Why Stripe built its own chain

Owning the seven layers of a transaction

Hey there,

Today’s issue extends our piece on vertical capital integrators. Blockchain rails are changing how value moves across the internet. But little has been written on the mechanisms by which traditional capital aggregators — Stripe chief among them — have expanded into crypto rails. This piece plugs that gap.

I break down how value leaks out of the payment stack at every step of a transfer, then map those losses to Stripe’s acquisitions over the past two years. Those acquisitions will add another $1 billion to Stripe’s topline by next year. We believe there will be businesses built, scaled, and acquired in each part of the stack Stripe has been going after, as the pie for internet-scale finance is constantly growing and ever-evolving. This piece should help build a mental model of the individual constituents of that stack.

As always, if you are building along these themes, find us on Telegram or drop a note to venture@decentralised.co. We’d love to chat.

In 2025, Stripe made $6.9 billion in revenue. It processed $1.9 trillion in payments. That’s about 6.5% of US GDP and 1.6% of global GDP. Over five million businesses use Stripe to accept payments, including 90% of the companies in the Dow Jones Industrial Average. By most measures, it is the largest internet payments company in the world. Among international businesses Stripe caters to, 30% of revenue comes from countries that are neither its home market nor among the top 10 global economies.

The concept of “domestic markets” doesn’t really make sense for internet businesses. The share of cross-border payments cannot be ignored anymore.

Global cross-border flows exceeded $190 trillion in 2024 and generated an estimated $240 billion in revenue for the banks and intermediaries that facilitate them. The average cost of sending $200 across borders is still 6.5%, more than double the UN Sustainable Development Goal target of 3%. That difference, between what cross-border payments cost today and what they should cost, is the single largest fee pool in global payments.

So Stripe doesn’t make much on one of its fastest-growing payment processing through correspondent banks, FX desks, and SWIFT messaging infrastructure that Stripe has no control over. Gaining better control over cross-border payments will allow Stripe to capture a much larger share of this growing pie.

Capturing a larger share without passing cost to the consumer means bypassing the existing intermediaries. That is what Stripe has been building. The only way to see what it is doing is to look at who the banks and financial institutions actually are, and what each of them is being paid for.

