Asset Wrapped Equities

When Tokens Go to Stock Markets

Hello!

Newton is now known for his work on gravity, but in his time, he had a different field of interest: the alchemy of finance. Or, the pursuit of trying to create gold out of materials like lead. His pursuit led him to explore theology. Modern day finance rhymes with his interest. We live in an age where financial engineering transforms lead into gold by combining the necessary elements.

In today’s issue, Saurabh explains how corporate treasuries are adding crypto to their balance sheet and generating a premium on their real value. MicroStrategy, a firm with a little over $100 million in quarterly revenue, holds close to 109 billion in Bitcoin. There are 80 companies around the globe exploring how to add crypto to their balance sheets. Traditional finance institutions love this, and have been paying a premium for both the volatility & the upside that comes with such stocks.

Saurabh explores the emergence of convertible bonds that helped create this thriving ecosystem, the risks that come with it & the firms exploring adding altcoins on their balance sheets. Reach out to us at venture@decentralised.co if you are tinkering with bridging TradFi with on-chain primitives.

On to the story..

Joel

Hello!

A software/business intelligence company with quarterly revenue of $111 million is somehow worth $109 billion. How did it achieve this monumental feat? It bought bitcoin with other people’s money. And the market now values it at a 73% premium compared to the amount of Bitcoin it holds. What is the alchemy behind this math?

Strategy (fka MicroStrategy) has created a financial mechanism that allows it to borrow money at almost zero cost to buy bitcoin. Using their recent $3 billion convertible notes from November 2024 as an example, here's how it works. The company issued convertible bonds that pay 0% interest, meaning bondholders don’t get regular payments. Instead, each $1,000 bond can be converted into 1.4872 shares of Strategy stock. But only if the stock price rises to $672.40 or higher before maturity.

When they issued these bonds, the stock was trading at $433.80, so it needs to jump 55% before conversion becomes profitable. If the stock never reaches that level, bondholders simply get their $1,000 back in five years. But if Strategy's stock soars (which it tends to do when bitcoin rises), bondholders can convert to shares and capture all the upside.

The genius is that bondholders are essentially betting on bitcoin's performance while enjoying the downside protection that direct bitcoin buyers don't have. If bitcoin crashes, they still get their money back because bonds are senior to stock in bankruptcy. Meanwhile, Strategy gets to borrow $3 billion for free and immediately buys more bitcoin with it.

But there's the key trigger mechanism: Strategy can force an early redemption of these bonds starting December 2026 (just two years after issuance) if their stock trades above $874.12 (130% of the conversion price) for a specified period. This "call provision" means that if bitcoin drives the stock high enough, Strategy can essentially force bondholders to convert to shares or get their money back early. This allows the company to refinance at even better terms.

This strategy works because bitcoin has delivered extraordinary returns, with an approximately 85% annual growth over 13 years and a 58% annual growth over the past five years. The company is betting that bitcoin will continue growing much faster than the 55% stock appreciation needed to trigger conversions, and they've already proven this works by successfully calling earlier bond issues and saving millions in interest payments.

At the heart of this structure sit three distinct perpetual preferred stock series: STRF, STRK, and STRD, each tailored to different investor profiles.

STRF: Perpetual preferred stock with 10% cumulative dividends and the highest seniority ranking. If Strategy misses dividend payments, they must pay all missed STRF dividends before paying any other stockholders, plus the dividend rate increases as a penalty.

STRK: Perpetual preferred stock with 8% cumulative dividends and middle seniority. Missed dividends accumulate and must be paid in full before common shareholders receive anything. Also includes conversion rights to common stock.

STRD: Perpetual preferred stock with 10% non-cumulative dividends and lowest priority. Higher dividend rate compensates for increased risk - if Strategy skips payments, those dividends are lost forever and don't need to be made up later.

Perpetual preferred stock lets Strategy raise equity-like capital that pays bond-like dividends forever, with each series customised for different investor risk appetites. The cumulative feature protects STRF and STRK holders by guaranteeing eventual payment of all dividends, while STRD offers higher current income but no safety net for missed payments.

The Strategy Scorecard

Strategy started raising funds to buy BTC in August 2020. Since then, BTC has gone from $11,500 to $108000, ~9x. At the same time, the Strategy stock price surged from $13 to $370, almost ~30x.

