The Libra Hustle

Breaking down why Facebook is entering the blockchain race

If you were born after 1995 and grew up in a developing economy, odds are high that Facebook has encompassed the vast majority of your digital life. The platform hit a billion users right around the time you were 13 (2008), leveraged network effects of Mobwars and Farmville to keep a younger demographic hooked and converted to ownership of Whatsapp and Instagram as they grew older. For many of us — Facebook provided the means to connect to friends far and wide, hold conversations that’d otherwise be impossible and easily connect to influencers that were continents apart. In a pre-4G world, where e-commerce had not taken off, Facebook was the internet for so many of us. And it remains to be the case. If not on the platform itself, through Instagram or Whatsapp, Facebook owns much of the world, by its most private conversations and intimate moments shared in pictures. Zuckerburg is simultaneously the brand ambassador of a digital nation whose powers remain unchecked and the CEO of one of the fastest growing companies of our times. His board struggles to tame him, his regulators fail to understand his business model and his competitors crawl far away in the distance as the corporation sustains its growth consistently. Quarter after quarter.

Next week will be a monumental one for the blockchain ecosystem. One that many of us had anticipated for over a decade. It is when this niche technology that was once discussed only in the strangest, sometimes nerdy corners of the web goes mainstream. 2.4 billion users across 3 major platforms may access Facebook’s blockchain initiative as it rolls out to the public. While much has not come to the public yet, there are a few hints that explain what Zuckerburg is up to, where his business is headed and what that means for the people that have been tracking the space. Mark first alluded to the concept of “decentralisation” in a New Year’s post in 2018. While much didn’t come of it and Facebook continued to remain busy with regulatory tango over the course of the year, it seems his team has been busy at work. News has emerged that a Geneva-based foundation has raised $1 billion for the initiative from 100 major corporations including the likes of Uber, Visa and prominent Indian payments player PayU. Another way to put it is that the world’s largest corporations have pooled together a billion dollars in collaboration with the world’s largest digital network platform for a blockchain initiative.

Why Is Facebook Going Down This Route?

It would be a farce to even remotely suggest that Facebook’s entry into the space is based on good intentions. Calls to break Facebook apart has come from its early founder — Chris Hughes and early investors — Sean Parker and Chamath Palihapitiya. This is not for a lack of reasons. Facebook has been responsible for breaking down democracies, mass murders and even lynchings in India. The spread of fake news on platforms owned by Facebook today may have more power to declare death on an individual that supreme courts do in certain countries. Facebook’s echo chambers are the equivalent of religious propaganda inspiring hatred and calls to violence in the digital age. With this in context, it is only fair that the platform develops checks and balances for how its content is spread, consumed and verified. However, inspite of having a literal army of manual laborers, many of who are paid below minimum ages, whilst being subject to torture — mental, physical and emotional, Facebook has failed to do so. However, nothing Facebook is about to do has with its failures in being an ethical business that pushes mankind forward. It really boils down to numbers. In order to understand what Facebook is about to pull off, one has to dig into how its earning patterns are currently. To break it down to pointers here’s what you need to know

Facebook has a total of 2.3 billion users globally across three prominent platforms — Instagram, Whatsapp and Facebook itself

The vast majority of these users are interestingly from what are referred to as Tier 3 economies in the context of advertising. The average income in these nations is low, which in turn converts to lower digital spends, which in extension converts to lower RoI for digital ads.