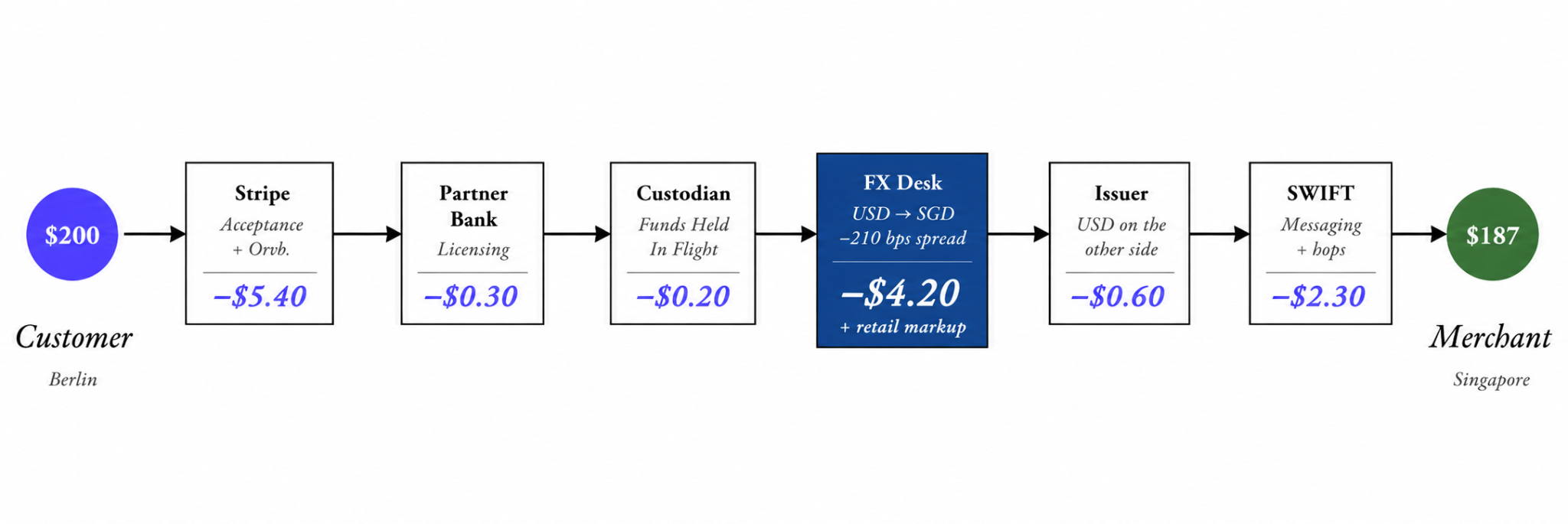

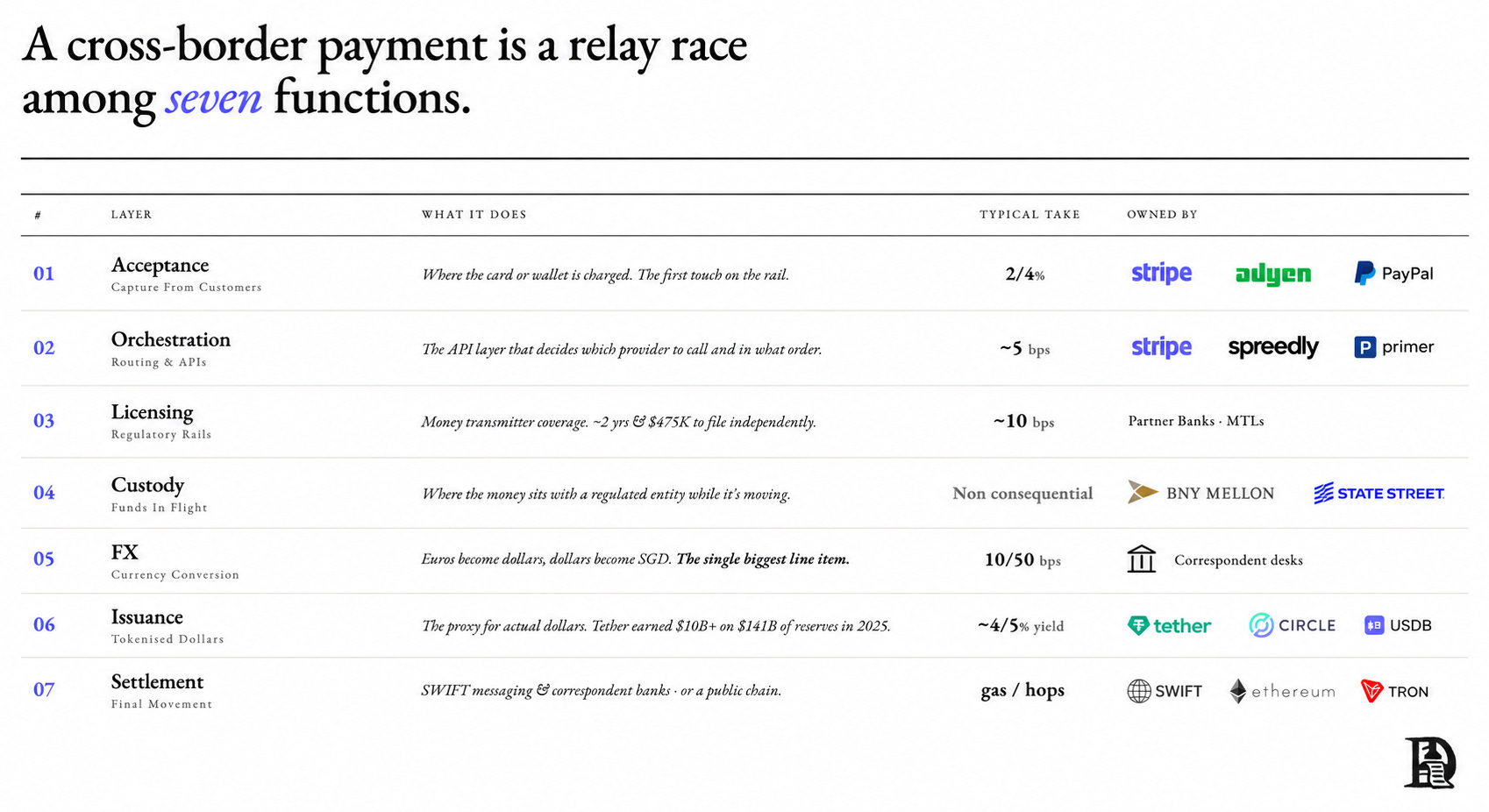

A cross-border payment is a relay race among seven functions, each collecting a toll before the money moves to the next.

Consider a merchant in Singapore accepting a $200 payment from a customer in Berlin. Stripe collects the transaction at acceptance and routes it at orchestration. A partner bank takes ~10 bps for licensing the cross-border move. A custodian holds the funds briefly. on the EUR to SGD conversion. A commercial bank or stablecoin issuer represents the dollars on the other side. SWIFT carries the messages. By the time $200 lands in Singapore, six different counterparties have been paid. Roughly $13 of the original $200 is gone before the merchant sees the receipt.

Seven layers, roughly in the order the money touches them:

Acceptance is where Stripe, Adyen, and PayPal capture payment from the customer. Take rates on a single cross-border card transaction are around 3% to 4%.

Orchestration is the API layer that routes the transaction and coordinates between providers. Stripe operates here alongside dedicated orchestrators like Spreedly and Primer. These players charge a few basis points on every transaction.

Licensing is how moving money across borders becomes compliant. If the operator does not have its own money transmission licenses, it must rent rails from someone who does. A typical US-to-Europe transaction routes through a partner bank or a licensed money transmitter that earns a cut for lending its regulatory coverage. Getting licensed independently takes roughly two years and up to $475,000 in filing fees, which is why most fintechs end up paying for access to someone else’s licenses.

Custody is where funds sit with a regulated entity while they are in flight. This layer is owned by custodian banks like BNY Mellon and State Street, which charge custody fees on balances and transaction fees on movements. Stablecoin issuers have their own Treasury custody relationships, which is how BlackRock and Fidelity ended up as major players in the stablecoin reserve market.

FX. Somewhere in the route, euros have to become dollars, and dollars have to become reais. Currency conversion is handled by FX desks at correspondent banks, which charge spreads of 10 to 50 basis points on institutional flows and substantially more on retail volume. FX is one of the single biggest line items in the $240 billion cross-border revenue pool.

Issuance is where the proxy for actual dollars comes into the picture. Stablecoin issuers allow companies and users to mint and redeem tokenised fiat currencies. Tether holds roughly $141 billion in short-duration Treasury reserves and earned over $10 billion in profit in 2025, almost all of it yield on reserves. Circle’s revenue on USDC works the same way.

Settlement is the final movement of value between institutions. In the traditional system, this is done over SWIFT messaging and a chain of correspondent banking relationships. This is where delays and costs compound. Stablecoin payments solve the delay by settling on a public blockchain like Ethereum, Solana, or Tron, but those chains charge their own transaction fees in their native tokens, which is money that leaves the payment stack entirely.

Every cross-border payment today passes through some combination of these seven gates. Most are owned by different entities. And that’s why it still costs ~6% to send $200 across a border. The $240 billion that banks and intermediaries collect on cross-border volume is the sum of what each layer charges.

