Going Institutional

ZKsync as a Call Option on Enterprise Adoption

Hello,

For the past year, DCo has been talking about how institutions are coming on-chain, but they’re coming on their own terms. They want privacy, compliance, and control, and they aren’t going to get those with products as they exist in their crypto-first form. Most of the institutional conversation has centred on infrastructure built by incumbents for incumbents, with Canton as the obvious example. We keep circling back to this question: can a crypto-native project, one that grew up in the open Ethereum world, actually serve institutions at scale?

ZKsync is one of the serious attempts to say yes, which is why it’s worth a close look.

This article walks through the stack and what Prividium actually does, why institutions might need their own chains and why they couldn’t have had them five years ago, how ZKsync compares to Canton in the race to become the institutional standard, and what the revenue model looks like across scenarios through 2028. If you were to bet on ZK, it has to be a low-probability, high-payoff bet, closer to an out-of-the-money option than a conviction hold.

TLDR;

Institutions are coming on-chain on their own terms. ZKsync is one way to bet on a crypto-native project serving them. The market is not pricing in the optionality of its success.

Teams have already built chains using ZKsync’s offering. These are live and some are thriving, which validates the stack’s technical capability. The enterprise narrative is a separate and still unproven claim. Prividium has institutional interest and early partners, but interest is not revenue. Whether it converts to paid production deployments is the open question.

ZKsync offers a comprehensive suite for institutional blockchains. No competitor currently offers everything they need while anchoring to Ethereum. The bet is that the full stack under one roof matters more than the relationships incumbents already have.

Most of the value in crypto is on networks that won the distribution game, not necessarily the technology game. Arbitrum and Base control ~70% of L2 TVL. But two shifts can change the market dynamics and anoint new winners:

Institutions are coming on-chain for real this time.

ZK tech has finally caught up in cost and speed. ZKsync sits right at that intersection.

The retail story is almost settled with clear winners so far. The institutional side is chaotic, with a few winners emerging, but far from over. It is also messier, with different trade-offs. Institutions care about privacy and control more than cheap gas.

The numbers back the narrative. BlackRock’s BUIDL fund peaked at $2.9B in AUM in mid-2025. As of mid-2026, AUM has settled to roughly $2.0–2.5B across eight chains. It is tradeable via Uniswap through whitelisted qualified purchasers. This is BlackRock’s first direct integration with DeFi infrastructure. JPMorgan’s Kinexys settles more than $2B daily, with cumulative throughput past $1.4T. The Canton Network, backed by Goldman Sachs, DTCC, and JPMorgan, reports over $6T in tokenised assets and 15M+ monthly transactions.

Tokenised equities grew ~2,900% in a single year, from ~$30M to roughly $963M. Stablecoins now settle $9T+ monthly on a base of $300B+ in outstanding supply. And the DTCC, the entity that clears virtually all US securities, has received SEC authorisation to create blockchain-based digital twins of equities and Treasuries it already holds. The infrastructure question for institutions is no longer whether to come on-chain, but what stack to build on.

This is not the first time institutions have tried to use blockchain. Around 2017-2018, a wave of banks attempted to create their own private networks. Those efforts largely failed for three reasons: the technology was immature, the engineering complexity was beyond what banks could manage internally, and the chains they built were silos.

The next attempt was to directly use public networks like Ethereum. That failed because of compliance risks, regulatory exposure, customer privacy laws, and the simple fact that banks cannot have their balance sheets and trading activity visible on public rails. The institutions that tried the public-chain route faced regulatory consequences that made it untenable.

What Institutions Want and Who Can Give It to Them

Public-by-default blockchains clash with how finance works. Banks cannot expose trade strategies, client data, or counterparty relationships on a public ledger. It is about competition more than regulation. So, even if regulation allows it, banks wouldn’t want this part to be wholly public.

The four requirements institutions have articulated through ZKsync’s consultations with banks, corporations, and governments are:

Privacy (transaction-level confidentiality)

Control (governance over who participates and what they can do)

Risk management (predictable throughput, SLAs, and failover).

Interoperability (connection to global markets without bridges).