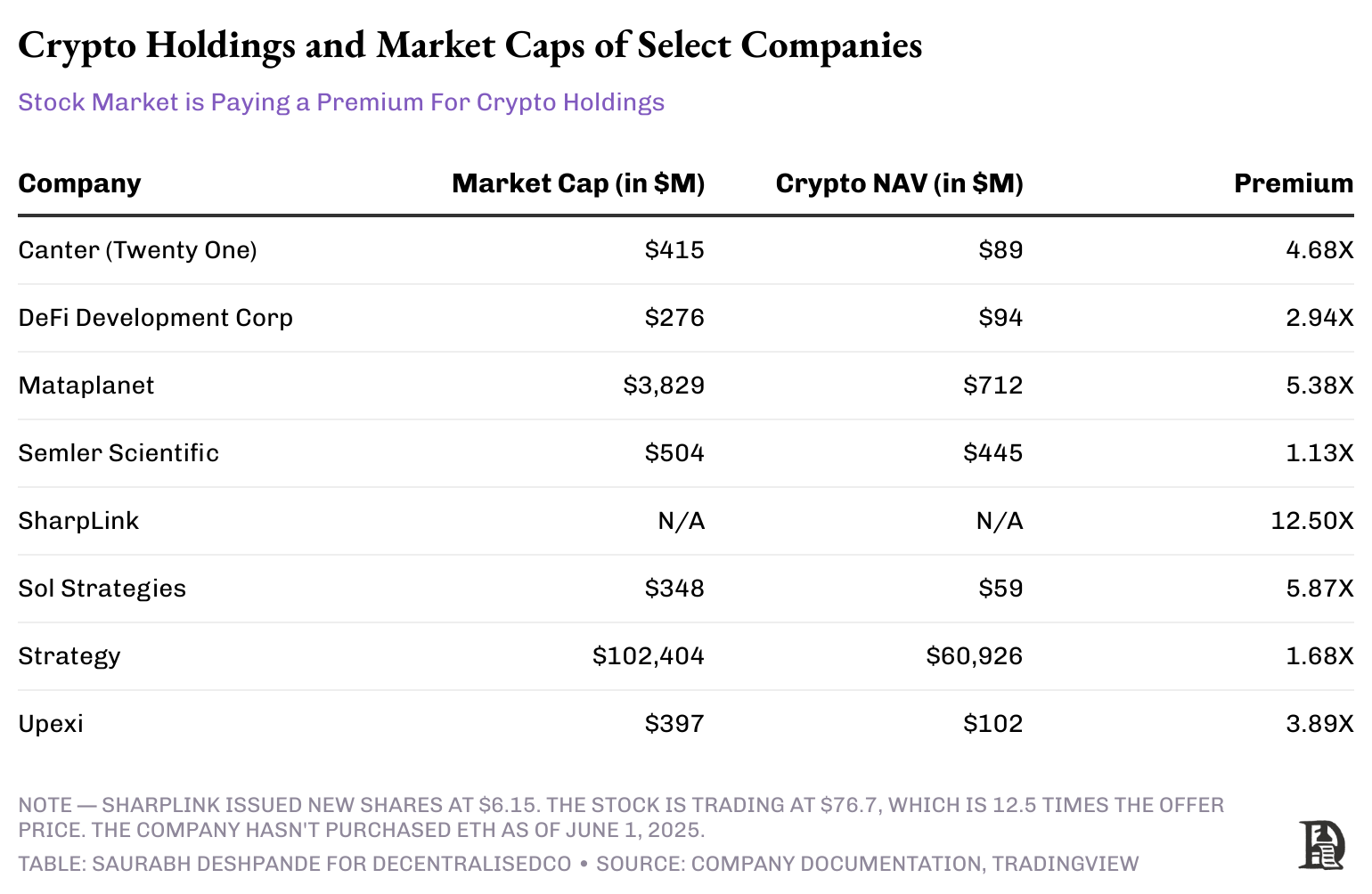

Strategy's regular business hasn't grown at all. They still make the same $100-135 million in quarterly revenue they always did. The only thing that changed is that they borrowed money to buy bitcoin. They now own 582,000 bitcoins worth around $63 billion. Their stock is valued at ~$109 billion, which is 73% more than their bitcoin is actually worth. Investors are paying extra just for the privilege of owning bitcoin through Strategy's stock.