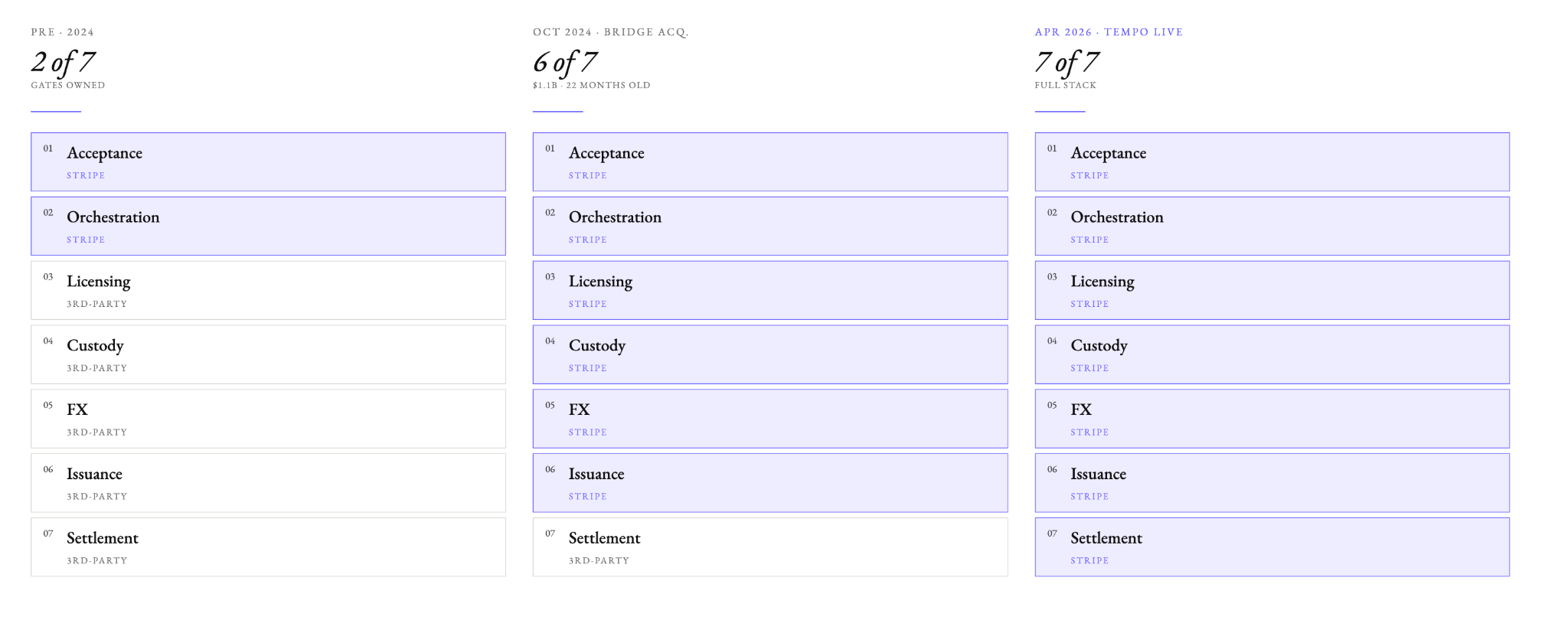

Until 2024, Stripe owned only the first two gates. The other five belonged to banks, FX desks, licensed money transmitters, stablecoin issuers, and SWIFT. That is the value chain Stripe set out to replace.

Stripe acquired the next four layers with one Bridge Transaction

By 2024, Stripe had owned acceptance and orchestration for over a decade. When our customer paid for the software to the Singapore company, the euros entered Stripe’s Acceptance infrastructure in Berlin within milliseconds of the charge being authorised. The Orchestration logic performed necessary checks and handed the payment off.

In the past, that relay was where value leaked. A partner bank took a cut to facilitate the cross-border payment. Some FX desks took a fee for converting EUR to SGD. Another bank may have to hold the funds in custody while they wait for settlement. A stablecoin issuer, or more often a ledger inside a commercial bank, created the representation of those dollars on the destination side. SWIFT passed the messages that let everyone agree on what had happened. Each gatekeeper charged, and the charges were invisible to the Singapore merchant, who saw only Stripe’s fee on the receipt.

In October 2024, Stripe announced the acquisition of Bridge for $1.1 billion. The company had been founded only a couple of years earlier by two former Square executives. It was already being used by SpaceX to collect payments for Starlink in over a hundred countries whose banking systems couldn’t reliably process dollar transactions, and by Scale AI to pay data labellers in dozens of emerging markets. The acquisition looked rich against any revenue multiple. But it wasn’t their revenue that Stripe was going after anyway.

What Stripe was actually buying was a collection of regulatory and operational assets on the cross-border value chain. Bridge held money transmitter registrations across 30 states in the United States. It had custody arrangements with BlackRock, Fidelity, and Superstate for the Treasury bills that back stablecoin reserves. It ran an FX desk that marked the spread between fiat and stablecoin pairs. It later issued its own dollar-backed token, USDB. Stripe bought the next four layers in a single transaction.

By the spring of 2026, Stripe owned six of the seven gates. Acceptance and Orchestration had been there since the beginning. Licensing, Custody, FX, and Issuance were acquired with Bridge. The seventh gate was Settlement. That’s where Tempo comes into the picture.

By the first half of 2025, with Bridge integrated, Stripe controlled six of the seven pieces of the payment system value chain. The seventh was the rail on which a settled payment moved from one ledger to another. In the legacy system, that rail was SWIFT. A payment that cleared via SWIFT could take a long time to finalise and incur costs that compound with each hop along the way.

The obvious question was whether Stripe should use an existing blockchain as its settlement layer. Ethereum was the largest smart contract platform and had the deepest developer ecosystem, but at Stripe’s potential transaction volumes, base-layer fees, and block times were disqualifying for small payments. Ethereum does about 15 transactions per second.

Stripe processed 137,000 transactions per minute at peak during Black Friday and Cyber Monday in 2024, and about 2,300 per second sustained. and governance priorities, few of which were tailored to the operational requirements of a payments company. Solana was fast enough at 3,000 to 5,000 TPS, but it was a general-purpose chain with its own validator set

The alternative was to build a chain whose priorities were payment settlement. In September 2025, Stripe and Paradigm jointly announced Tempo, a payments-focused layer-one blockchain co-incubated by the two companies. Matt Huang, Paradigm’s co-founder, would lead Tempo while continuing to run Paradigm. A month later, Paradigm confirmed that the Ithaca team was joining Tempo to build the execution infrastructure. Paradigm’s own research group would stay on the architecture.