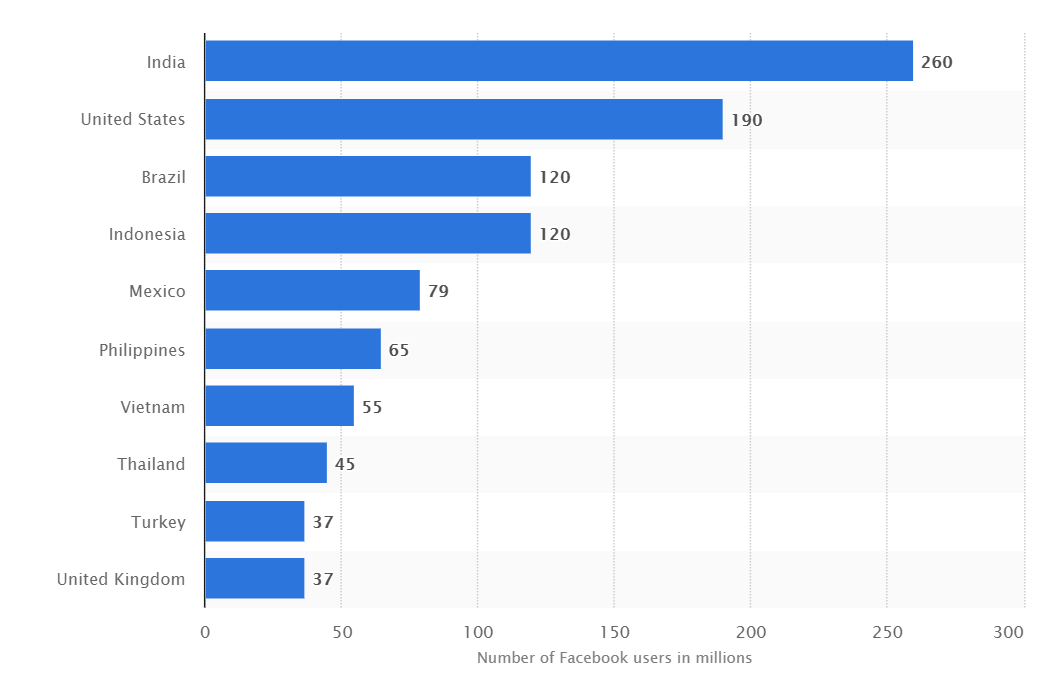

India has 260 million users on the platform and claims the largest user base geographically. Technically a population that is as big as that of the United States. This is followed by Brazil at #3 (120 million), Indonesia at #4 (120 million), Mexico has 79 million, the Phillipines has 65 million, Vietnam has 55 million and Thailand, 45 million. You get the point — low-income economies dominate Facebook’s user base by a great extent.

The reasoning for this is simple. Facebook’s growth came at a time mobile and internet penetration happened simultaneously. For many in these economies, the mobile was the first ‘digital world” experience. The internet is essentially Youtube, Whatsapp, Facebook and new age platforms like TikTok in this part of the world

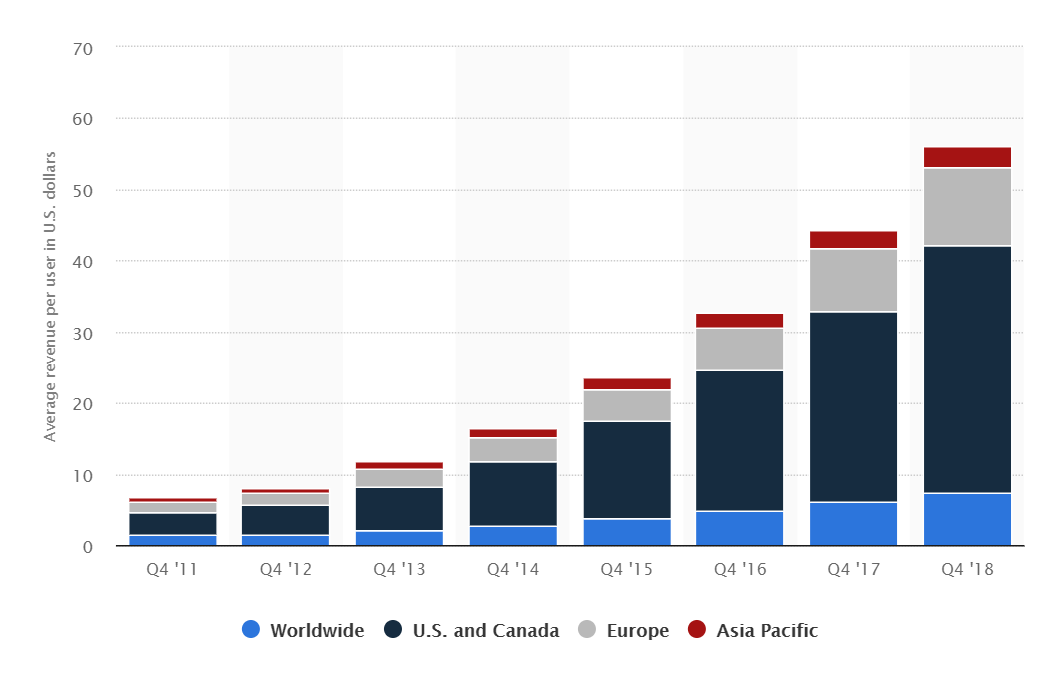

For context, Facebook’s Average Revenue Per User in America is $34. In India, it is under $3. The global average is twice that figure at $6.