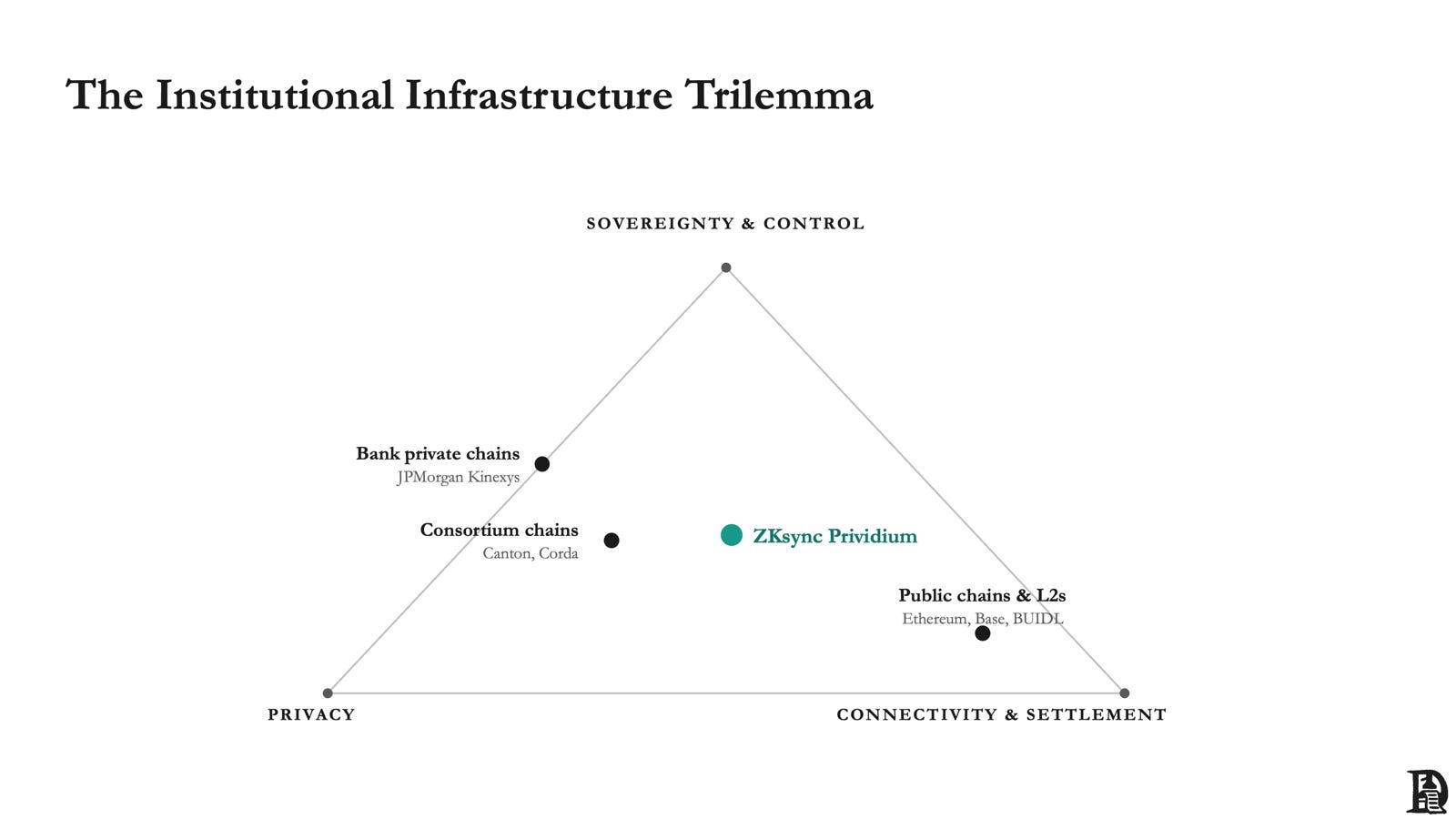

Institutions want a chain they control, privacy over balances and counterparties, and a way to reach public liquidity and settle on neutral ground. You can’t really have all of it at once. Almost everything on the market today gets you two corners and gives up the third.

Public chains and the assets issued on them, Ethereum, Base, BlackRock’s BUIDL, nail connectivity and settlement. They’re liquid and composable, but there’s no real privacy and you don’t control the chain. On the other side, you have bank-built chains like JPMorgan’s Kinexys and consortium networks like Canton and Corda. Those give you control and confidentiality, but they’re walled gardens with little reach into public liquidity, and their privacy leans on governance agreements rather than maths. Everyone has picked two and lived with the gap.

ZKsync’s whole pitch is that it doesn’t have to pick. Prividium lands in the middle of the triangle: a private chain the bank runs, confidentiality enforced by ZK proofs, and it still settles to Ethereum and can tap public liquidity when it needs to. That middle spot is the entire thesis. It’s also unproven. What it takes to actually get there is the rest of this piece.

Competition and the Standard War

Since the asymmetric part of the thesis depends on institutional adoption, the relevant competition is not just other public rollups. The most important comparison is the group of platforms competing to become the institutional standard for tokenised finance. The most relevant benchmark is likely Canton Network, not Arbitrum or Optimism. Arbitrum matters for retail L2 adoption. Canton matters for the institutional-standard race that underpins the non-consensus part of the ZK thesis.

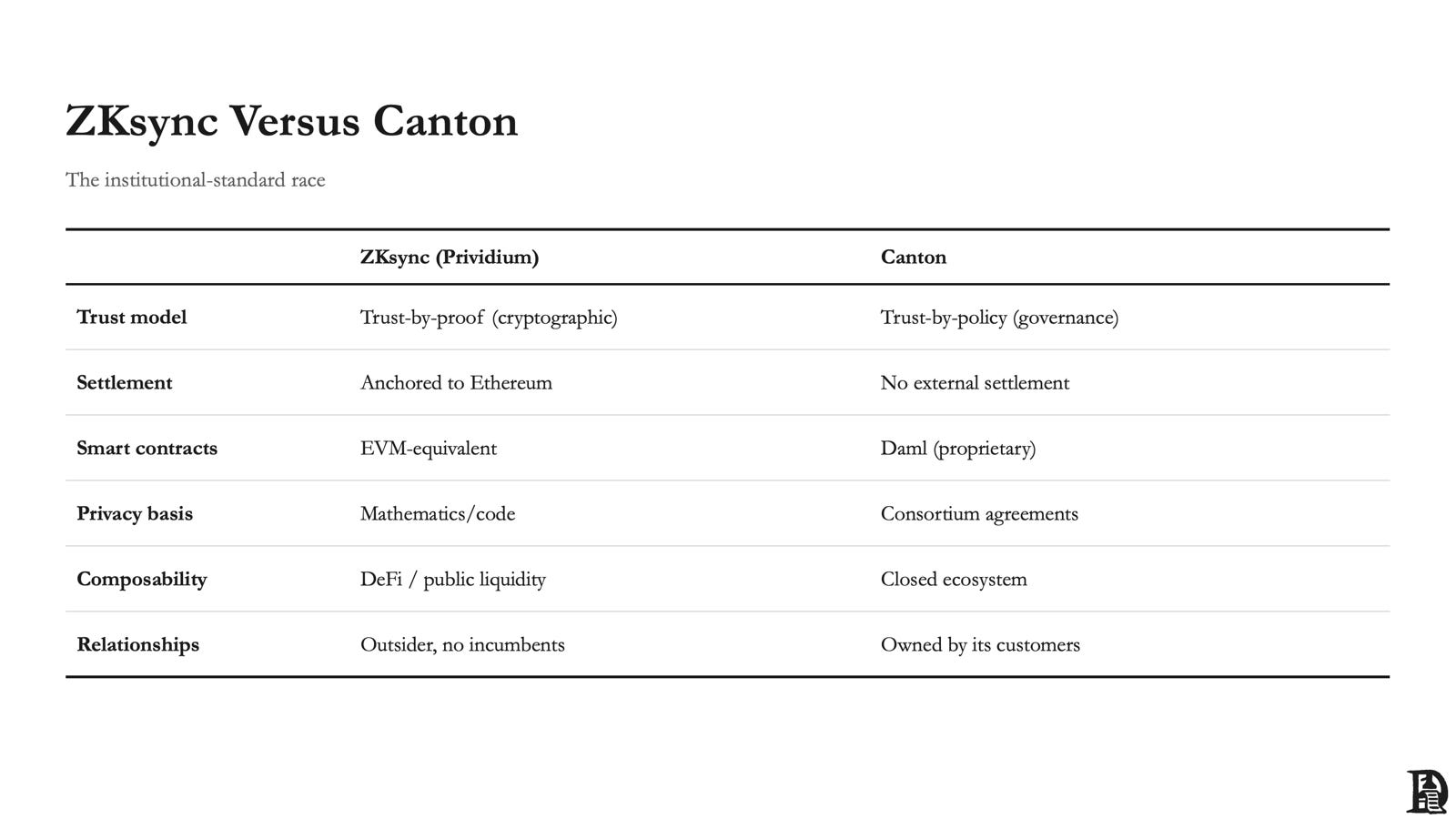

Canton is a privacy-enabled L1 blockchain backed by Goldman Sachs, DTCC, Citadel Securities, BlackRock, Nasdaq, and S&P Global. Today, its incumbent ownership appears strong, and the ZKsync team is candid that this is their biggest competitive hurdle. Canton has deep, established relationships in the banking industry built over the years. ZKsync is the newer entrant that banks do not have existing relationships with. In institutional sales, that matters enormously because banks default to vendors they already know.

