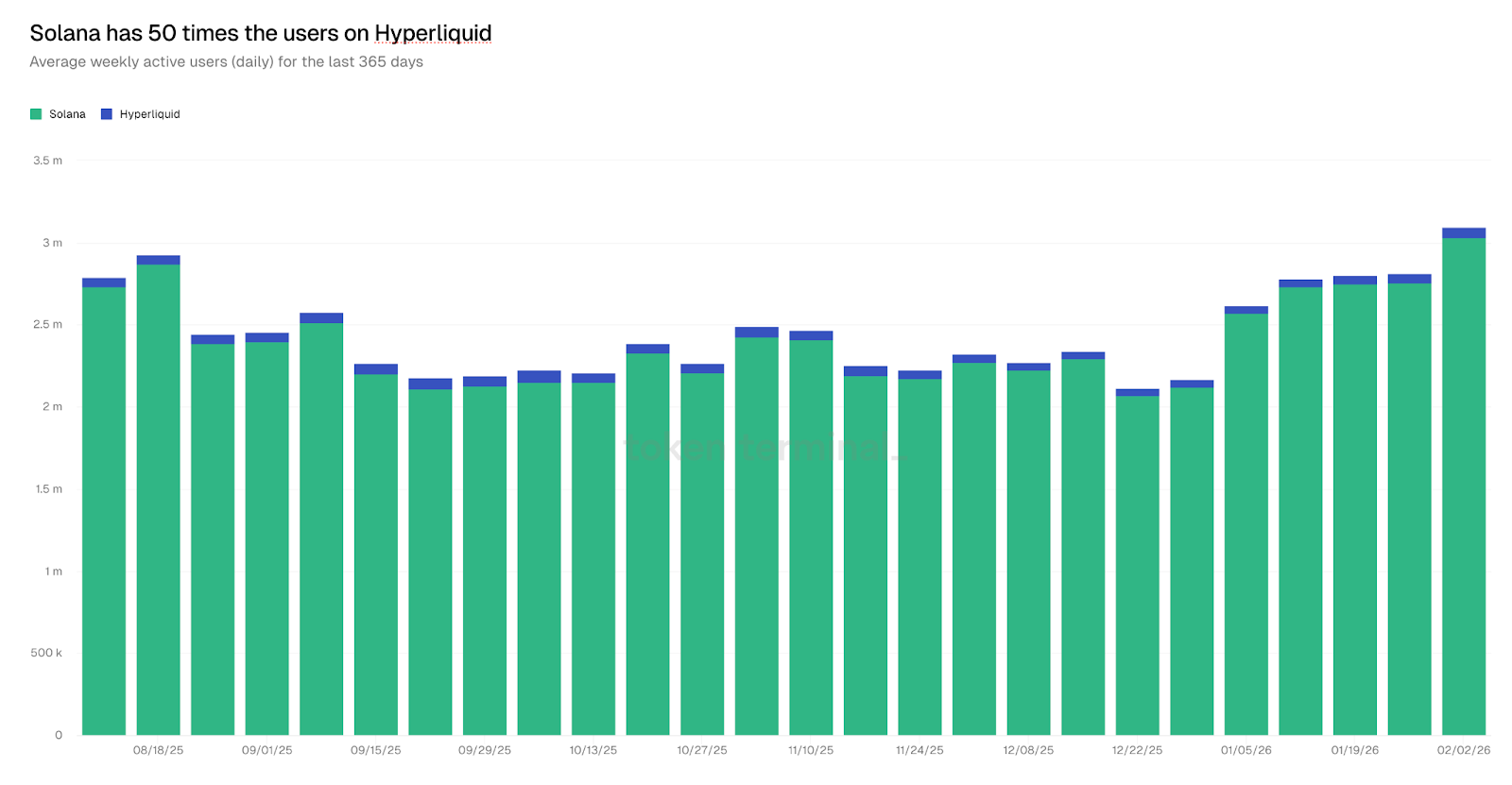

One way to see Drift’s potential for growth is by comparing Solana’s active user base with Hyperliquid’s, as shown in the chart below.