Facebook is stuck with a conundrum where its largest userbases make the lowest amounts in return for the platform. With the spread of fake news, higher investments into moderation meant lower ROI from these economies inspite of economies of scale

Combine that with the fact that AI has not been developed to moderate regional linguistics (and by extension regional content) and you have Facebook in an icky position where it cannot sustain its existing growth in developing economies or run profitably without facing heavy regulatory pressure.

Tl:dr — Facebook’s largest userbase comes from developing economies. But it makes the lowest income from those regions. Difficulties in training AI for regional content, combined with heavy expenses in human run teams means difficulties in running the business.

However, Facebook has a golden goose that has been slowly coming of age in these regions. It is payments. Unlike advertisements, payments do not require vast amounts of on-platform web traffic. It is driven by utility. And unlike web publishers, having a cut of digital transactions could mean considerably higher average revenue per user. By mapping out the social relationships, emotions (through reactions), preferences (through likes), political, artistic and religious leanings (through groups) Facebook has a map of where and how individuals prefer to lean towards in terms of consumption. By mapping where and how often individuals pay, Facebook will have data on individual expenditure. This move is likely inspired by three key trends in Facebook-owned platforms

The surge in social selling on Facebook groups. It is common for individuals in India to list their houses for rent, applications for sale or even pets for adoption in large facebook groups. Key reasoning that encourages this behavior is the verification of social profiles and background checks that are enabled by simply clicking on the poster’s profile link.

The surge in influencer sales on Instagram. The platform continues to dominate among millennials as a go-to platform for everything from news to comics and everything in between

A rising number of business interactions enabled by Whatsapp. Small and medium enterprises stand to see substantial gains through chat-bot enabled interactions on Whatsapp. While the APIs are not open for the general public yet, prominent services such as MakeMyTrip in India already deliver travel tickets in PDF forms through WhatsApp messages. It won’t be long before full-blown checkout processes will be enabled on the platform

Facebook’s desire to enter payments is further cemented by the fact that it has rolled out digital payments in India and Thailand, two of its largest userbases. By simply shifting from an advertisement driven model in these economies to solely focusing on payments, the “social network’ platform will become a banking behemoth that can compete directly against the likes of WeChat.

What does this mean for the platform?

In order to understand what blockchains enable for Facebook, one has to associate the key use-cases that may see direct utility from an integration currently. While all of these are speculatory use-cases, they are ones that can be realistically be integrated into their system and see substantial traction. The purpose of this exercise is not to suggest Facebook will enable them but to lay out the key applications that may witness a threat from Libra

The Identity Stack — Facebook already holds data on social verification of individual profiles. Our social interactions are algorithmically used to define the creditworthiness we hold. In some nations like India, Facebook has also gathered passport and Aadhar details on users alongside phone numbers. Put together, Facebook could expand into a self-sovereign identity network. Much like how we have “Log-in With Facebook” today as an option to merely login and provide details on name, age, region and taste profiles, Facebook could use blockchains as an identity layer to enable authentication to government officials, banking partners and even employers to check the credibility of an individual. With Apple launching its own “Log-in with Apple” button for third-party apps and Microsoft’s renewed focus on Decentralised Identity (DID), one has strong reasons to believe this could be the case. Note: I have covered more on DIDs here.