But Canton’s technology tells a different story. It is a fully permissioned chain that uses Daml, a proprietary smart contract language, thereby limiting the developer pool and creating vendor lock-in. A Flashbots deep dive on Canton flagged that membership is permissioned, participation is subject to institutional gating, and only approved financial institutions may operate nodes.

The same research flagged that a single entity controlling sequencers can achieve “God Mode” over sub-networks, enabling potential history rewrites or unauthorised participant admission.

The security models are philosophically different. Canton follows trust-by-policy. It has a known validator set, contractual governance, and consortium agreements. If the operator is hacked or hits a bug, there’s no cryptographic fallback. ZKsync, on the other hand, is trust-by-proof. The correctness of every transaction is verified mathematically.

Canton’s model is similar to how banks work today. It works well for bilateral settlement between known counterparties in a single jurisdiction with aligned incentives. What happens when entities that don’t know each other want to work together? Many institutions operate across borders, counterparties, and time horizons. A consortium with differing priorities and competing political pressures behaves correctly until it doesn’t. That’s where policy-based trust hits its ceiling.

ZKsync’s model has multiple layers of redundancy. The bank runs its own Prividium chain and can freeze or halt it if something goes wrong. Proofs are aggregated on the ZK Gateway before reaching Ethereum, catching failures before settlement. Even if the ZK circuits themselves have a bug, the system doesn’t collapse because each layer intervenes independently. No single operator can break the whole thing.

ZKsync’s other lever is EVM equivalence. Institutions building on ZKsync can tap into the existing Ethereum/EVM developer ecosystem and tooling. Canton’s Daml creates a closed ecosystem. And Ethereum itself is the most secure database in the world, with 33–34 million ETH staked (around 27% of supply) securing it. If companies want to transact with each other on a neutral, highly secure settlement layer, that would be Ethereum. ZKsync gives you native access to that.

The point is that institutions have to decide between Canton’s familiarity and ZKsync’s openness and Ethereum connectivity. Institutions tend to default to familiarity. When Canton just works, ZKsync will struggle to pull institutions towards an Ethereum-connected product.

Buying Its Way Into the Room

ZKsync is not ignoring Canton’s distribution advantage. The team has been aggressively countering it through several channels: a complete overhaul of marketing and branding since fall 2025; the Prividium Breakthrough Initiative, which brought Citi, Deutsche Bank, Mastercard, and other companies together to explore Prividium deployments; strategic partnerships with established players like Cari Network (five US regional banks with $600B+ in combined assets) and Bitco to leverage their existing banking connections; and direct engagement with government regulators in Washington DC.

The public debate between ZKsync and Canton has also intensified. Canton’s position is that ZK proofs “make everything invisible” while Canton “ensures the right people see the right data”; ZKsync’s counter is that an open ZK system gets harder to compromise as the verifier network grows, while a permissioned trust model stays as strong and vulnerable as its weakest operator. Nethermind formally verified the correctness of ZKsync’s on-chain ZK verifier using EasyCrypt in 2025, completing the first formal proof of this kind and directly addressing Canton’s concern about undetected bugs in ZK circuits.

ZKsync’s Comeback

ZKsync obviously didn’t start with this institutional approach. It launched as an Ethereum L2 chasing the same retail users as everyone else, and it lost that battle. Base and Arbitrum took the distribution, and Era is a rounding error next to them. ZKsync rebuilt itself into a full ZK stack (a chain, a chain factory, a prover, an interop layer, and managed services) and aimed it at institutions through Prividium, a private and compliant chain that still settles to Ethereum. The technology is now competitive. The Atlas upgrade pushed throughput past 15,000 TPS with roughly one-second finality, and the Airbender prover sits at the top of the public leaderboard on cost.

ZKsync is an enterprise infrastructure company that happens to have a public chain, ZKsync Era. You can think of the public chain as ZKsync dogfooding their own products to show what can be built. Its positioning is to be the institutional-grade ZK-rollup layer for Ethereum.

Ethereum’s execution market has bifurcated. Users and liquidity have concentrated on a small set of distribution-heavy rollups, while a second wave of validity-proof (ZK) systems is competing on performance, settlement certainty, and institutional fit. According to L2BEAT, different flavours of L2s secure ~$40B of total value. Arbitrum at $17B and Base at $11B lead the pack with ~70% of the total TVL. In ZK rollups specifically, ZKsync is still at the start. ZKsync Era secures ~$230M and is rated Stage 0, while Starknet secures ~$400M and is rated Stage 1. If one looks only at public chains, ZKsync Era has a long way to go to catch up and might never meaningfully close the gap, given how far ahead the leaders are.

But thankfully, it doesn’t have to. The story here is not about who wins over retail users. That space is arguably overcrowded and concentrated with Arbitrum and Base. At the same time, acquisition and retention costs are unsustainable and rarely convert mercenaries into durable users. The more interesting question is who will win where privacy, verifiability and institutional controls matter. ZKsync has gotten in on the ground floor of Ethereum enterprise adoption. But that doesn’t automatically mean durable distribution and recurring fees. We don’t know whether a technical edge is even what decides institutional deals in the first place.

ZKsync is implicitly competing in two markets: (1) crypto-native consumers and DeFi activity on a public rollup; and (2) the institutional market for tokenised assets, where compliance and privacy are the prerequisites.

If ZKsync wins only as a public rollup, it competes head-on with distribution-heavy ecosystems (Base, Arbitrum, OP) where network effects already dominate. This is extremely tough, given that ZKsync has little market share.

If ZKsync’s enterprise strategy works, it expands the TAM and changes the competitive set: permissioned environments, middleware, and tokenisation platforms. This is where the next leg of growth will come from, and ZKsync is well-positioned to capitalise on this shift.