The Ithaca engineers were the core contributors to Reth, a Rust-based Ethereum execution client that Paradigm had been developing since 2022 and had shipped in production form in June 2024. Tempo required a skill set suited to a new chain designed around payment throughput rather than general-purpose computation at its foundation, and Ithaca provided that.

It made sense to build Tempo as EVM-compatible because the Ethereum ecosystem of contracts, libraries, and developer tooling had accumulated over a decade of engineering work that Tempo could inherit.

By mid-2025, the structural ingredients were in place. Stripe was in a position to completely own the stack.

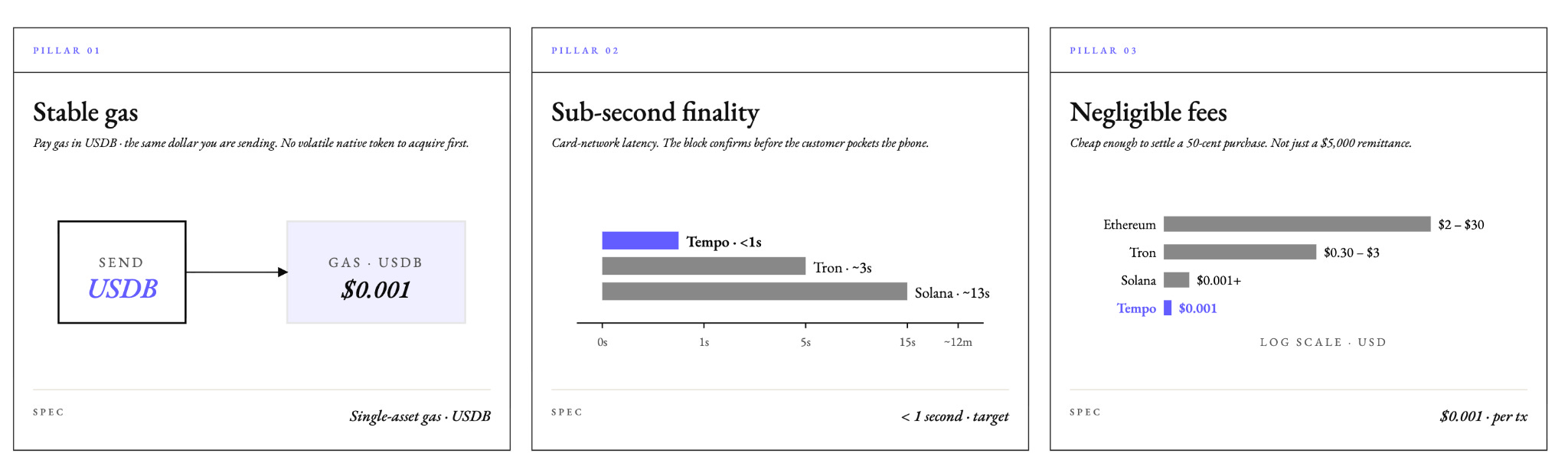

Tempo’s mainnet went live on 18 March 2026 — eighteen months after the Bridge announcement and six months after the Ithaca team formally joined. The chain shipped with the architectural decisions that its payments-first design required. It ensured three critical features:

Gas fees are paid in approved stablecoins rather than a native token, so merchants never have to hold a second, volatile asset to move payments on the chain.

Sub-second deterministic finality means a transaction is cryptographically final at block inclusion, faster than any existing cross-border settlement rail and close to what card networks deliver at checkout.

Every transaction costs a tenth of a cent per transfer, cheap enough for cross-border payments to undercut ACH and for agent-to-agent micropayments to survive their own fee.

In April 2026, Visa joined Tempo as an anchor validator after six months of joint engineering with the Tempo team, taking its place alongside Stripe and Zodia Custody, Standard Chartered’s digital-asset subsidiary. Visa’s cross-border settlement business runs on correspondent-bank rails that Tempo is designed to bypass, which made its decision to operate a validator node a tell about where the industry expects this to go.

The stack closed in April 2026. For our $200 from Berlin to Singapore, every fee on every layer was now Stripe’s.