Gaming — One could argue that Zynga (the publisher behind Farmville and Mobwars) was the reason why Facebook spread so virally in regions like India early on. Low power, browser-based gaming built on network effects was a powerful on-boarding tool at a time when much of India browsed the web on 2 Mbps connections with low compute power computers and no graphics cards. The success of Fortnite and Apex legends repeated the same success for a time when mobile hardware was becoming cheaper and internet costs reduced. Facebook’s bet on OculusVR is an indication of where it is eying its next big win. If VR is to take off, and Facebook is the largest distributor both from a hardware and a network access point of view, the social network is well poised to gain from blockchain integration. How? Non-fungible tokens allow the transfer and trade of in-game assets with ease. Where previously a player spent years building up a FarmVille profile and gained little or no financial gain from it, in-game assets could be made into a marketplace of its own through non-fungible tokens. This is not a ‘new” invention in itself. Counter Strike Go has a $2.5 billion economy for digital guns. Similarly, Grand Theft Auto 5 has generated an additional $500 million in revenue from in-game assets. These are both single games, with a decade-old brand behind them. Given Facebook’s current wide user base, evolutions in VR and the fact that the network has benefitted from game economies in the past, it may only be a matter of time before they roll out full-fledged NFT based marketplaces. Need that brand new t-shirt from Nike? How about you redeem 100 points gained from visiting their latest store (AR+Location data). Facebook could effectively combine off-line retail, with digital economies by bringing together AR, VR and NFTs to their ecosystem. Note : More on what non fungible tokens are here.

Marketplaces — We have witnessed the unbundling of Web 2.0 in developing economies. But as I mentioned, for many, the internet is Facebook today. If that is to remain the case, Facebook will have to drive more value into the platform to ensure user transactions don’t spill out. How does one ensure that? Create social network based economies. The earliest variants of this already exist in the form of Facebook Groups. However, the spill-over happens in the form of transactions. An effective blockchain based escrow system that combines DID based reputation and on-chain transactional records to gauge the user’s consumption patterns could further enhance how individuals engage with commerce on the platform. This could theoretically spark an entirely new rally in entrepreneurship in tier two and tier three cities in a nation like India. Why? Because women there are already using Facebook to explore everything from Saree designs to food recipes. What’s missing for them is an effective payments mechanism and logistics. While logistics is too operational for Facebook to bother with, in-platform payments could reduce the barrier for these entrepreneurs to begin selling digitally. From a very Indian point of view, this could bring our cities and villages closer. However, given the role Whatsapp Payments and UPI plays in our economy, Facebook’s payments play alone may not be of much benefit. It will only be in combination with the network effects the social network’s large user base already offers and the identity/reputation system mentioned above that individuals will be able to create high trust economies.

Remittance — India receives roughly about 2.5% of its GDP in inbound remittances. In dollar terms that’s roughly over $79 billion. While most growing economies may not be the best to advertise within, capturing a large user base in these regions and monetising them through a capital transfer network could prove to be highly profitable. In the case of Facebook — the platform comes with the added advantage of having users in the most remote corners of the globe. One could argue that two things reach the remotest parts of India. One is its democracy each time our elections happen. The other is Facebook, thanks to the newfound increase in network access. Through collaborating with a global network of banking partners — Facebook could offer what Transferwise has historically been doing for what could be considered ‘prosumers” in the web. How would a network of bank balance accounts at fast enough speeds? That’s perhaps where blockchains could be used. Even regions that have been hostile to ‘crypto’ have opened up to the idea of using blockchains for balance settlements between them. In India, this includes pivots from prominent banks such as Yes Bank, Axis Bank, ICICI and a slew of others. What facebook could offer them is a network of users, and what banks could offer Facebook is a financial network. By creating a global network of banks and providing the infrastructure layer for them (through project Libra), Facebook stands to be the middleman, and therefore gain a cut of these transactions. When it comes to remittance, fees are charged on (i) percentage of volume and (ii) foreign exchange rates. In comparison to traditional alternatives, Facebook can realistically compete on providing lower fees on volumes through efficiency in the foreign exchange rates it can negotiate for in-platform transfers. Even if Facebook eats into 5% of the current remittance market — that is, $3.5 billion and makes 1% in profit, that is a material gain of $35 million the platform could make. Given the average revenue per user is at $3 for an economy like ours, that is roughly worth ~12 million users or 5% of its existing user base of 240 million users. Given that Facebook’s growth in economies like India is beginning to slump, the platform would have to find new avenues for growth. Remittance, could realistically be one of them.