As mentioned earlier, Strategy issued new stock to fund its bitcoin purchases. Since they started buying bitcoin, they've nearly tripled their share count, going from 95.8 million shares to 279.5 million shares (a 191% increase).

Normally, creating that many new shares would hurt existing shareholders because everyone's slice of the company gets smaller. But while the number of shares increased by 191%, the stock price skyrocketed by 2,900%. This means that even though shareholders own a smaller percentage of the company, each share became so much more valuable that they still came out ahead.

The Strategy playbook goes viral

Several companies with BTC treasuries have popped up, attempting to replicate Strategy’s success. One of the recent ones is Twenty One (XXI). It is a special purpose acquisition company (SPAC) led by Jack Mallers and supported by Brandon Lutnick’s (the son of the US Secretary of Commerce) Cantor Fitzgerald, Tether, and SoftBank. Unlike Strategy, Twenty One is not listed. The only way to get public exposure is through Canter Equity Partners (CEP), which seeded XXI with $100 million for a 2.7% share.

Twenty One owns 37,230 bitcoins. Since CEP owns 2.7% of Twenty One, they effectively control about 1005 bitcoins (worth roughly $108.5 million at $108k per BTC).

CEP's stock market value is $486 million, which is 4.8 times more than their bitcoin holdings are actually worth! The stock shot up from $10 to around $60 when its bitcoin connection was announced.

This massive premium means investors are paying $433 million for exposure to $92 million worth of bitcoin. As more companies like this emerge and their bitcoin holdings grow, market forces will eventually bring these premiums back down to more reasonable levels, though nobody knows when that will happen or what "reasonable" will look like.

The obvious question is, why do these companies trade at a premium at all? Why not go and buy BTC from the market and get that exposure? I think the answer lies in optionality. Who is funding Strategy’s BTC buys? It is largely hedge funds that trade bonds in the quest for delta-neutral strategies. If you think of it, this trade is similar to Greyscale’s Bitcoin Trust. The trust used to trade at a premium to BTC because it was closed (you couldn’t remove BTC until it was converted into ETF).

So you would keep BTC with Greyscale and sell GBTC shares that used to trade publicly. As mentioned previously, with Strategy’s bonds, holders can enjoy over 9% CAGR.

What can go wrong here? There is a risk of Strategy having to sell BTC to honour redemptions or interest payments. But how real is it? The total annual interest burden on Strategy is $34 million. With a gross profit of $334 million for FY 2024, Strategy is well positioned to service the debt. Strategy has issued convertible notes with maturities bearing bitcoin’s four-year cycles. They are far enough to let the downward price risk dampen. So, as long as BTC increases by more than 30% in four years, new stock issuance can easily pay for redemptions.

At the time of redeeming these convertible bonds, Strategy can simply issue new shares to the bondholders. This reference stock price, based on which bondholders will be paid, is mentioned in the issue. This price is ~30-50% higher than the stock price at the time of issuing bonds. This can only be problematic if the stock price is lower than the conversion price mentioned. In that case Strategy has to return cash. It can do so either by raising a new round of debt with more favourable terms, so that earlier debt is paid back, or by selling BTC to cover the cash.

The Value Chain ⛓

It obviously starts with the company trying to acquire BTC. But they end up using exchanges and custody services. For example, Strategy is a Coinbase Prime client. It has bought BTC using Coinbase and stores BTC with Coinbase Custody, Fidelity, and its own Multisig wallets. Exact numbers of how much Coinbase earns from Strategy’s BTC execution and storage are difficult to pinpoint, but we can venture a guess.

Assuming exchanges like Coinbase charge 5 bps for OTC execution for buying BTC on behalf of Strategy, for 500,000 BTC at an average execution price of $70,000, they earned $17.5 million from the execution. BTC custodians charge 0.2% to 1% as annual fees. Assuming the lower end of the range, for storing 100k BTC at the price of $108,000, custodians earn $21.6 million annually by storing BTC for Strategy.

Beyond BTC

So far, creating vehicles to give BTC exposure in capital markets has performed well. In May 2025, SharpLink raised $425 million through a Private Investment in Public Equity (PIPE) led by ConsenSys founder Joe Lubin, who also became executive chairman. Priced at $6.15 per share for roughly 69 million new shares, the round will finance the purchase of ~120,000 ETH, which will likely be staked later. As of now, ETH ETFs are not allowed to stake.