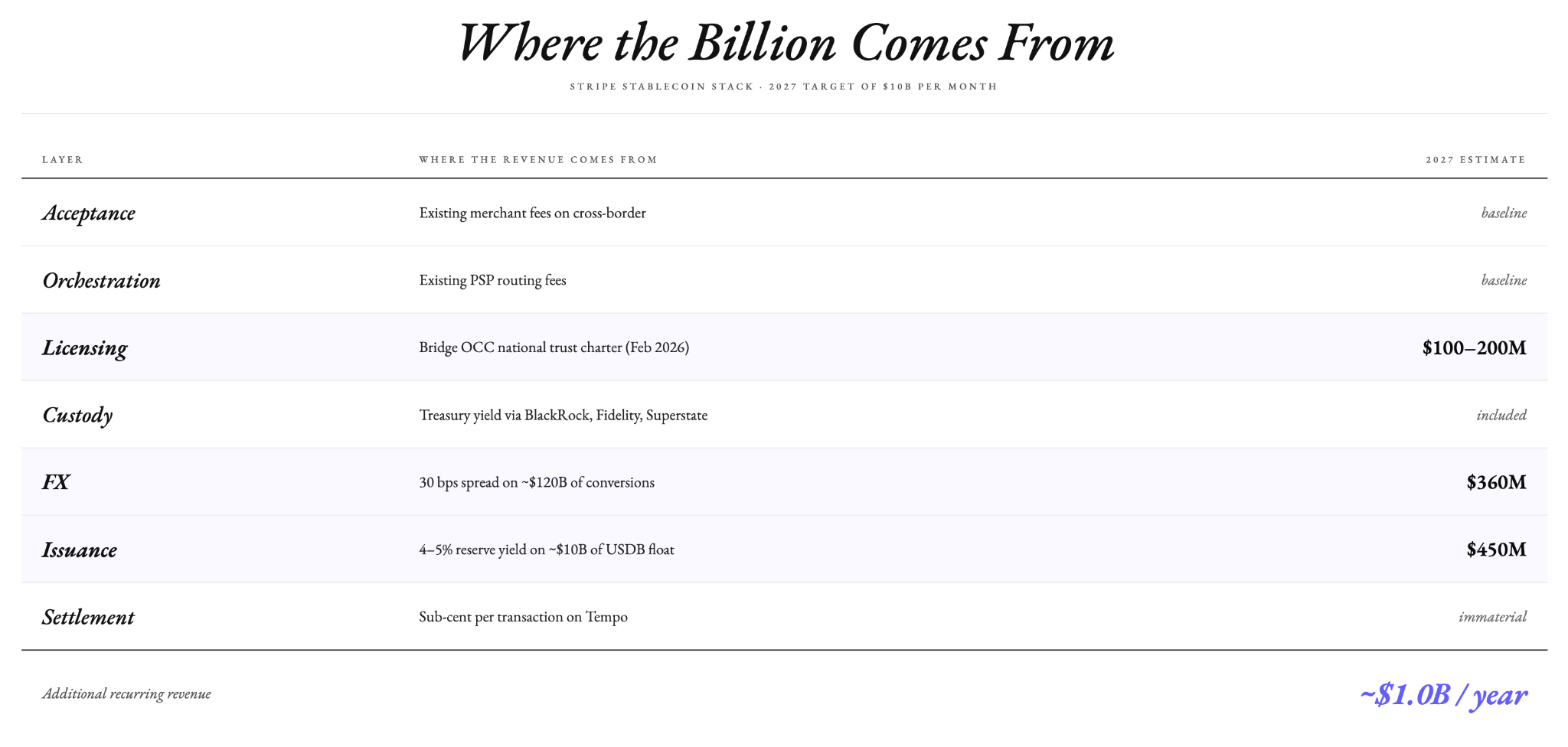

A billion in additional revenue

If the Bridge-Tempo stack can achieve a monthly target of $10 billion a month, it will generate roughly $1 billion a year in additional recurring revenue, on top of the merchant fees Stripe already collects on cross-border traffic. The ceiling is substantially higher than the 2027 target; Tether generated more than $10 billion in net profit in 2025 on roughly $175 billion of USDT in circulation, and that was the take from one layer of the seven Stripe now controls.

Here is how Stripe can make $1 billion with its vertical integration.

Acceptance and Orchestration are Stripe’s existing merchant fees on cross-border transactions and the baseline that the new stack protects. Nothing new here.

Licensing keeps $100 to $200 million a year inside Stripe. All the licences that Bridge acquired carry the regulatory coverage for cross-border dollar flows directly, eliminating the partner-bank licensing fees Stripe would otherwise pay on that volume.

Custody is a small cost line on the reserve balance. Bridge retains the Treasury yield that flows through BlackRock, Fidelity, and Superstate.

FX earns Bridge a ten-to-fifty basis-point spread on every stablecoin-to-fiat conversion. At $120 billion of annual volume and an average 30-basis-point spread, the FX layer generates roughly $360 million a year.

Issuance earns the reserve yield on USDB’s Treasury backing, roughly 4% to 5% in the current rate environment. At the 2027 volume target, an expected float of roughly $10 billion contributes about $450 million. Tether’s $10 billion of profit came on roughly $175 billion of USDT.

Settlement earns sub-cent per-transaction fees on Tempo and is immaterial as a revenue line at any realistic volume.

Across Licensing, FX, and Issuance, the 2027 target amounts to roughly $1 billion in potential annual revenue. That’s about 15% additional revenue every year. As the supply of USDB grows, Stripe earns yield on it just like Circle and Tether do on USDC and USDT backing, respectively. This becomes additional revenue for Stripe.

The stack describes a world where people pay for things. But we are also entering into a time where agents will pay for things. Stripe is building a second stack where software pays for things.

Gartner forecasts that AI agents will intermediate $15 trillion in global B2B spending by 2028. McKinsey expects agentic commerce to orchestrate roughly $3 to $5 trillion by 2030, while Bain estimates that US agentic commerce could reach $300 to $500 billion in the same period.

What is actually settling on agentic rails today is closer to a rounding error. Bloomberg reports that Coinbase’s x402 processed about $24 million across 94,000 buyers and 22,000 sellers in a single 30-day window in early 2026. The point is that the gap between estimates and what’s happening now is massive. If the forecasts even partially come true, companies that get a take rate on every dollar moved by agents will win. If they don’t, Stripe still owns the merchant network and the cross-border revenue stack it already monetises today.

Stripe has been assembling the pieces of the agent stack on different rails since before Tempo existed as a product.

The wallet layer is Privy, the infrastructure company Stripe acquired in June 2025. At the time of the deal, Privy powered more than 75 million accounts across over 1,000 developer teams, orchestrating billions in transactions. Privy’s embedded wallets live inside the applications developers are already building, with login via email and keys split across secure enclaves so no seed phrase ever touches a user. Every agent spun up against a Privy-backed application inherits a wallet at creation. The wallet becomes a default rather than a setup step.