What it Actually Does

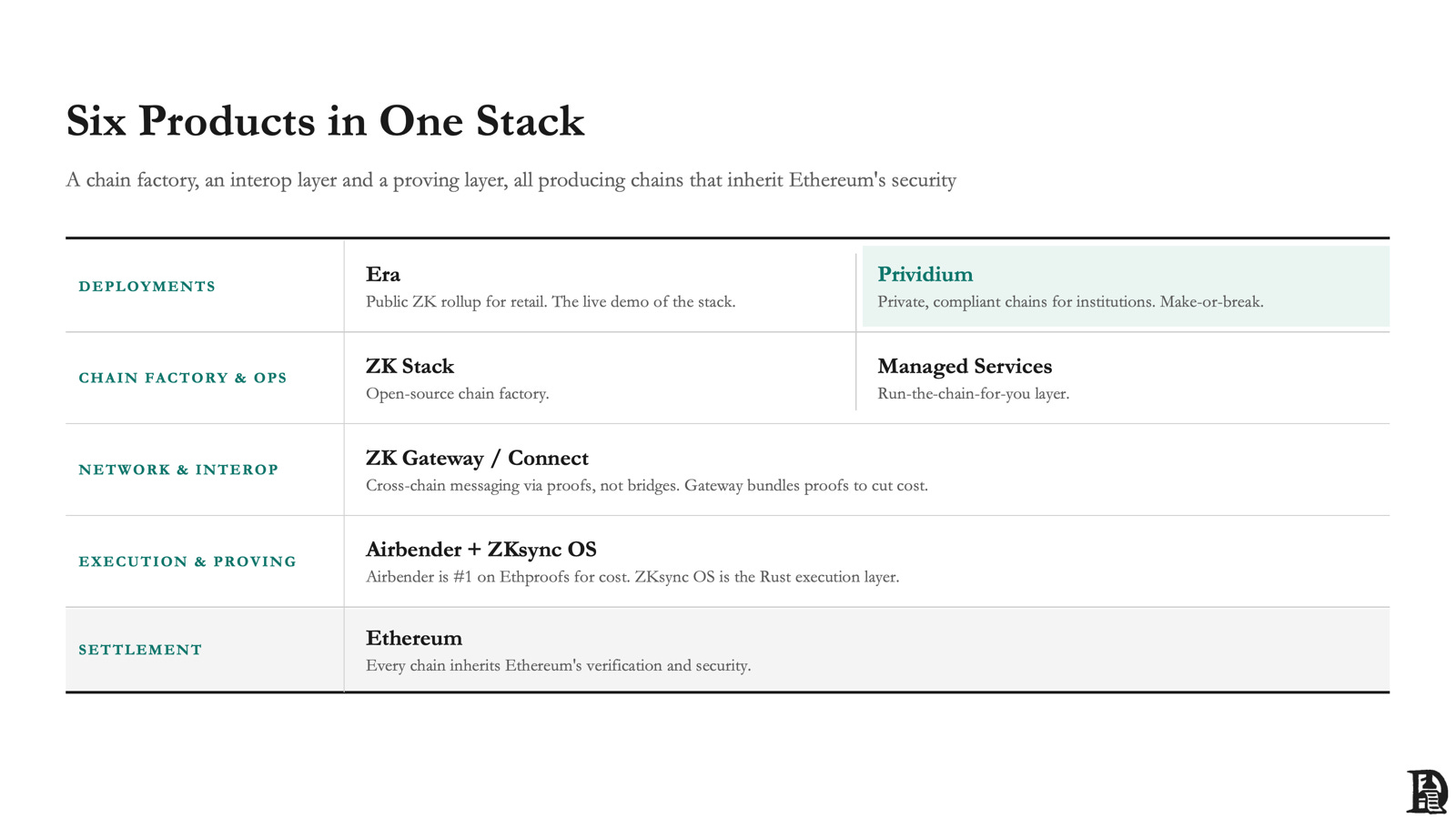

ZKsync is a full‑stack ZK infrastructure platform. For an institution standing up a tokenisation product, it covers everything from spinning up a chain to running it day-to-day. It combines: (i) a chain factory for launching your chains; (ii) a network and interop layer that makes those chains interoperable; and (iii) a proving and execution layer that compresses proving cost/latency for better developer economics.

With this stack, ZKsync covers the spectrum from public consumer DeFi to app‑specific chains to regulated and private deployments (Prividium) while inheriting Ethereum’s verification.

Privacy & Enterprise stack

Prividium is the star product for this thesis. The asymmetric upside depends almost entirely on it. It’s a permissioned Validium (a Validium stores transaction data off-chain rather than on Ethereum) deployment built on ZK Stack, and it gives institutions three levels of customisation.

Privacy with auditability: Regular users don’t see each other’s balances, counterparties or transactions. But the chain operators (say, banks) can see everything so that they meet compliance requirements.

Enterprise-grade controls: This is a way to apply controls that banks already have at the blockchain level. Who can join the network, what can they do, KYC/AML checks, role-based permissions, SSO login through systems like Okta.

Ethereum settlement: ZK proofs from the chain get posted to Ethereum. This gives you external verifiability (anyone can confirm the chain is operating correctly) without exposing any of the private data. You get Ethereum’s security guarantees without making your transactions public.

In a way, Prividium lets a bank run a private blockchain that behaves like an internal ledger but settles to Ethereum. The bank controls who can transact, what they can see, and how compliance is enforced. All of this happens while still getting the security guarantees of Ethereum and the ability to connect to public liquidity when needed.

ZKsync Prividium is an Ethereum-anchored platform that provides users with private, permissioned, compliant blockchain environments with one-second finality. Optimistic rollups structurally cannot provide the same at this point. While Arbitrum and Optimism dominate current retail L2 TVL with optimistic rollups, ZK rollups have evolved to offer high throughput and structural advantages for enterprises. In short, it seems increasingly clear that ZK rollups will win over optimistic rollups (ORUs) in the long run:

Performance superiority: Airbender, ZKsync’s proving engine, ranked #1 on the Ethproofs leaderboard (January 2026) for cost per proof and #2 for proving speed. This is significant because proving used to be the bottleneck that made ZK rollups expensive relative to optimistic rollups. It no longer is. And ZK rollups still have a structural edge on finality: transactions settle in about a second, versus the 7-day challenge window that optimistic rollups require.