Assuming even 2% of Solana’s existing user base turns to Drift Protocol as users, the number of active traders on Drift will be in parity with what Hyperliquid has. When new primitives launch, they generally focus on a single application. Hyperliquid focused on trading for over a year before enabling lending. But the core user base of traders does not need lending at scale. The broader ecosystem within Hyperliquid struggles to capture the core users who came there to trade.

Drift, in contrast, benefits from Solana’s varied user base.

Solana users have the choice among NFT collections, gaming, or payments, and a meaningful share of them will find themselves on Drift. The exchange benefits from the organic, cross-category demand that a single-purpose chain may not see. This assumption, however, requires the asset types on Solana to evolve beyond where they are today, from meme assets to primitives that enable capital formation at scale.

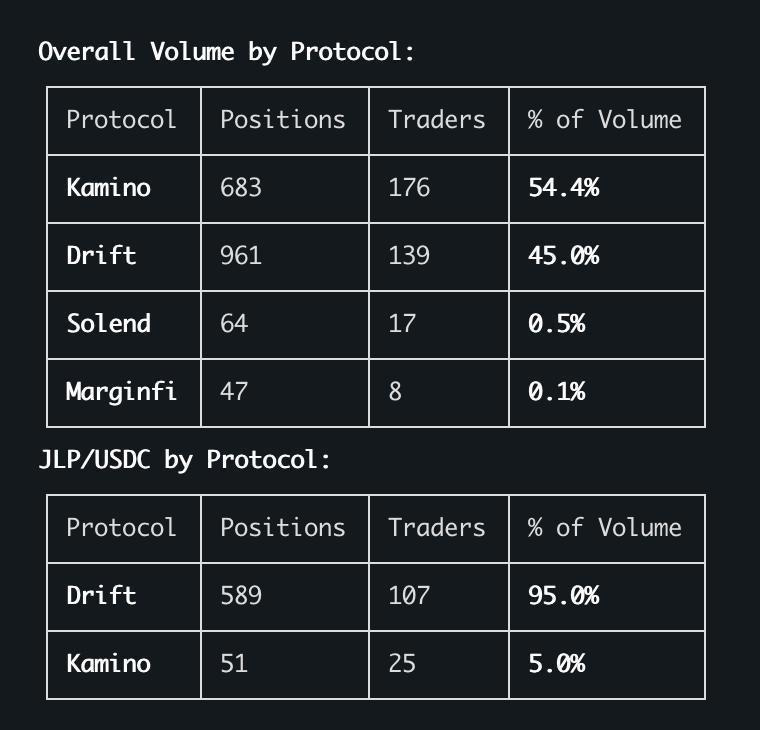

We already see primitive versions of these trends in our portfolio companies. Asgard.fi mimics a traditional prime brokerage through routing lending positions across perpetual exchanges to generate yield. Close to 45% of their overall volume and 95% of their volume on JLP go through Drift today. Asgard could offer this infrastructure to a traditional fintech player focused on on-ramping, creating a neo-banking experience where users can earn yield on their dollars through such composable layers.

Given the network effects of existing Solana-focused service providers, we believe the surface area for such opportunities remains underexplored.

While these statements about product direction are forward-looking, it is important to note that Drift’s team is one of the few that have consistently built a product with meaningful revenue, across cycles. Q4 2025, in fact, marked an ATH for multiple exchange metrics. Compared to Q2 2024, earnings increased from a paltry $970k to $6M on the exchange. Its average daily volume doubled - from $126M to $268M, and the total volume traded on the exchange scaled from $11B to $25B.