Banking — The ultimate play for Facebook will be to evolve into a full fledged bank of its own. In the list of possibilities, this has a sub 20% chance for me. One way to think about this is in the sense that as digital platforms like Twitter and Facebook evolve to be as large and powerful as nation states, they will roll out internal banking systems to enable and retain economies. Jack Dorsey has alluded to doing so with Twitter a number of times. Bitcoin is in some sense the internet’s first fully native currency (discounting the likes of e-gold and Liberty reserve). Facebook is well poised to create a network of Startups in developing economies like Indonesia, Vietnam and India to help with on-boarding individuals to their digital “banking” platforms. Based on the metadata they have already collected, they could offer a wide range of services ranging from lending to social network based discounts and custom deals. In comparison to traditional banks, Facebook has considerably more data on individuals and could, therefore, customise banking services on the basis of the need of the individual. However, before this can be a reality there are large regulatory hurdles to cross. One way Facebook could get around them is through the acquisition of regional start-ups or talent from regional market leaders. Most recently in India, Facebook had hired Ezetap — a prominent payment solution’s CEO as the head of Whatsapp payments. Is this possible? Less likely. Is this profitable? Definitely.

Data Marketplaces — An additional avenue for growth in the case of Facebook would be the trade of data. Once blockchain based identity networks are in place, Facebook could theoretically enable the trade of personal data on the platform to private enterprises in exchange for discounts and redeemable points. The reasoning for this is the fact that as the interest of the demographic on the platform changes (eg: shifts in music preferences over the years), old data-sets held by the company may no longer be meaningful assets in the context of advertising. However, it could be handy for the purpose of research or training AI. By allowing a secure marketplace where individuals are allowed to trade their personal data and track who has access to what of it for how long, Facebook could spur usage of the platform from users that are now slowly moving away from it and create a new avenue for growth.

What could be the impact on the token economy?

Distribution. Distribution. Distribution.

That is at the crux of what Facebook’s move into the space means. Until earlier, platforms such as Twitter, Facebook and Google had control on what crypto oriented content was discovered and used in the form of ads. In fact, when advertising of token-based products declined in 2018, startups struggled to find a user base. Even today, with Apple maintaining a monopoly on how apps are distributed for the iPhone, token-based apps struggle to go through verification. One could argue that Facebook could be more lenient with how it lists and enables apps. The more powerful case here being the fact that all of a sudden developers are incentivized to build for Facebook’s network of users given its large user base. Imagine building Android apps without Google’s ecosystem of apps. Or iOS apps without Apple’s ecosystem in place. Until now, what existed as loose ecosystems with steep learning curves will be replaced by Facebook’s large distribution channels. Distributed applications (dApps) built on Facebook could advertise on the platform and find its first ten thousand users. For context, daily average users across every dApp today is at 300,000. That is below an estimated 0.01% of the internet’s population. Apps that leverage the advantages token based dApps provide today (NFT, asset ownership, data portability, identity) but remain centralised in Facebook’s servers could swallow up the vast majority of users that are unaware of the decentralised ecosystem. However, as they become aware that their digital currency is not really “theirs” and a company based off Silicon Valley now owns their data, digital assets and financial holdings — they may spill over to truly decentralised, immutable, permissionless assets such as Bitcoin. In other words, Facebook could be the inflection point that makes the discovery of this ecosystem possible. This was the case for many of us in India. As foreign companies like Paypal struggled to meet the needs of individuals from India seeking digital payments solution, they spilled over to Bitcoin and other digital currencies. If even 1% of Facebook’s existing userbase converts to using Bitcoin, that is roughly about 25 million users. As a metric of comparison, Bitcoin has roughly 800,000 active wallets the past week. In other words, even a small amount of spillover from Facebook’s space to the token economy could be a huge boom.

The idea that Libra could offer a stable coin alternative to many in developing economies within legal frameworks that currently exist may be flawed. The reasoning being that nation-states often restrict the amount of foreign currency an individual can hold to restrict currency flight. In India, under FEMA laws (Foreign Exchange Management Act) this figure is at $250k. If an individual did wish to hold dollars, they’d rather do it through traditional avenues — that is, their banks. In the case of nation-states where financial infrastructure has been toppled completely (eg: Sudan), Bitcoin acquired through OTC (over the counter), P2P (peer to peer) transactions serve the function far better than Facebook’s libra offering. In other words, what Facebook is offering is not to be seen as a sovereign, immutable, stable alternative to what Bitcoin offers. One is a corporate offering designed to maximise the profits of shareholders. The other is a decade long financial experiment, secured by infrastructure that has billions invested in it, developed on open-source code, distributed by individuals who believe in it.