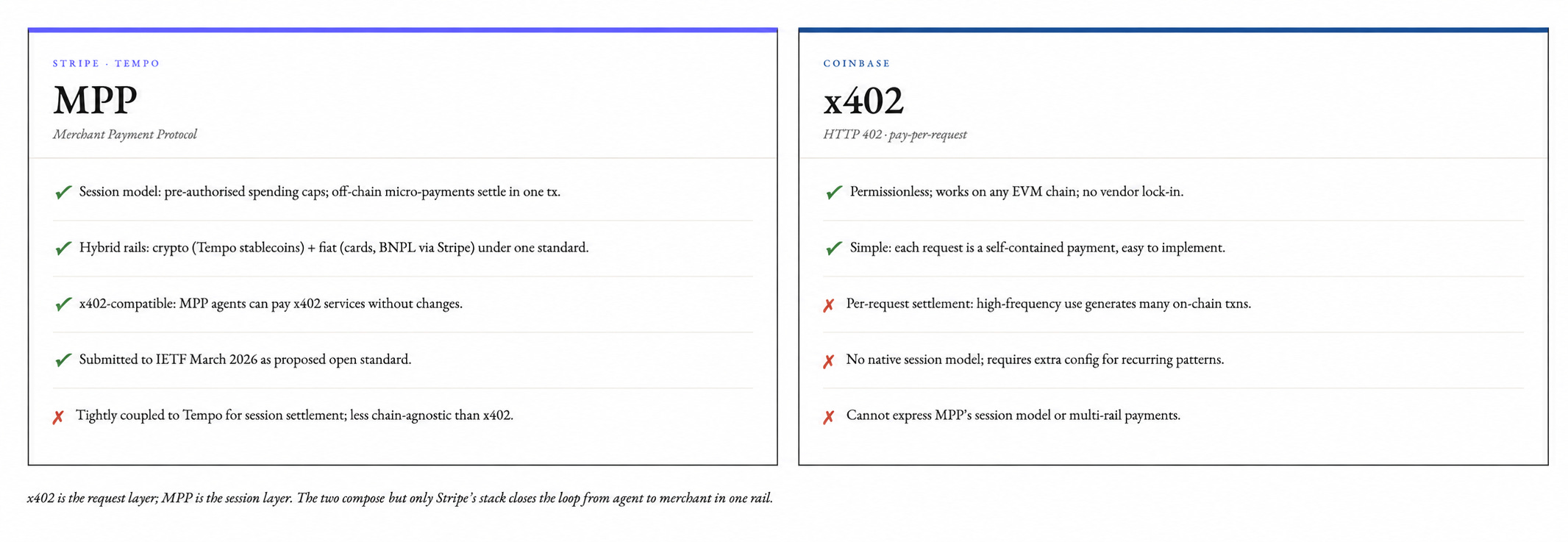

The rails are the Machine Payments Protocol (MPP), launched alongside Tempo’s mainnet in March 2026. MPP is a specification, co-authored by Stripe and Tempo, for how software makes requests and payments. It resurrects HTTP 402, a status code defined in the original HTTP specification as “Payment Required” and left dormant for nearly 30 years.

MPP can do everything x402 does, and more. It can handle simple per-request payments, but also supports sessions, where many small payments are grouped and settled once. x402 doesn’t support that. That means MPP can work with x402-style services without changes, but not the other way around.

Within its first week, MPP was integrated across more than 50 services, including OpenAI, Anthropic, Google Gemini, and Dune Analytics on the AI side, and purpose-built agent-commerce services like Browserbase (pay-per-session headless browsers), PostalForm (programmatic physical mail), and Parallel Web Systems (per-call web access). Visa contributed to the MPP specification alongside Stripe and Tempo.

Stripe’s stack is the first end-to-end position in that world. Privy issues the wallet. MPP structures the request. Tempo settles it. USDB carries the value. Stripe remains the merchant of record, earning its acceptance fee on a rail that costs a fraction of a cent to operate. If Gartner’s directional number is even half right, the ceiling on this stack is well above the cross-border merchant volume.

Ethereum, Tron, and Solana moved the trillions of dollars of stablecoin volume. Then why are companies like Stripe trying to launch their own chains and hoping that they will attract enough volume? About 15%-20% of the current stablecoin volume can be considered non-speculative as per Visa. The share of stablecoin use in daily commerce, i.e., the non-speculative share, can only grow when stablecoin rails are integrated into merchant networks. It is difficult for general-purpose chains to do that.

This is where the idea of Tempo, Arc, and Plasma starts to make sense. The argument for the new chains does not rest on Ethereum or Tron breaking down. General-purpose chains are at the bottom of the entire stack. Besides settlement, six other functions need to be in place to complete the value chain. And it will happen for whoever gets there first.