The Revenue, Valuation Divergence

Drift remains undervalued when compared to its historical trends, too. Drift is trading at the lowest multiple (on fees) it has ever had. At its peak, Drift’s price-to-earnings ratio was 80. It generated $5.7 million in earnings in Q4 2024 and traded at an FDV of $1.85 billion. ( We annualise the quarterly figure to $23.1M for earnings) Last year, Drift generated a total of $19.8M in earnings. It trades at an annualised protocol earnings of ±4.8x. If it were to simply return to its all-time high multiple of eighty, it would trade at an FDV of $1.58B. A more conservative and realistic outcome would be a return to a multiple of twenty (based on current earnings of $19.8M), which would have the token trading at $398M, or four times its current level.

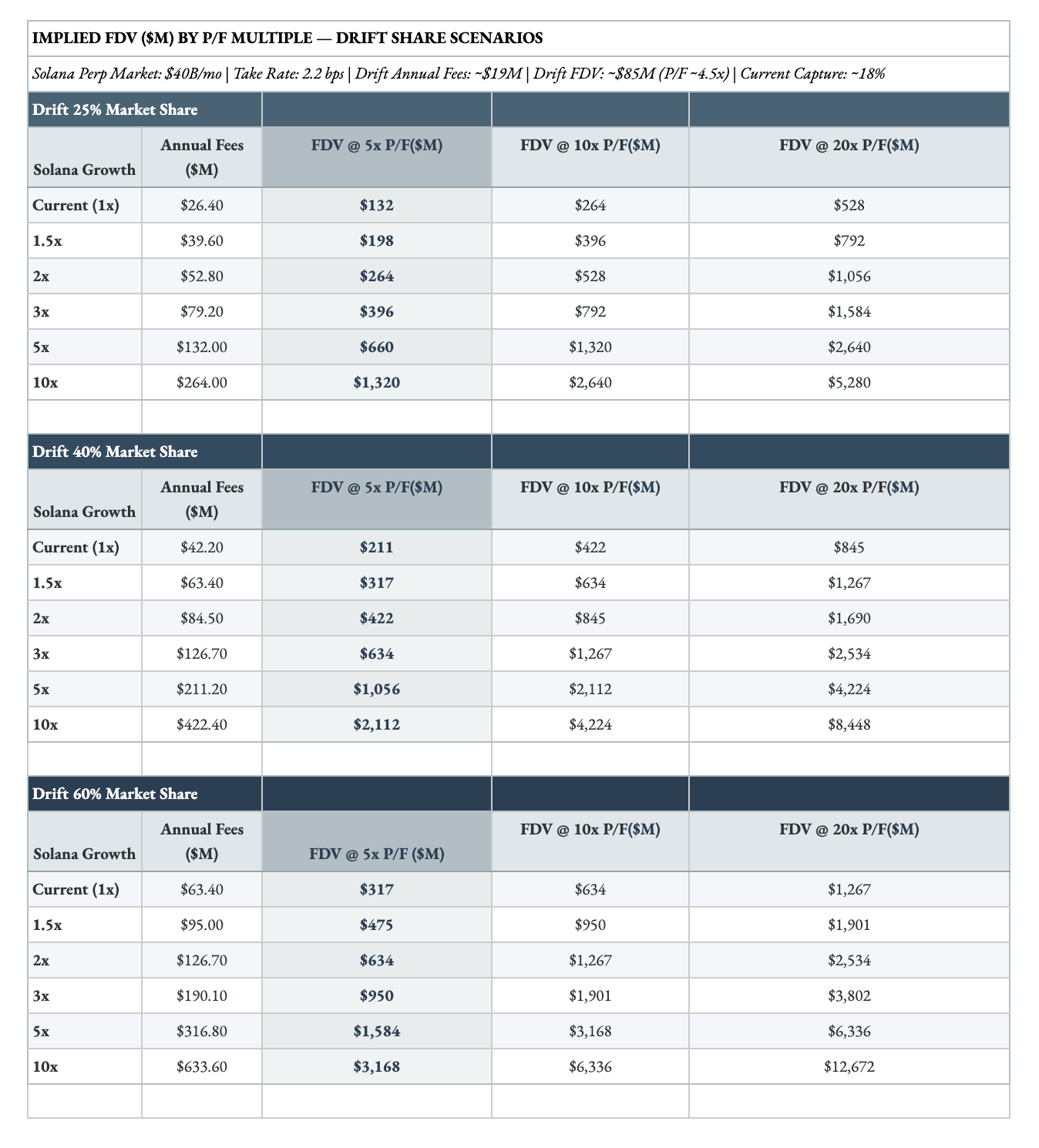

Another way to understand this divergence is by observing the difference between current volume metrics and past highs. When the market is in favour of an ecosystem, it can offer an extreme premium (such as a 40x multiple) relative to Drift’s current valuation. We model two scenarios. One where Solana’s perpetual exchange volumes surpass the $40B it sits at today. And one where Drift is able to return to capturing 60% market share within Solana’s ecosystem. In both scenarios, we use fees to measure multiples as the protocol’s retained earnings may change in the coming years.

There are three catalysts that will drive valuation up.

Traders who left for Pacifica to receive airdrops will return to Drift. Users routinely switch between products in anticipation of token rewards. Over time, users go where a pre-existing relationship and better liquidity exist.