The big threat to Bitcoin from Libra comes in the form of bad marketing. Imagine, Bitcoin Cash — except with the distribution channels that Facebook holds. That is what we are up against. Individuals could be deluded into believing their data is decentralised, their currency is reliable, their moments can be monetised and that Facebook will work in their best interest. All while corporations plunder it for their own gains. What Facebook could be rolling out in the coming week is an inter-corporation allegiance to share and exploit the personal data of individuals in the most efficient fashion. Liked a track mentioning Gucci on Spotify? How about we offer a 5% discount on it while checking out with PayU. Want a Visa enabled loan on it? Maybe finance it by giving us access to your health data? That is the murky world Libra may enable. Every truly decentralised application today is up against this new reality where a large central corporation with the distribution channels needed to change user behavior and dictate the fates of corporations (eg: Snapchat) and nations (eg: Myanmar) alike is out to eat their meal.

This means two things to put it simple language.

User experience is no longer something we can aspire to improve. Existing token-based applications need to be able to compete against centralised, web 2.0 alternatives that are well cognizant of the challenges posed by web 3.0 applications. They are not here for a share of the pie. They are here to set the restaurant on fire. There will be a period of compromises where token-based applications can find middle-ground with Libra and will likely leverage it for distribution but as we have seen with Zynga on Facebook and distributors on Amazon in the past, the platform can eat up the business built on it. Anyone that truly cares about decentralisation and empowering users, has their reason to be averse.

Infighting within token economies needs to reduce. We are past a point where radical disagreements on key matters can hinder the pace at which we innovate. Token economies need to be able to find middle ground regardless of their chains and build one another instead of torching one another. Key challenges with scaling and fees continue to plague Bitcoin and Ethereum as on-chain activity surges. Inspite of layer two scaling solutions such as those of Lightning network, with a mere $10 million in capacity in Lightning network, one could argue that we are far from seeing true, retail scale. In addition to this — if an individual is expected to pay $2 in fees for each transaction on a blockchain, it could become impractical for utility for roughly 4.5 billion individuals living under that figure today. While there is a price to pay for immutability, sovereignty and decentralisation, let us not build it upon economics that is not inclusive of the vast majority of the world.

Regulators around the globe will wake up to a new reality where decentralisation is not at the fringes but a reality. The FSB (Financial Services Board) of the G20 recently issued a document exploring how decentralisation in finance will affect the space. We will soon see the same becoming applicable for elements such as data ownership and identity. Decentralisation as a macro-trend is here and it is here to stay. It will take a while before technology and regulations catch up to it. In the interim however, we ought to realise that we are at the inter-junction of a generational opportunity to remake the internet the way it was designed to be by Tim Berners Lee. Before Facebook’s newsfeeds took over the web, communities interacted with one another in niche forums and chat rooms. Bitcoin had its own share in IRC chat, e-mail lists and Bitcointalk before the industry boomed. When Facebook enters the party, it enters with the same monopolistic mindset it has run with for over the past 15 years. With the same desire to bring together communities and individuals onto a single platform. And if it is able to sell its blockchain with decentralisation sprinkled on top with just the right amount of utility and optimised use-case, there will be challenges in onboarding individuals to a truly decentralised web.

Back to regulations… Those in India wondering if Facebook’s entry could shift regulatory attitudes meaningfully are in for some serious disappointment. As stated earlier- Facebook will not be pushing for a tokenised economy whose pricing moves on the basis of free market principles. It will be positioning itself as the platform upon which hundreds of corporations can pillage personal data and incentivise people while doing it. Even if there is a currency, it will only be a digital variant of regional currencies with high levels of AML/KYC and stricter tracks on how it is used. The idea that an American corporation is here to liberate individuals and ensure their sovereignty is as meaningful as American attempt in delivering democracy in certain parts of the globe. If and when regulators do shift their stance it will be because

1. The G20 has collectively made a decision on how to regulate the space

2. A large economy like the United States has created a functional framework

3. The government decides an outright ban to play vote bank politics.

If you truly care about decentralisation, individual rights and our ability to stand strong in the face of tyranny, I worry Facebook is not the answer. It is just another tool that has grown from the surveillance capitalism economy.