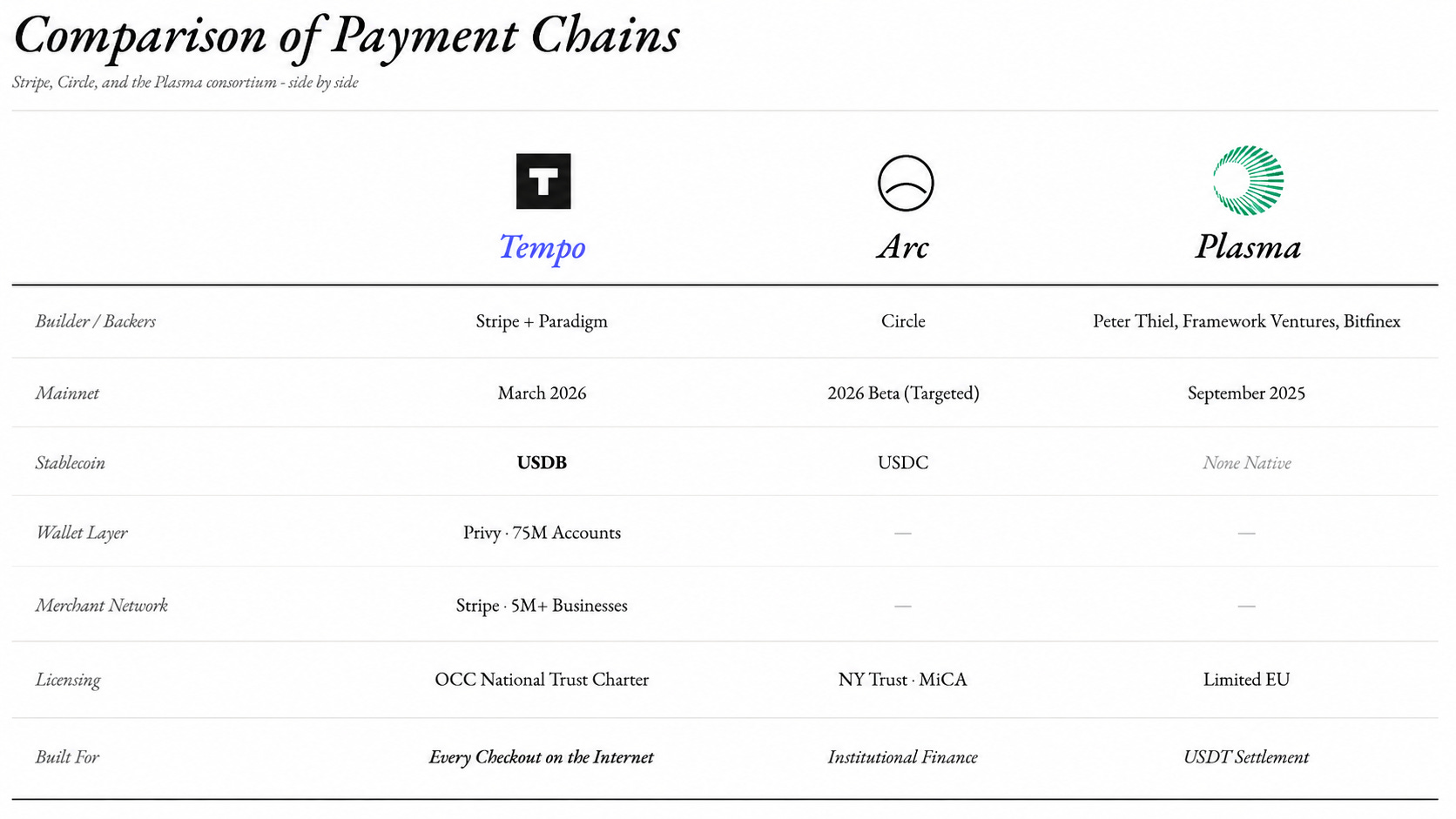

Tempo is not the only operator making this bet. Arc and Plasma are parallel attempts with different parts of the stack already in hand.

While payment chains are optimised to capture more of the traditional settlement business from merchant flows, existing chains are far ahead in financial speculation use cases. The volume of chains like Tron, Solana, and Ethereum is orders of magnitude higher than payment-specific chains right now. These chains also offer much more liquidity. But the bet is that the use of stablecoins for so-called genuine businesses will be as much, if not more.

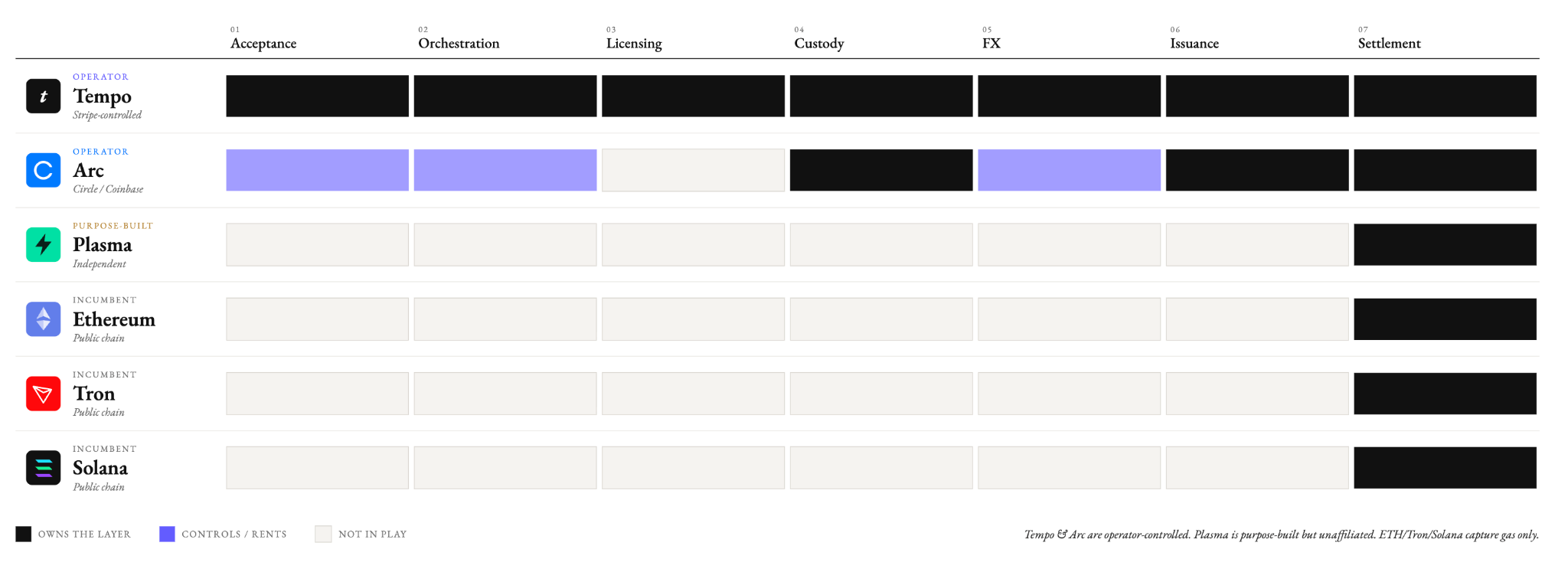

The following image shows how these new chains, especially Tempo, are geared towards the payments use case.

The six chains fall into three categories. Tempo and Arc are operator-controlled stacks, owned by the commercial entity that also owns the issuance and the distribution. Plasma is purpose-built for stablecoin payments but independent of any issuer or merchant network. Ethereum, Tron, and Solana are the incumbent public chains hosting the bulk of today’s stablecoin volume. The public chains, for all their current dominance in volume, capture only gas.