Secondly, the nature of RWA assets available on Drift expansion will contribute to its overall valuation.

Lastly, Drift’s presumed 2.2 bps in our modeling is extremely conservative. As shown further above in the document, that metric is usually twice as much and closer to 4 bps on average.

Solana is steadily positioning itself as the layer on which all fintech primitives will emerge. There needs to be an avenue for hedging assets, for price discovery to occur, and for traders to have easy access to leverage. Drift sits at the intersection of all three needs. It will see positive tailwinds as Solana’s focus shifts from being mostly on crypto-native spot assets to a mix of commodities, indices, and equities in the coming quarter. We see the world coming on-chain, through Solana. The data below explains our reasoning for it.

Solana is undergoing its own infrastructure evolution. If Alpenglow, from Anza, comes to market, transaction finality will happen in roughly a third of the time (150ms versus 400ms currently) directly reducing the latency cost that JIT auctions currently carry. A frequently debated point of view is that Solana’s transaction throughput is the bottleneck for perpetual exchanges. Alpenglow changes that equation on finality.

Firedancer, an independent validator client built by Jump Crypto addresses throughput through parallelisation. Once live, Solana’s ecosystem will have two independent validator clients built by entirely separate teams. This matters specifically for Drift because its verifiability argument only holds if the chain it settles on is itself resilient. In the meantime, Drift’s gasless trading features have already pushed the product closer to parity with its peers on speed of execution