Institutional requirements: Enterprises require instant finality for settlement - they cannot wait 7 days for transaction finality that optimistic rollups require. As per the Prividium paper, many companies specifically chose ZK for this reason.

Privacy capabilities: ZK cryptography can hide transaction details by default. For institutions that offer confidential settlements for a multitude of use cases, that’s a hard requirement. Canton’s privacy model depends on governance agreements between participants (trust-by-policy). ZKsync’s model relies on mathematics (trust-by-proof). The difference shows up when participants operate across jurisdictions with different rules and different incentives. Policy-based privacy holds up as long as everyone cooperates. Cryptographic privacy holds up regardless.

Why this is hard, before we get to anything else

Selling core infrastructure to banks is one of the slowest and lowest-converting sales processes in technology. The cycles run for years through procurement, risk, compliance, and security review, and most pilots never make it to production. An MOU or a consortium initiative is just the start of a conversation, far from recurring revenue.

Banks also buy from people they trust and expect to still exist in a decade. ZKsync, or Matter Labs, is a startup that comes with entity and centralisation risks. Canton’s backers are its own customers. That relationship gap doesn’t usually get closed with better technology alone.

The one thing working in ZKsync’s favour is that switching and integration costs go both ways. They make the first deal hard to win, but sticky once it’s won. So the thesis really hangs on landing a handful of genuine production deployments, not on a wide funnel.

Interest Is Not Revenue

Prividium launched in May 2025. ZKsync’s conversations with institutions sit at different stages. Live and in production is one thing, signed is another, and exploring is the top of the funnel and by far the biggest bucket. The first named institutional partner is Deutsche Bank, which is co-building an on-chain fund management solution with Memento (a TradFi-to-crypto bridge company). In October 2025, ZKsync announced the Prividium Breakthrough Initiative, with Citi, Deutsche Bank, Mastercard, and 30+ global institutions participating. These are all exploratory engagements at the top of the funnel, not paid production deployments. In institutional infrastructure, most exploratory engagements don’t convert.

A US regional banks consortium called Cari Network selected Prividium to power a bank-governed tokenised deposit network. They have combined assets exceeding $600B. Unlike stablecoins issued by non-bank entities, Cari’s tokenised deposits remain FDIC-insured and on each bank’s balance sheet. This positions Prividium as the banking system’s answer to the $300B+ stablecoin market.

On the managed services side, ZKsync has 11 signed chains and 15 more in negotiation, with a pipeline of ~40 total prospects. Additional institutional partners include Securitize ($200M+ in tokenised assets on Era) and Tradable ($2B+ tokenised assets), exploring tokenised deposit networks on Prividium. The 2026 roadmap describes moving from foundational deployments serving tens of millions of users.

ZKsync’s technology is in production. The ZK Stack powers:

GRVT: $85M TVL, $1B+ daily perp volume, processes 600K+ trades at under 2ms latency per trade. Mix of retail and institutional, with high-performance privacy-preserving execution.

ADI chain: ZK chain licensed by the UAE Central Bank, powering the DDSC dirham-backed stablecoin. Live in production.

Memento/Deutsche Bank: Prividium deployment under MAS Project Guardian (Project DAMA), co-building an on-chain fund management solution.

Abstract: ~50K DAUs, consumer-facing chain (retail use case, validating stack versatility).

Era itself: 700M+ total transactions, 291+ dApps, 162K daily transactions, $400M+ total value secured.

15 independent ZKsync chains are live in production on mainnet, with another 10 on testnet.

ZK Stack chains are already proving themselves in production. Perp DEX GRVT and consumer chain Abstract (L2 by Igloo Inc., Pudgy Penguins’ parent) have both used the stack to launch their chains. Abstract has ~50K DAUs, while GRVT shows the stack can support high-performance trading with $1B+ daily perp volume. These are not proofs of concept. They are live products handling real-world demands across multiple segments.

The most credible near-term commercial wedge is three specific use cases: 1) tokenised deposits, 2) treasury management, and 3) internal liquidity mobility. These solve an immediate, quantifiable pain point. A bank running a Prividium today can move liquidity between internal desks or across subsidiaries on private rails that settle to Ethereum, without waiting for the rest of the financial system to coordinate around a shared standard.

What's It Worth If It Works

The market currently values ZKsync as a failed retail general-purpose L2 and prices in little or no probability that it will become institutional infrastructure. The model below sizes the payoff.

ZKsync is one of the closest candidates to be Ethereum’s answer for enterprise chains, and it’s been moving in that direction. On that basis, we examine the various revenue streams and estimate how much ZKsync could generate through the end of 2028.