Every layer except acceptance and orchestration is capital-intensive but buyable. Bridge cost $1.1 billion and delivered issuance, FX, and licensing in a single transaction. Privy was a smaller check and delivered 75 million embedded wallets. Ithaca was an acqui-hire. Spinning up a new chain like Tempo is not a big deal these days. MPP is an open specification that anyone can clone. Five of the seven things on the stablecoin payments stack can be assembled for a few billion dollars and a two- to three-year roadmap.

Acceptance and orchestration are the points where you interface with the customer. You can rent the highly desirable access to these layers. You will take a long time to clone them. You can issue stablecoins like Circle and Tether or build a new chain like Plasma. But you cannot buy into the checkout flow of five million merchants. Adyen has scale but a different developer footprint. PayPal has consumers rather than a merchant API relationship. Stripe is the landlord now, and every stablecoin issuer that wants to reach commerce has to negotiate rent with the landlord or build its own checkout flow.

What Stripe built over fifteen years in checkout integrations and developer trust is the asset that the image does not show. The stablecoin stack is the monetisation wrapper on top of it. Bridge, Tempo, Privy, and MPP are tools that turn an existing moat into rent on every new transaction type, including agent payment volume that does not yet exist.

Circle can match Tempo, USDB, Privy, and MPP given enough time and engineering. What Circle cannot match, and what Tether cannot match, is Stripe’s merchant network. Everything else in this story is Stripe installing toll booths on a highway it already owns.

The last mile is the moat

PayPal launched in 1998. Wise in 2011. Revolut in 2015. Every few years, a digital remittance company arrived with better rates, better UX, and we felt Western Union was done for sure. But not yet. If you go to Argentina, the best way to swap your dollars for pesos is Western Union. It moved roughly $76 billion in consumer-to-consumer transfers last year, and its network runs to 500,000+ agent locations across more than 200 countries.

Look past the agents. The real asset is the postal system.

Western Union is wired into the post offices of more than 100 countries. It rents the last mile from post offices of different countries.

Visa did the same in 1958, when BankAmericard piggybacked on the branch networks of every bank willing to sign. Safaricom ran the same playbook with M-Pesa, turning airtime resellers into cash-in and cash-out agents and pushing ~$300 billion a year in transaction volume through a telecom’s distribution. Alipay did the same by living inside Taobao. Tencent won payments without a single bank branch, because WeChat Pay was integrated into a messenger with 1.3 billion monthly users.

Every one of those landlords had a statutory duty to rent. Post offices are public infrastructure with an obligation to let anyone inside who can pay the counter fee. Bank branches under the old correspondent regime had the same obligation as Airtime agents, who were licensed under telecom rules that forced open access. WeChat is the partial exception, and Tencent spent a decade being pressured by the PBOC to keep the rails interoperable. The post offices worked because the doors were held open by law.

Stripe’s doors are not.

Now look at what Stripe is doing with Tempo.

Stripe doesn’t need Tempo to find merchants. Stripe already has them. Its 2025 annual letter reports more than 5 million businesses on the platform, $1.9 trillion in total payment volume for the year, 90% of the Dow Jones, 80% of the Nasdaq 100, and a quarter of all new Delaware corporations signing up through Stripe Atlas. That is the substrate. Tempo is what runs underneath it.

The pitch is straightforward. If you are already on Stripe, the chain is already there. Stablecoin settlement in real time, near-zero fees, and none of the 200-basis-point tax that Visa and Mastercard have been collecting for decades. What the merchant sees is a cheaper invoice and a cleaner reconciliation file. They don’t know or care whether the chain is used for settlement. If it’s faster and cheaper on existing rails, it gets a thumbs-up from the merchants.

While Stripe has the distribution for the payment use case, general-purpose chains rule the speculation use case.

Ethereum, Solana, and Tron carry real stablecoin volume. Tron alone clears more than $20 billion of USDT on an average day. This volume lives and dies with wallets held by traders, OTC desks, and remittance corridors. Public chains own the trading layer, and hold roughly 42% of all circulating USDT

The commerce layer sits behind Stripe, Adyen, and a dozen PSPs whose merchant contracts were signed a decade ago.

Plasma tried to shortcut the problem by buying liquidity directly. The TVL dropped from the peak of $6.3 billion to ~$1 billion as the incentives dropped, as the price of the XPL token dropped from ~$2 to $0.10. The thing is, you cannot bribe your way into a merchant integration. That takes years, licences, enterprise sales teams, and the kind of contracts that do not get signed on Twitter.

Arc has Circle behind it, which buys it USDC distribution across every major exchange and a growing share of fintech treasury stacks. Useful, but being in Coinbase is not the same as being inside the checkout flow of a US SaaS business billing a European enterprise customer. Stripe is the one sitting there.

The existing merchant network is the worldwide network of post offices. Merchants are vendor-locked into their payment service provider. They don’t care which chain their vendor points to. As long as the terms are fair, they will keep using the same vendor, whether the chain is Solana or Tempo.

There are two broad use cases of stablecoins. Financial speculation and commerce. Public blockchains have dominated and will dominate the first part. For the second part, we need existing merchants and existing payment flows. Existing companies like Stripe are in a much better position to capture this market.

Stablecoin chains by themselves don’t make sense unless you already have an existing volume. Owning a stablecoin chain doesn’t guarantee that you will make money. The stablecoin chain will be a loss leader. It lets you own payments end-to-end, so that once you own the customer, you can earn money from other services built on top of it. The moral of the story is that Stripe doesn’t need Tempo to win commerce. It needs Tempo so that it doesn’t have to share.

Watching fintech coming for crypto,

Saurabh Deshpande

the "last mile is the moat" framing hits hard. we match this point with what VCs say for sure: the founders who control merchant flow always beat the ones with better infra

The seven-layers framing is the right lens, but the part most analysts will skip is timing. Stripe shipping its own chain the same week AWS Bedrock made every agent on its platform a USDC buyer by default isn't a coincidence — it's both companies pricing in agentic payment volume that doesn't exist yet on legacy rails. Whoever owns the chain owns the meter, and metering is the only durable margin in agent economics.