The World will Trade Onchain

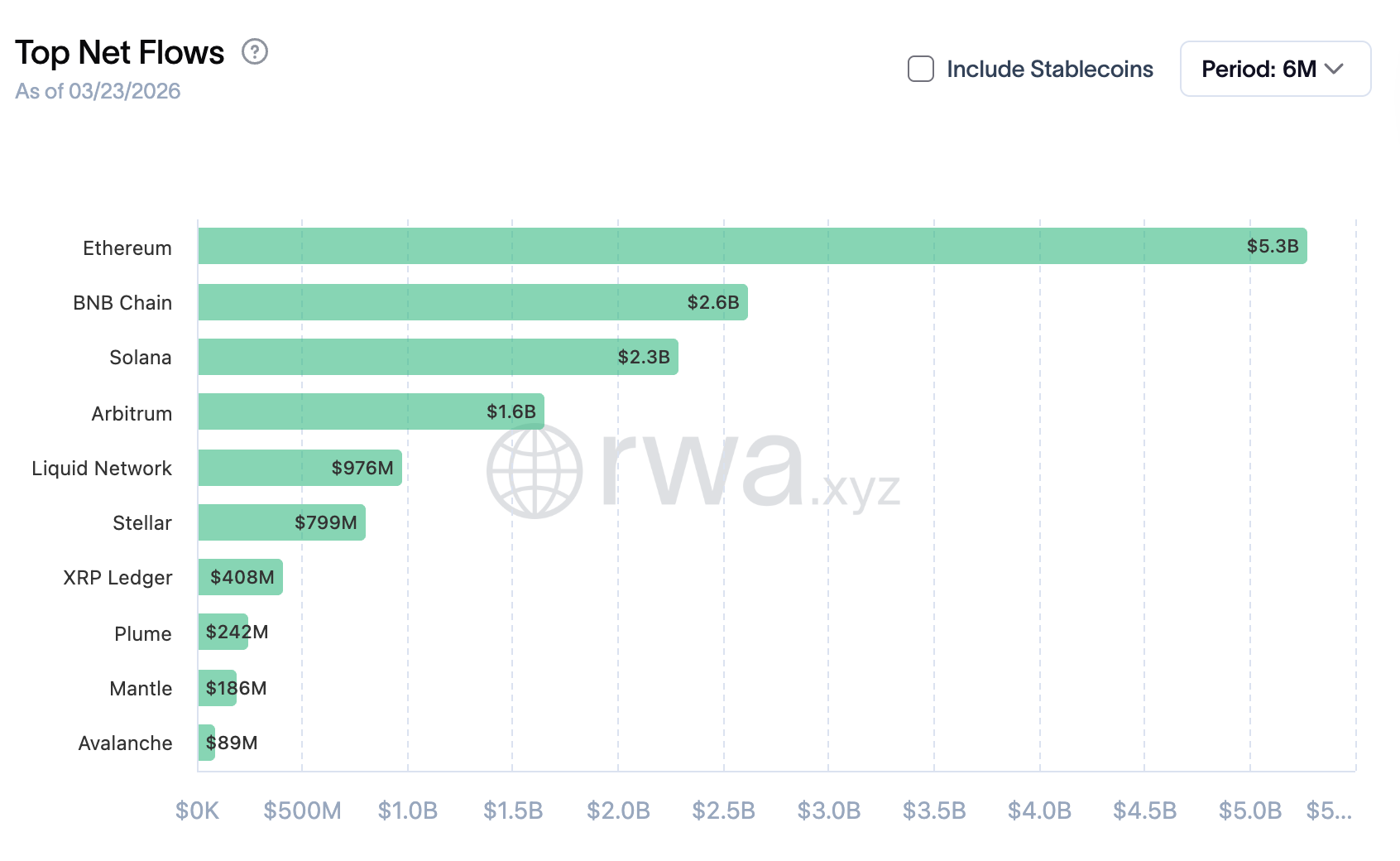

Solana’s RWA base has grown from a little over $10 million in January of 2024 to over $1.6 billion in the span of two years. It is far smaller than Ethereum’s $14.7 billion, which accounts for ~59% of all RWA assets represented on-chain.

According to RWA.xyz,

Solana has the second-highest holder base of RWA assets on-chain at 283k, compared to 160k on Ethereum

It was home to 60k active addresses engaging with RWAs on-chain in January of 2026 alone.

Solana has been where retail participants already are. It is where they come to hold meme assets, send dollars cheaply, and stay up-to-date on culture. The fact that these users currently generate $120k each day on Phantom through builder codes is a sign of how big the market for retail participants trading perpetuals could be. There is a segment of the world that needs access to commodities, equities, and foreign currencies without going through local brokers. HIP-3 serves the crypto-native crowd quite well today.

But when you consider tooling such as wallets, off-ramps, and private key management solutions, along with the mix of spot assets, Solana is positioned as a better ecosystem for developers to build on. We are already witnessing an uptick of RWA assets on Solana.