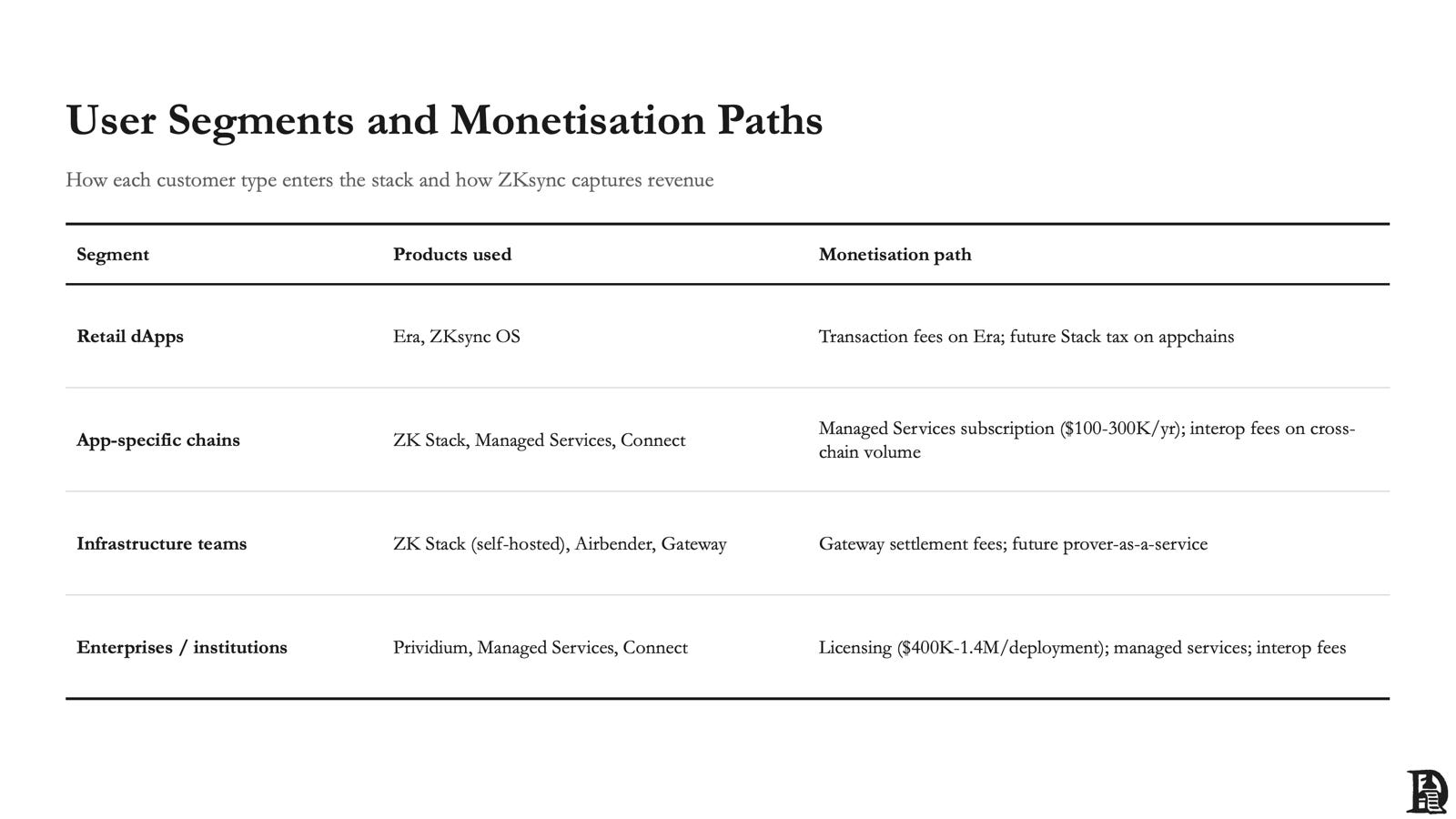

ZKsync’s product stack has three broad user categories: 1) developers, 2) crypto-native chain operators, and 3) institutions. Each enters the ecosystem at a different layer and pays in a different way.

Developers build on Era or use the SDKs to generate transaction fees. Chain operators deploy their own chains using ZK Stack and pay for Managed Services subscriptions to handle sequencing, proving, and data infrastructure. Institutions come in through Prividium and pay enterprise licensing fees for private, compliant blockchain environments coupled with managed services.

All the potential users or customers have different entry points into the stack. But all of them have the freedom to move across the stack once they are in. A chain operator that starts with a basic ZK Stack deployment might later upgrade to Managed Services, and an institution evaluating Prividium will likely need managed infrastructure bundled in. Each layer creates a fee rail that compounds as adoption deepens.

Where the Money Comes From

Each of the six possible revenue lines above is about a specific part of the ZKsync product stack. Here is what drives each one and why we think it can scale.

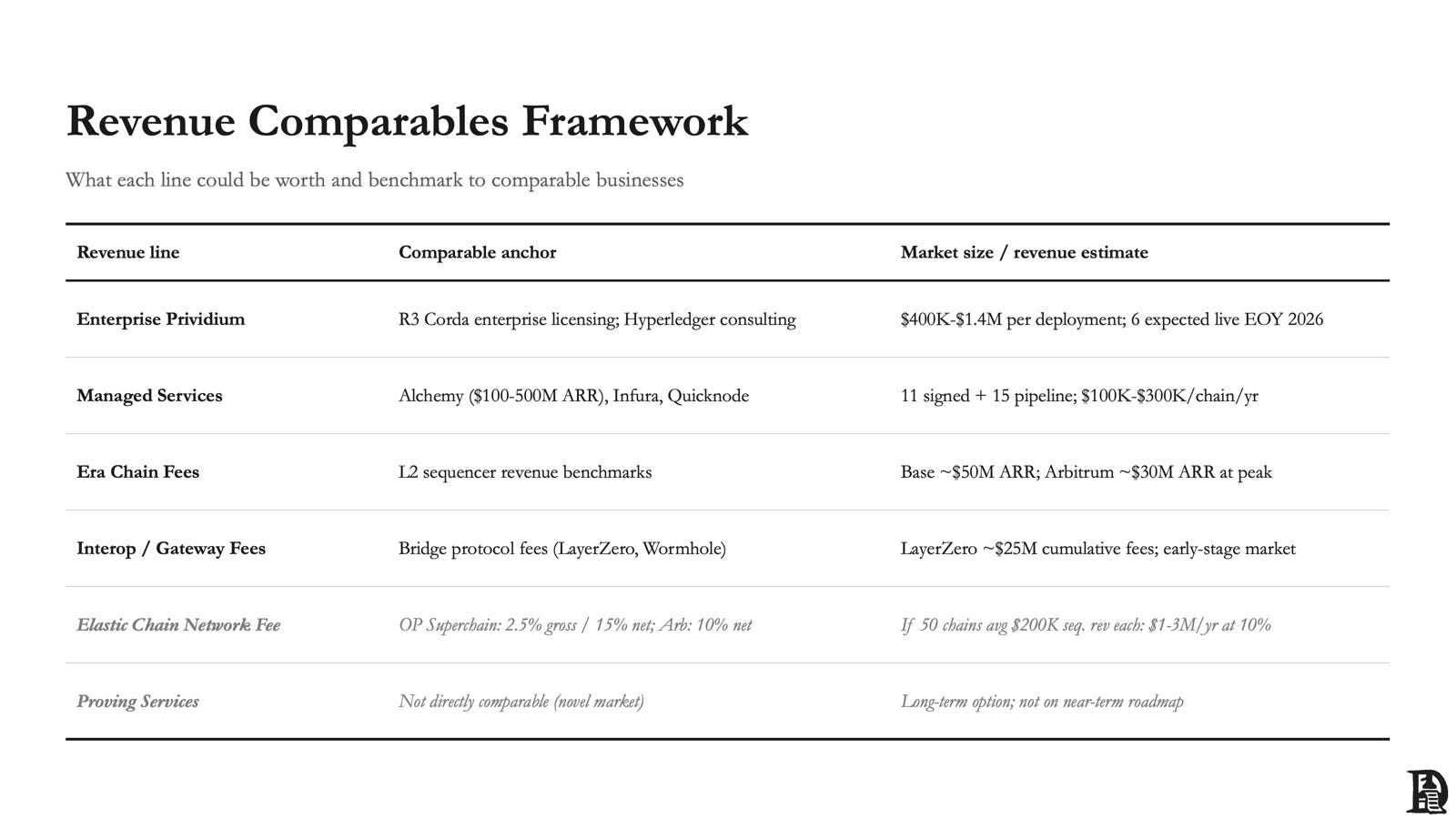

Enterprise Prividium will decide ZKsync’s fate, and it’s also the least proven. Institutions need private blockchain environments that are also compliant, and Prividium is one of the few products that deliver privacy, access controls, and Ethereum settlement in a single package. Institutions can either deploy through Prividium and run it themselves or hand it to ZKsync via managed services. Six Prividium deployments are targeted to be live by the end of 2026, though that’s a target, not a commitment. The early use cases here are tokenised deposits, treasury management, and bank-to-bank settlement. If those work, they open the door to repo, FX, and securities settlement. Given the scope, this is the line that makes or breaks the thesis.