This type of vehicle, which also offers a 3-5% yield, becomes automatically more attractive than the ETF. Before the issue was announced, SharpLink was trading at $3.99 per share with a market cap of ~$2.8 million, and ~699k outstanding shares. The issue priced shares at a 54% premium over the market price. After the announcement, the stock jumped to a high of $124.

The newly issued 69 million shares represent ~100 times the current outstanding shares.

Upexi has a plan to acquire more than 1 million SOL by Q4 2025 while keeping cash burn neutral. The plan began with a $100 million raise by selling 43.8 million shares in a private placement round anchored by GSR. Upexi expects a 6-8% staking yield plus MEV rebates to cover the preferred dividend and self‑fund future SOL buys. The stock jumped from $2.28 to $22 before closing around $10 on the day of the announcement.

Upexi had 37.2 million shares, so the new issuance was ~54% dilutive for the old stockholders. But the stock jumping by ~400% more than compensated for the dilution.

Sol Strategies is another company that has raised and intends to raise more money from the capital markets to buy SOL. The company operates Solana validators and earns more than 90% of its revenue via staking rewards. While the company has staked 390k SOL ,~3.16 million SOL is delegated by third parties. In April 2025, Sol Strategies had secured a financing facility of up to $500 million through a convertible note agreement with ATW Partners. The initial $20 million has already been deployed to purchase 122,524 SOL.

Recently, the company filed a shelf prospectus to raise another $1 billion via different offerings of common shares (including through “at-the-market” offerings), warrants, subscription receipts, units, debt securities, or any combination. This gives them the flexibility to raise via different mechanisms.

Unlike Strategy’s convertible notes, both SparkLink and Upexi raised funds by issuing new stock upfront. In my opinion, the Strategy’s model of allowing the optionality of redeeming 100% cash targets a different investor class. If I’m just going to get ETH or SOL exposure by buying your stock, why shouldn’t I just buy ETH or SOL? Why do I take the added risk of the middleman having the ability to lever-up more than my comfort zone? The fundraising using convertible notes with enough buffer of operating profits to service interest payments makes more sense unless there's some added service.

When the Music Stops

These convertible notes target hedge funds and institutional bond traders seeking asymmetric risk-reward opportunities. They're not designed for retail investors or traditional equity funds.

From their perspective, these instruments offer a "heads I win big, tails I don't lose much" proposition that fits within their risk frameworks. Convert the bond if bitcoin delivers the expected 30-50% upside over two to three years, or collect 100% of principal back if things go sideways, even if that means losing a bit to inflation.

The beauty of this structure is that it solves a real institutional problem. Many hedge funds and pension funds either lack the infrastructure to hold crypto directly or face mandate restrictions that prevent them from buying bitcoin outright. These convertible instruments provide a regulatory-compliant backdoor into crypto markets while maintaining the downside protection that fixed-income allocations require.

This advantage is inherently temporary. As regulatory clarity improves and more direct crypto investment vehicles with custody solutions, regulated exchanges, and clearer accounting standards emerge, the need for these elaborate workarounds diminishes. The 73% premium that investors currently pay for bitcoin exposure through Strategy will likely compress as more direct alternatives become available.

We have seen this movie before. Opportunistic managers once exploited the Grayscale Bitcoin Trust’s (GBTC) premium—buying BTC and keeping it in Greyscale's trust and selling GBTC shares in the secondary market at a 20–50% premium to NAV. When everyone started doing it, GBTC swung from a peak premium to a record 50% discount to NAV by late 2022. This cycle underscores that without sustainable revenues to underpin repeat financings, crypto‑backed equity plays are eventually arbitraged away.

The critical question is how long it can last and who will be left standing when the premiums collapse. Companies with strong underlying businesses and conservative leverage ratios might weather the transition. Those chasing crypto treasuries without durable revenue streams or defensible moats may find themselves facing dilution-driven selloffs once the speculative fever breaks.

For now, the music is playing, and everyone's dancing. Institutional capital is flowing, premiums are expanding, and more companies are announcing bitcoin and crypto treasury strategies every week. But smart money recognises that this is a trade, not an investment thesis. The firms that survive will be those that use this window to build lasting value beyond their crypto holdings.

The transformation of corporate treasuries may be permanent, but the extraordinary premiums we're seeing today are not. The question is whether you're positioned to profit from the trend or just another player hoping to find a chair when the music stops.

Signing out,

Saurabh Deshpande