Currently, xStocks alone does $600 million in on-chain volume in spot markets each month. HIP-3 native markets are expected to reach $100 billion in the coming months. Presume half of that would trend to Solana and be worth $50 billion each month. Given Drift’s market positioning, it could command half of that volume - and capture $25 billion. Assuming a fee rate of 2.2 bps on that volume, we are looking at a fee uptick of $5.5 million per month. The number is 5.34 times what Drift reported in earnings in January, at $1.03M. Annualised, that amount will be $66 million. Considering a 5x PF, we are looking at a $ 330 M valuation.

Drift can capture half of the RWA segment volume as it has demonstrated the ability to capture 60% of the market on Solana in the past, and its architecture is meaningfully better for institutions that care about order sequencing, settlement times, and verifiability.

In 2025, Drift was early to collaborate with Securitize to bring a tokenised version of Apollo’s Credit fund on-chain. They have proven their ability to structure, on-board, and create MVPs with the largest asset issuers to extend asset representations on-chain. As the demand for RWAs increases, Drift benefits from its storied past and strategic positioning within Solana.

Assets on Solana usually trade at deep discounts to their fees due to the seasonality of revenue sources or being relatively early. Drift, by comparison, commands a premium due to its steady, consistent governance structure and the fact that the team has silently built a cash-flow machine that sustains itself through market cycles across all market environments. Everyone needs a perpetual exchange regardless of whether tokens go up or down. Drift has consistently been the best avenue for traders on Solana. It has the opportunity to simultaneously expand its volume base while commanding a premium in the Solana ecosystem.

If it is to establish itself as the home of all DeFi on Solana, we expect this premium to grow substantially. Solana has yet to respond to Hyperliquid.

What Could Break

For Decentralised.co - the bet is not about going against Hyperliquid. It is a long on Solana’s ecosystem through a player that is deeply discounted for the value it generates and the premium its team should command. There are several assumptions that can break here.

As it stands, Drift’s revenue is being used to sustain the team. This is considerably better than selling tokens to fund operations, but if other perpetual exchanges continue to command volume and Drift struggles to catch up, it may find itself having next to no capital to reinvest in the community or product through incentives.

We also presume that price-to-earnings ratios are good indicators of a network’s value, but over the past four years, owning the token has not meant much in terms of how earnings flow back to users. The assumption here is that investing earnings in the team’s operation is currently the best use of them, but that assumption can falter.

Hyperliquid trades at a 29 PE because much of its earnings flow back into the token through buybacks. Currently, Drift’s model does not have a buyback program. The markets may continue to punish this through valuation discounts if there is no confidence that the product is better off leaving the fees unused.

Lastly, Jupiter, given its aggregator model, can compete with Drift on several fronts. Ultimately, the choice between Jupiter and Drift boils down to a specialist platform vs an aggregator. Our assumption is that a specialist will beat an aggregator during this phase of the market, where a sectoral leader is not yet established in Solana. Jup’s new chain and ability to acquire players within Solana ecosystem are meaningful threats to Drift.

One challenge we see is with tying the token’s revenue to its valuation. This will require working with the team on governance and on the long-term relationship between token holders and the business’s core fundamentals. As it stands, the token could benefit from more proactive governance and engagement from its holders.

For investors looking to build exposure to perpetual exchanges, Hyperliquid could be a better choice, given that the assistance fund on Hyperliquid routinely buys back HYPE tokens from the market. One of the things we would like to work on in the coming months is to propose a framework for Drift’s token to accrue more value from the traction the protocol generates.

Drift’s team has shown exceptional commitment towards building open, verifiable markets. They have been at the cutting edge of delivering a better user experience (via solutions like gasless trading) without compromising decentralization. Although markets do not currently talk about the need for verifiability or trustlessness, we believe it is only a matter of time before these elements become important.

In the past four years, Drift has shown commitment towards that mission. Our investment is a bet that as Solana’s capital markets mature, venues that prioritise verifiability, composability, and openness will command a premium.

We are ultimately long open, verifiable, composable markets. Drift is a position that expresses that conviction.

Verifying markets,

Joel John