Managed Services is the steady-state subscription business. As mentioned earlier, if you would rather not run a chain, ZKsync does that for you. Teams that want to run a ZK Stack chain without managing sequencing, proving, RPC, indexers, and data services themselves can pay an annual subscription. The subscription will be a cheaper option than running DevOps by yourself. This shifts ZKsync from cyclical on-chain fee revenue to more predictable recurring income, with room to expand through premium add-ons like private DA, dedicated regions, and priority support. There are already 11 signed chains and 15 more in negotiation.

Era Chain Fees are the most straightforward line: user transaction fees on ZKsync’s public L2. This is live today, but it is not the primary growth driver. Era serves more as a proving ground for the technology than as a revenue engine in its own right. That said, with 700M+ total transactions and 291+ dApps, the stack demonstrates it works at scale.

Interop / Gateway Fees become relevant with scale. ZKsync Connect and Gateway went live in June 2026. The idea is that every cross-chain transaction routed through the Elastic Network pays a small protocol fee. As the volume of cross-chain messages grows, ZKsync can charge a small fee per message.

Elastic Chain Network Fee is speculative based on Arbitrum and Optimism stacks charging 10% on the net revenue and 2.5% on gross revenue, respectively. Although ZKsync doesn’t currently enforce this, as the Elastic Network grows, it remains a credible future lever.

Proving Services is also speculative. Not every chain that wants ZK proofs will build its own prover. Airbender currently sits at #1 for cost per proof on the Ethproofs leaderboard and at the top tier for proving speed. If proving-as-a-service becomes an industry norm, ZKsync is well-positioned.

The table below maps each revenue line to market comparables and an estimated revenue range.

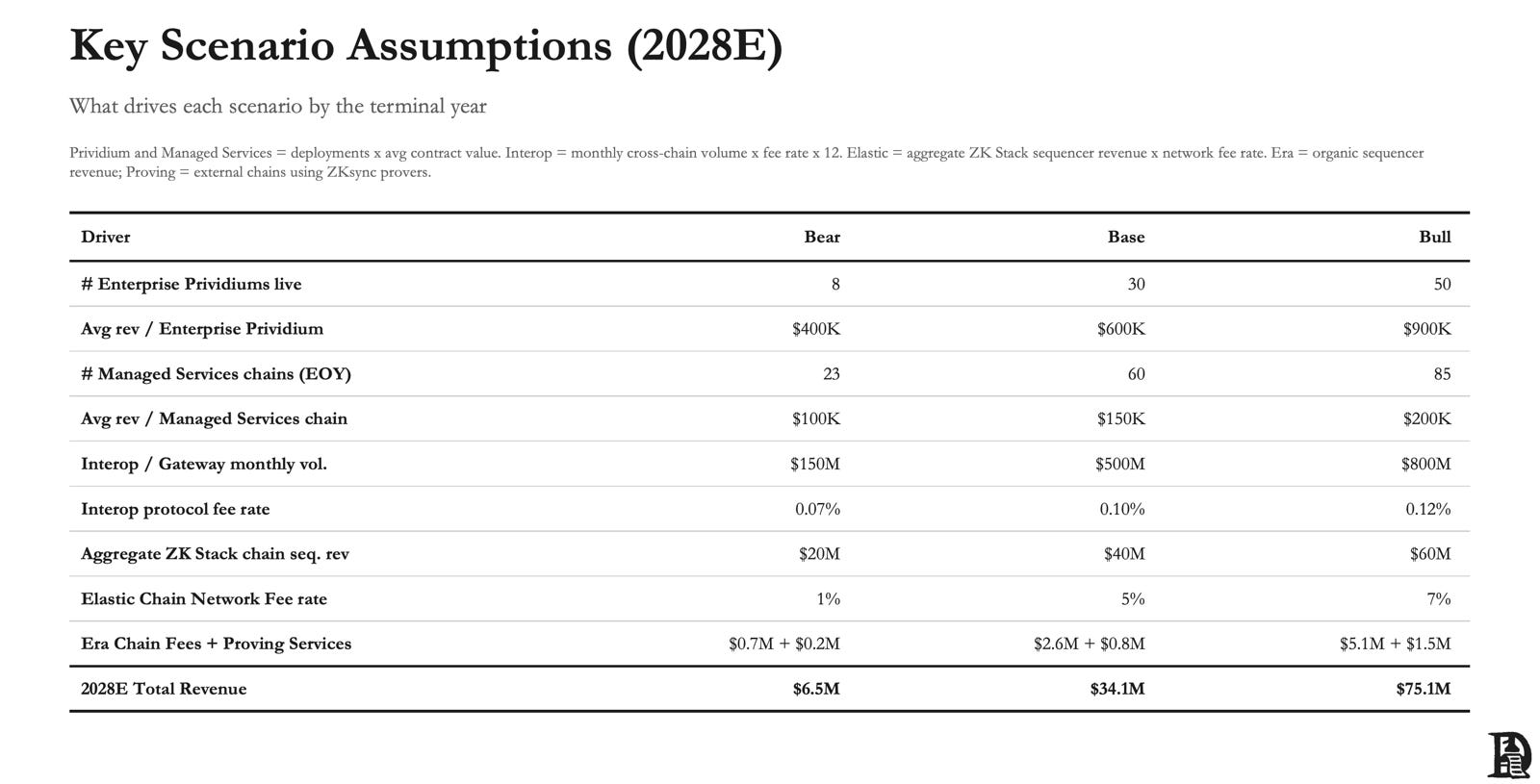

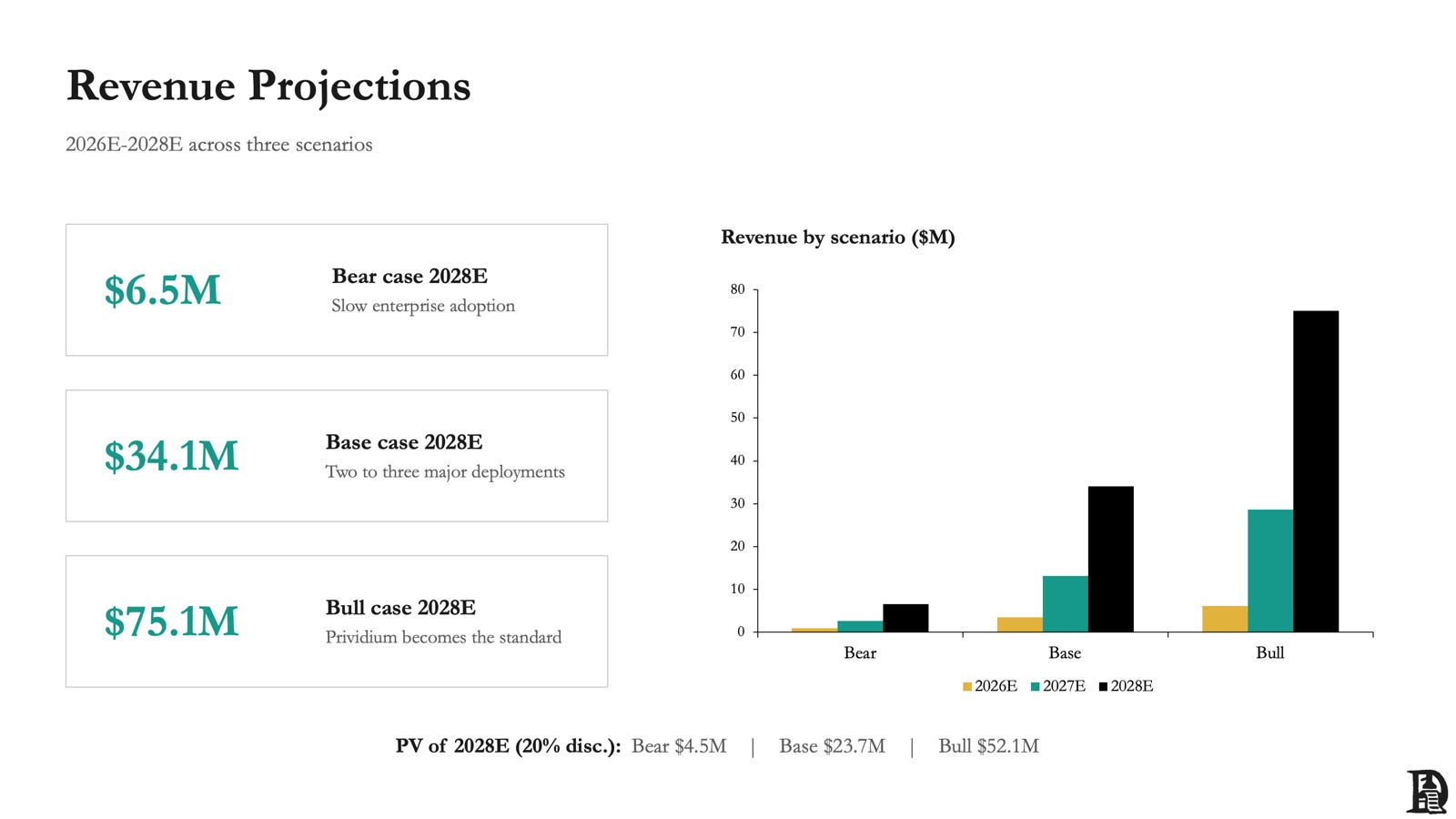

ZKsync could generate about $4-7 million in revenue in 2026. The largest driver for this would be the enterprise Prividium deployments. If six Prividium deployments are live by the end of 2026, with an average revenue of ~$400k-$600k, they will generate $2.4 million to $3.6 million. Managed services are the second pillar. 15 of these at the end of 2026 will amount to ~$1.5 million to $3 million. The Era chain and interop gateway are unlikely to be heavy contributors this year. The remaining two streams will only start contributing once other lines solidify.

We would normally take the 2026 estimate, apply a multiple, and assess potential valuations. But we can’t do that because ZKsync’s institutional push began around the second half of 2025. Given how time-consuming the sales process is for banks and financial institutions, it will take at least three years to validate the ‘enterprisification’ thesis. This is why we built the model out to 2028. The table below shows assumptions used for 2028 revenue contributions across all revenue streams.

We bring those revenues back with a 20% discount rate. So this is what revenues under different scenarios look like.

So where does this leave us? Step back from ZKsync for a moment. The trend that keeps winning in crypto is tokenisation, not token issuance. We wrote about this recently. Investors have stopped paying up for low-revenue governance tokens, and value has moved to assets with real revenue, real moats, or plain equity. Stablecoins were the first wave, and on-chain stocks are the second. The logical progression is that blockchains become the place where the world’s assets are issued, traded, and settled. And these assets will mostly be issued by large institutions.

What’s clear is that institutions will use blockchains. But we don’t know how or which blockchains. Do they build their own chains, adopt crypto-native infrastructure like ZKsync, or stick with the familiar vendors already in the building? And how big a shift is this really?

Moving settlement and record-keeping from fully centralised systems to a more decentralised version could be a generational re-architecture of financial infrastructure, comparable to the move from paper to digital. Or it could end up as a ‘not-a-big-deal’ upgrade that mostly preserves the existing power structure. Then there’s the question that decides whether any of it holds together: once a dozen institutions are each running their own environment, how do those systems talk to each other? We don’t have answers yet.

Our own view is that this is a bigger change. Can crypto-native projects be useful to this tokenisation trend? The time and environment feel right for it. The next phase of crypto is about bringing the world’s best assets on-chain, and that doesn’t happen without institutions. Whoever builds the rails they settle on and connects those rails to each other captures the most value of this cycle. ZKsync is one of the more credible crypto-native attempts to serve as that layer for Ethereum, which is why it’s worth watching. The incumbents have the relationships; ZKsync has the architecture and the bet on open networks. Which of those matters more is what the next two years will decide.

Exploring how crypto expands finance TAM,

Saurabh Deshpande